EM LATAM CREDIT: LATAM Credit Market Wrap

Source: Bloomberg Finance L.P.

Measure Level Δ DoD

5yr UST 3.59% +4bp

10yr UST 4.01% +3bp

5s-10s UST 41.5 -1bp

WTI Crude 57.5 +0.1

Gold 4252 -74.8

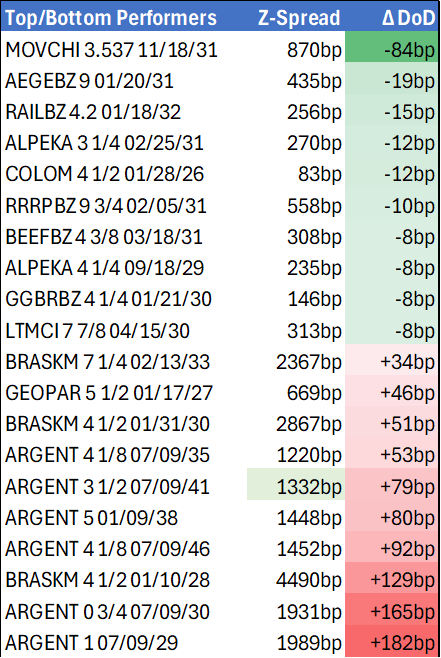

Bonds (CBBT) Z-Sprd Δ DoD

ARGENT 3 1/2 07/09/41 1332bp +80bp

BRAZIL 6 1/8 03/15/34 231bp -3bp

BRAZIL 7 1/8 05/13/54 320bp -1bp

COLOM 8 11/14/35 330bp -7bp

COLOM 8 3/8 11/07/54 386bp -6bp

ELSALV 7.65 06/15/35 388bp -4bp

MEX 6 7/8 05/13/37 225bp -1bp

MEX 7 3/8 05/13/55 271bp -1bp

CHILE 5.65 01/13/37 129bp -3bp

PANAMA 6.4 02/14/35 242bp -6bp

CSNABZ 5 7/8 04/08/32 617bp +3bp

MRFGBZ 3.95 01/29/31 270bp -1bp

PEMEX 7.69 01/23/50 496bp +0bp

CDEL 6.33 01/13/35 193bp -2bp

SUZANO 3 1/8 01/15/32 178bp -6bp

FX Level Δ DoD

USDBRL 5.41 -0.03

USDCLP 957.65 +1.70

USDMXN 18.4 -0.07

USDCOP 3831.20 -18.96

USDPEN 3.38 -0.01

CDS Level Δ DoD

Mexico 97 2

Brazil 147 2

Colombia 203 (1)

Chile 55 1

CDX EM 97.55 0.05

CDX EM IG 101.23 0.01

CDX EM HY 93.14 0.02

Main stories recap:

· Treasury yields rose about 4bp as U.S. regional bank stocks bounced back which was supportive for major U.S. equity indexes.

· LATAM benchmark bond spreads were generally 3-7bp tighter though there were exceptions.

· Argentina sovereign bonds slipped 1.5 pt as the market did not greet the idea of collateral backed private-sector loans warmly and has become less reactive to U.S. expressions of support.

· Telefonica Moviles Chile bonds moved 2 points higher as we awaited more news about a potential joint purchase of the struggling company from Spain based Telefonica by Mexico based America Movil and Chile’s Entel.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

ASIA: Coming Up In Asia Pac Markets On Thursday

| 2345BST | 0645HKT | 0845AEST | New Zealand Q2 GDP |

| 0050BST | 0750HKT | 0950AEST | Japan July Core Machine Orders |

| 0200BST | 0900HKT | 1100AEST | China Aug Swift Global Payments In CNY |

| 0230BST | 0930HKT | 1130AEST | Australia Aug Jobs Report |

| 0335BST | 1035HKT | 1235AEST | New Zealand 2030, 2024 Bond Sale |

| 0430BST | 1130HKT | 1330AEST | Japan 3mth Bill Sale |

| 0600BST | 1300HKT | 1500AEST | Japan Aug Tokyo Condominiums For Sale |

Source: Bloomberg Finance L.P./MNI

FED: MNI Fed Review-Sept 2025: No Risk-Free Paths Now

We've published our review of the September FOMC meeting - Download Full Report Here

- The Fed resumed its easing cycle with the first cut of the year on September 17, of 25bp to a range of 4.00-4.25%. That decision was expected, but the lack of conviction on the FOMC about the rate path forward was a key theme of the September meeting’s release materials, as well as Chair Powell’s press conference.

- Despite a lower rate path signaled in the new Dot Plot, a seeming lack of clarity on delivering those future rate cuts saw an early dovish market reaction subsequently reverse.

- See PDF report for:

- MNI View

- Market Reaction

- MNI Instant Answers

- Press Conference Transcript

- FOMC Meeting Links

- Policy Statement Changes

- Dot Plot/Econ Projections

FED: Monthly Data In Sharper Focus Ahead Of October's Meeting (3/3)

On inflation, Powell said “since April, to me, the risks of higher and more persistent inflation have probably become a little less… We continue to expect it to move up, maybe not as high as we would have expected it to move up a few months ago. The passthrough of the tariffs into inflation has been slower and smaller. The labor market has softened. So the case for there being a persistent inflation outbreak is less.”

- On whether the Fed would have cut earlier in the year had they known payrolls would be substantially revised lower: “We have to live life looking through the windshield rather than the rear view mirror, as you know, and all I can tell you is we see where we are now and we take appropriate action. And we took that appropriate action today.”

- All of that sets up what, as Powell said, would be a meeting-by-meeting approach. It’s possible we could get more sensitivity to individual releases, as there aren’t many major ones ahead of the next decision at end-October (one CPI, one nonfarm payrolls). A stronger-than-expected employment report in particular could see conviction on an end-October cut dissipate quickly. As such the 85+% priced 25bp cut at that juncture may be on the high side depending on one’s forecasts for the monthly data.