EM LATAM CREDIT: LATAM Credit Market Wrap

Source: Bloomberg Finance L.P.

Measure Level Δ DoD

5yr UST 3.73% -0bp

10yr UST 4.15% +0bp

5s-10s UST 42.2 +1bp

WTI Crude 57.9 -0.6

Gold 4278 +49.1

Bonds (CBBT) Z-Sprd Δ DoD

ARGENT 3 1/2 07/09/41 821bp +5bp

BRAZIL 6 1/8 03/15/34 233bp -2bp

BRAZIL 7 1/8 05/13/54 317bp -3bp

COLOM 8 11/14/35 337bp -5bp

COLOM 8 3/8 11/07/54 387bp -4bp

ELSALV 7.65 06/15/35 348bp -3bp

MEX 6 7/8 05/13/37 221bp -3bp

MEX 7 3/8 05/13/55 267bp -3bp

CHILE 5.65 01/13/37 115bp -0bp

PANAMA 6.4 02/14/35 197bp -2bp

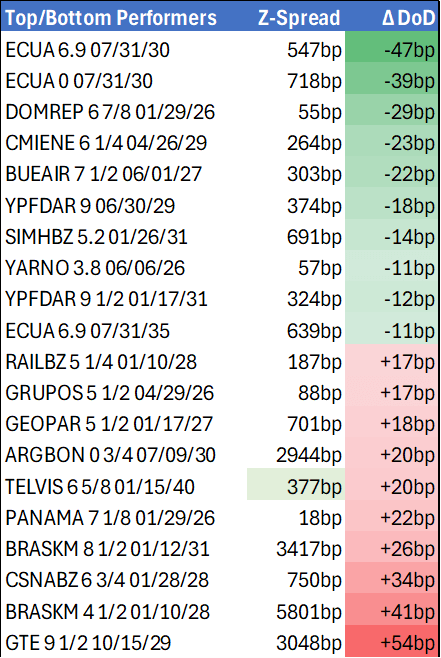

CSNABZ 5 7/8 04/08/32 716bp +12bp

MRFGBZ 3.95 01/29/31 255bp +4bp

PEMEX 7.69 01/23/50 479bp -4bp

CDEL 6.33 01/13/35 173bp -1bp

SUZANO 3 1/8 01/15/32 166bp -0bp

FX Level Δ DoD

USDBRL 5.41 -0.07

USDCLP 914.38 -8.97

USDMXN 18.0 -0.13

USDCOP 3809.25 -33.29

USDPEN 3.37 -0.00

CDS Level Δ DoD

Mexico 93 (3)

Brazil 139 (3)

Colombia 210 (3)

Chile 44 (1)

CDX EM 98.74 (0.00)

Main stories recap:

· The S&P 500 hit a new record high while Nasdaq finished slightly lower, possibly indicating a broadening trend away from big tech. Treasuries closed mostly unchanged after yesterday’s less hawkish than expected press conference by Fed Chairman Powell.

· Rate cuts across EM globally provided a positive backdrop fundamentally, with Philippines cutting their policy rate 25bp to 4.5%, the fifth time this year, while Turkey cut rates a larger than expected 150bp as they cited lower inflation. Secondary spread changes for sovereigns ranged from -5/+5bp in CEEMEA while corporate bonds exhibited a widening bias of up to 5bp.

· In LATAM, spreads generally tightened 2-6bp though there were a few exceptions such as the Argentina sovereign with prices down about ½ point. Argentina reported higher than expected November inflation of 2.5% MoM with core up 2.6% and YoY inflation at 31.4% vs earlier in the year projections of 20-25% for 2025 that clearly will not be achievable.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BONDS: Slightly Richer With US Tsy Futures

NZGBs are flat to 2bps richer, with the 5-year benchmark leading.

- US tsy futures holding firmer. Currently, the Dec'25 10Y contract finished trading +10 at 113-00 vs. 113-01.5 high - just below resistance at 113-02, the Nov 5 and 7 high. Clearance of this level would highlight a potential bullish reversal – MNI Tech

- Otherwise, a short-term bear theme in US tsy futures remains in place. Attention is on a reversal trigger at 112-06, the Sep 25 low, and the 100-DMA, at 112-08. A clear break of these price points would expose a trendline support at 112-02.

- Bloomberg reports that, "First-Time Buyers Snap Up New Zealand Property After Price Slide. People signing up to buy their first property in New Zealand made up a record 27.7% of all transactions in the third quarter, according to the Cotality-Westpac NZ First Home Buyer Report."

- Swap rates are 2bps lower.

- RBNZ dated OIS pricing is little changed across meetings. 28bps of easing is priced for November, with a cumulative 38bps by February 2026.

- Today, the local calendar will be empty ahead of Card Spending data tomorrow.

- On Thursday, the NZ Treasury plans to sell NZ$250mn of the 4.50% May-30 bond, NZ$150mn of the 4.25% May-34 bond and NZ$50mn of the 5.00% May-54 bond.

OIL: Crude Rallies As Market Watches Rise In Product Prices

Oil rallied on Tuesday as the impact on global supplies from sanctions on Russia came to the fore again after US President Trump said that a US-India trade deal was close. Also, demand for products remains robust, as seen in US inventory data, and the announcement of restrictions on Russia’s Rosneft and Lukoil drove prices sharply higher. Short-covering also supported oil benchmarks on Tuesday.

- WTI rose 1.5% to $61.04/bbl after reaching $61.28, below initial resistance at $62.59, 24 October high. It fell to $59.66 but has struggled to hold moves below $60, which provided support to the benchmark from a technical perspective. Support lies at $58.83, 6 November low.

- Brent was up 1.7% to $65.13/bbl after a peak of $65.31 to be slightly higher in November. It approached resistance at $65.98, 9 October high. Initial support is a $62.84, 6 November low.

- With product prices surging, attention will be on Wednesday’s US industry inventory data. The official EIA release will be Thursday.

- India is the second largest importer of Russian oil and if it looks to other sources there could be a large quantity of Russian crude unconsumed.

- The excess oil supply driven by increased OPEC and non-OPEC output remains in focus with the spread between the WTI December-January contracts only 6c. The EIA short-term outlook, IEA annual report and OPEC monthly report are published Wednesday.

JPY: USD/JPY - Fails Toward 154.50 Again On A Weaker ADP Print

The overnight range was 153.67 - 154.44, Asia is currently trading around 154.10. The pair failed again back toward the 154.50 area as the USD got sold off in response to a weaker ADP print. The return of a positive sentiment in risk has brought the focus in USD/JPY back to the 154-155 resistance area. A sustained break above here is needed to potentially see the uptrend regain upward momentum, through here the focus would then turn toward the 160 area where I would start to become wary of intervention risks. On the day it looks to be a 153.60-154.50 range, look for dips back toward 152.00 and then the more important 149.00-150.00 area to be supported.

- MNI BRIEF: Japan Oct Sentiment Posts 6th Straight Rise. Japan’s Economy Watchers sentiment index rose for a sixth consecutive month in October, prompting the government to upgrade its assessment from the previous month. The stronger data helped ease some Bank of Japan concerns that private consumption may lose momentum as households struggle with high living costs, though the survey does not directly measure consumption.

- MNI INTERVIEW: Fed's Risk Management Cuts Not Enough - Revelio. The U.S. labor market will continue to soften and the Federal Reserve's 50 basis points of interest rate easing so far this year will not be enough to shore up hiring, private data provider Revelio Labs’ chief economist Lisa Simon told MNI.

- Options : Close significant option expiries for NY cut, based on DTCC data: 152.00($668m). Upcoming Close Strikes : none - BBG.

- Data/Event : Money Stock M2, Machine Tool Orders

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P