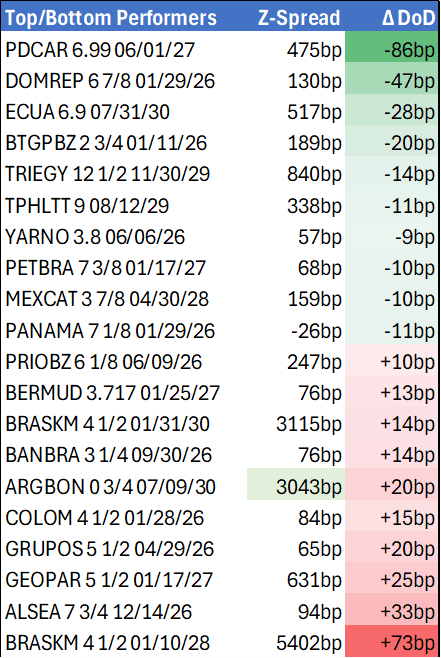

EM LATAM CREDIT: LATAM Credit Market Wrap

Source: Bloomberg Finance L.P.

Measure Level Δ DoD

5yr UST 3.59% +2bp

10yr UST 4.02% +2bp

5s-10s UST 42.6 +0bp

WTI Crude 59.1 +0.5

Gold 4203 +45.1

Bonds (CBBT) Z-Sprd Δ DoD

ARGENT 3 1/2 07/09/41 825bp N/A

BRAZIL 6 1/8 03/15/34 234bp +7bp

BRAZIL 7 1/8 05/13/54 319bp -2bp

COLOM 8 11/14/35 329bp -3bp

COLOM 8 3/8 11/07/54 385bp -4bp

ELSALV 7.65 06/15/35 361bp -1bp

MEX 6 7/8 05/13/37 225bp -3bp

MEX 7 3/8 05/13/55 269bp -4bp

CHILE 5.65 01/13/37 124bp -1bp

PANAMA 6.4 02/14/35 221bp -4bp

CSNABZ 5 7/8 04/08/32 795bp +1bp

MRFGBZ 3.95 01/29/31 285bp -7bp

PEMEX 7.69 01/23/50 489bp -4bp

CDEL 6.33 01/13/35 184bp -4bp

SUZANO 3 1/8 01/15/32 176bp -3bp

FX Level Δ DoD

USDBRL 5.34 -0.01

USDCLP 928.30 -0.68

USDMXN 18.3 -0.04

USDCOP 3740.69 -2.56

USDPEN 3.36 -0.00

CDS Level Δ DoD

Mexico 98 (1)

Brazil 142 (0)

Colombia 204 (3)

Chile 48 (0)

CDX EM 98.38 (0.00)

Main stories recap:

· Major U.S. equity indexes climbed about .5% higher while Treasury yields rose 2-3bp with no economic data to justify the move and month end trading flows dominating.

· LATAM secondary market benchmark USD bond spreads tightened 2-3bp in investment grade rated names and tightened 5-7bp in high yield credits.

· Ecuador 2035s rose another half point today, leaving them up 5 ½ points for the week from a combination of a debt ratings upgrade from Fitch late last week and additional financial support from development banks that was approved this week.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

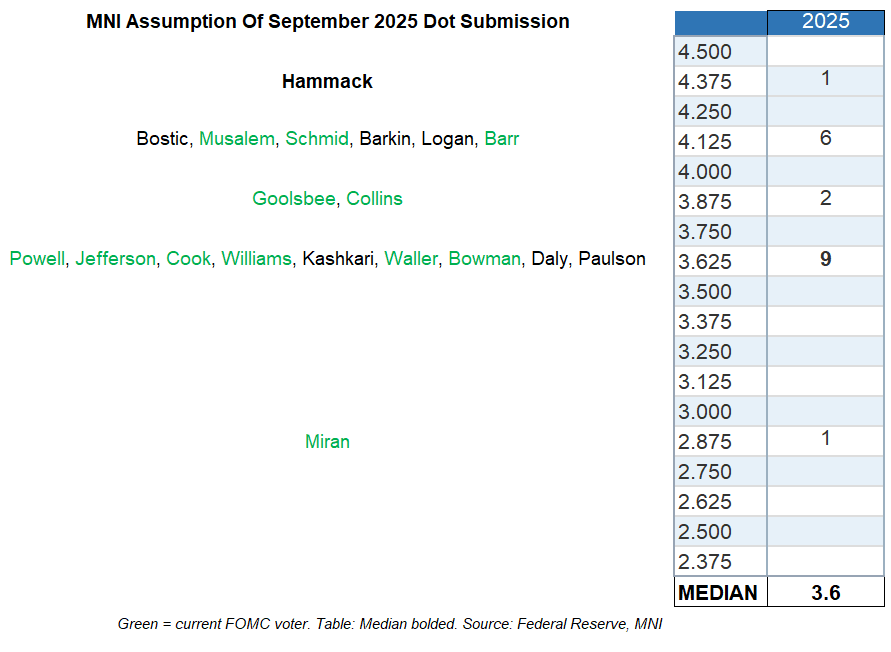

FED: Communications Reforms A Potential Topic Of FOMC Discussion

The Fed has signaled that this fall it would explore changes in the way it communicates policy as part of its framework review. This could be a key topic of conversation at the October FOMC meeting, with a variety of areas under scrutiny. At the very least we expect Chair Powell to be asked about this at the press conference.

- Various FOMC participants have suggested changes including changing the Dot Plot to no longer include the longer-run rate dot, and/or to show rate projections over rolling horizons rather than just for year-end.

- The latest rate policy communications have illustrated the potential utility of rolling horizons, since the September projections are basically a point estimate for Fed moves the remaining 2 meetings of the year).

- Other potential changes include scenario projections and joining-up macro forecasts by participant (instead of potentially disjointed forecasts across different variables).

- While an announcement on conclusions is unlikely at the October meeting, we will be interested in what Powell has to say about it – particularly with the December Dot Plot round looming.

- For what it's worth, here is MNI's assessment of where current FOMC participants placed their end-2025 Funds rate dots as of the September FOMC submission - see our preview for full commentary by all officials since that meeting.

BOC: Canada Bank Analysts Close To Abandoning Future Rate Cut Views Post-BOC

Canadian institutions have all but thrown in the towel on further BOC cuts after today's rate decision. Prior to the October meeting, BMO, Desjardins, and National each saw one further 25bp easing to a 2.00% terminal overnight rate - their post-meeting comments (below) suggest a reconsideration if not outright abandonment. Coming into the meeting, CIBC, RBC, Scotiabank, and TD each had no cuts beyond October as their base case and have retained that view.

- BMO doesn't quite abandon an expectation for further cuts but acknowledges "that’s likely it, for now, for Bank of Canada easing. The Bank appears to believe that the easing to date will offer support; inflation is steadily on its way back to 2%; and the usefulness of monetary policy is somewhat limited in this unique economic environment. That said, we believe that ongoing softness in the job market leaves the door open for some further support, and another 25 bp rate is still on the table for early-2026."

- National concurs: "To us, it’s reasonably likely that the Bank is now done as we share similar outlooks for growth and inflation. At the same time, we still judge economic risks as being skewed to the downside which warrants markets discounting some probability of further easing. Indeed, we wouldn’t close the door on a potential cut at one of the next couple meetings as incoming data—including a couple of jobs reports before December 10th —has the potential to change the outlook. At this point though, it seems a ‘hold’ is the more likely outcome. One naturally wonders how much next week’s federal budget led to the “hawkish cut”. Certainly, looser fiscal policy is supportive of growth and inflation over time, but we don’t expect marginal spending to immediately bring the Canadian economy out of its current malaise."

- Desjardins writes more conclusively: "The bar is high for further monetary policy support. ... We are now of the view that the Bank of Canada will keep interest rates on hold for the foreseeable future."

US 10YR FUTURE TECHS: (Z5) Trend Signals Remain Bullish

- RES 4: 115-00+ High Oct 1 ‘24 (cont)

- RES 3: 114-21+ 1.00 proi of the Aug 18 - Sep 11 - 25 price swing

- RES 2: 114-10 High Apr 7 (cont) and a key resistance

- RES 1: 113-24/114-02 High Oct 24 / 17 and the bull trigger

- PRICE: 113-15+ @ 16:52 GMT Oct 29

- SUP 1: 113-04 Low Oct 27

- SUP 2: 112-27 50-day EMA

- SUP 3: 112-16+ Low Oct 10

- SUP 4: 112-06 Low Sep 25 and a reversal trigger

The trend structure in Treasuries remains bullish. Moving average studies are in a bull-mode position, highlighting a dominant uptrend. Attention is on 114-02, the Oct 24 high and a bull trigger. A breach of this hurdle would confirm a resumption of the medium-term uptrend, and open 114-10, the Apr 7 high (cont). Support to watch is 112-27, the 50-day EMA. A clear breach of the average would instead highlight scope for a deeper retracement.