US STOCKS: Late Morning Equities Roundup: Off New Highs, Heavy Earnings Next Wk

Jul-18 15:38

- Stocks are retreating to moderately weaker levels late Friday morning - after the SPX emini and Nasdaq indexes managed to extend all time highs around the open.

- Currently, the DJIA trades down 147.91 points (-0.33%) at 44338.46, S&P E-Minis down 3.5 points (-0.06%) at 6337.75 (6357.0 high) , Nasdaq up 14.6 points (0.1%) at 20902.13 (20980.56 high).

- While generally upbeat upbeat earnings at the start of the latest cycle helped push indexes to new highs - investors took profits ahead next week's full docket of earnings releases across multiple sectors: Consumer Staples, Tech and Media, Industrial, Health Care, Energy and Financials.

- Some big names reporting next week include: Domino's Pizza, Coca-Cola, Alphabet, AT&T Inc, T-Mobile, Verizon Communications, IBM, Intel, Philip Morris, PulteGroup, Hasbro Inc, Amphenol, O'Reilly Automotive, Tesla and CSX Corp.

- Meanwhile, Friday's leading gainers included: Invesco +12.15%, Vistra +5.75%, Coinbase Global +4.93%, Regions Financial +4.69%, Constellation Energy +4.28%, Dell Technologies +3.84% and Abbott Laboratories +3.79%.

- Conversely, Health Care sector stocks, particularly pharmaceuticals underperformed: Elevance Health -5.20%, Molina Healthcare -4.24%, Viatris -3.51% and Humana -2.42%. Other laggers included Netflix -5.27%, American Express -3.12% and 3M Co -3.40%.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US DATA: Business Inflation Expectations Contained In June – Atlanta Fed

Jun-18 15:37

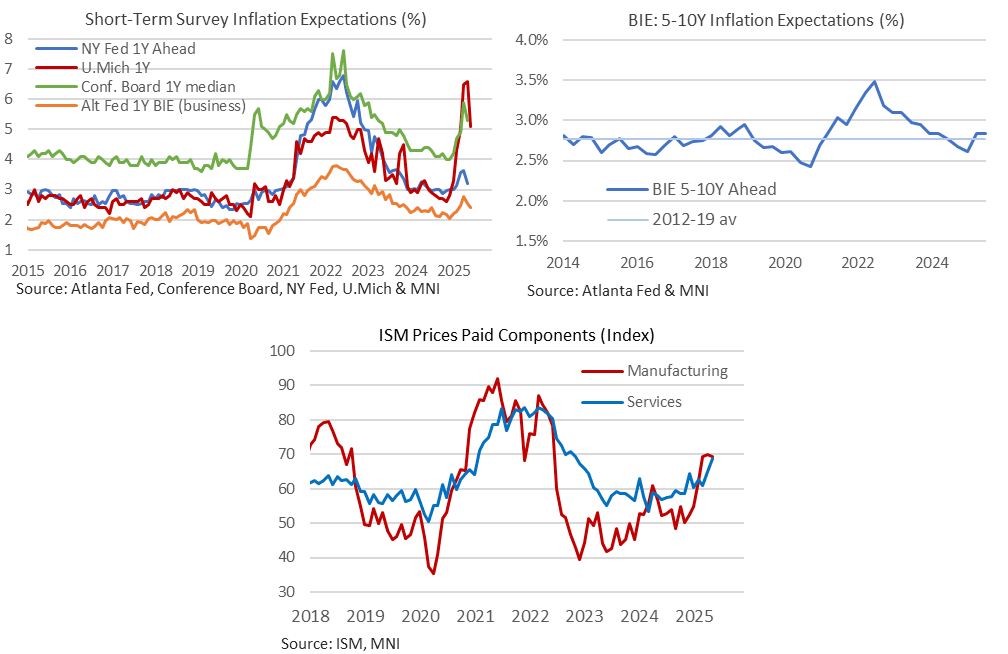

The Atlanta Fed’s Business Inflation Expectations survey for June (in-depth report, here) continued to show relatively modest impacts from US tariff policy.

- Firms’ 1Y ahead inflation expectations, defined in the details as the mean change in expected unit costs over the next 12 months, fell to 2.42% in June from 2.54% in May.

- It’s down from a recent high of 2.76% in April (highest since Jul 2023) for the lowest since February but still a little above the 2.24% averaged in 2024 for context.

- The increase and subsequent pullback is more in keeping with a modest increase in consumer expectations from the NY Fed’s survey as opposed to the sharper climbs in the U.Mich survey and less so Conference Board survey.

- This release also sees the quarterly question for firms’ long-run unit cost inflation expectations 5-10Y ahead, with it unchanged at 2.8% from the March survey. It’s up from Q4 low of 2.6% (lowest since 3Q20) but has only increased back to the 2.8% averaged since the survey started in 2012 through 2019.

- The combination points to a more mellow uptick in inflation expectations compared to sharper increases in prices paid components of ISM manufacturing and services surveys as of May.

FED: US TSY 8W BILL AUCTION: HIGH 4.470%(ALLOT 16.95%)

Jun-18 15:32

- US TSY 8W BILL AUCTION: HIGH 4.470%(ALLOT 16.95%)

- US TSY 8W BILL AUCTION: DEALERS TAKE 48.72% OF COMPETITIVES

- US TSY 8W BILL AUCTION: DIRECTS TAKE 9.12% OF COMPETITIVES

- US TSY 8W BILL AUCTION: INDIRECTS TAKE 42.16% OF COMPETITIVES

- US TSY 8W BILL AUCTION: BID/CVR 2.70

FED: US TSY 4W BILL AUCTION: HIGH 4.060%(ALLOT 48.91%)

Jun-18 15:32

- US TSY 4W BILL AUCTION: HIGH 4.060%(ALLOT 48.91%)

- US TSY 4W BILL AUCTION: DEALERS TAKE 18.15% OF COMPETITIVES

- US TSY 4W BILL AUCTION: DIRECTS TAKE 2.93% OF COMPETITIVES

- US TSY 4W BILL AUCTION: INDIRECTS TAKE 78.92% OF COMPETITIVES

- US TSY 4W AUCTION: BID/CVR 3.15