EM LATAM CREDIT: LATAM Credit Market Wrap

Source: Bloomberg Finance L.P.

Measure Level Δ DoD

5yr UST 3.65% -9bp

10yr UST 4.05% -9bp

5s-10s UST 40.2 +0bp

WTI Crude 58.9 -2.6

Gold 4008 +31.0

Bonds (CBBT) Z-Sprd Δ DoD

ARGENT 3 1/2 07/09/41 1150bp +45bp

BRAZIL 6 1/8 03/15/34 260bp +25bp

BRAZIL 7 1/8 05/13/54 341bp +22bp

COLOM 8 11/14/35 336bp +15bp

COLOM 8 3/8 11/07/54 396bp +15bp

ELSALV 7.65 06/15/35 391bp +15bp

MEX 6 7/8 05/13/37 228bp +11bp

MEX 7 3/8 05/13/55 276bp +11bp

CHILE 5.65 01/13/37 139bp +8bp

PANAMA 6.4 02/14/35 245bp +13bp

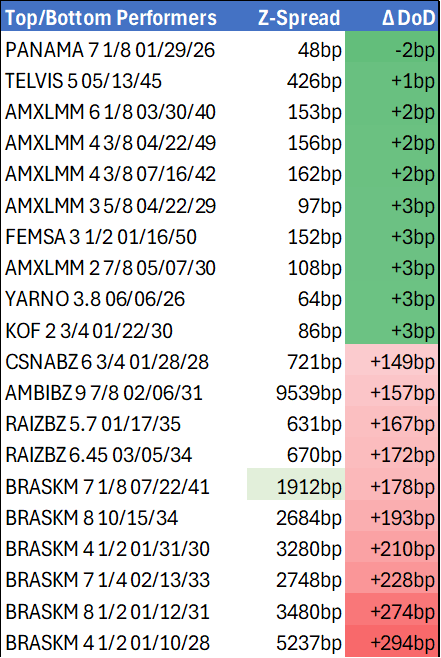

CSNABZ 5 7/8 04/08/32 688bp +73bp

MRFGBZ 3.95 01/29/31 295bp +34bp

PEMEX 7.69 01/23/50 501bp +28bp

CDEL 6.33 01/13/35 191bp +11bp

SUZANO 3 1/8 01/15/32 180bp +16bp

FX Level Δ DoD

USDBRL 5.50 +0.13

USDCLP 959.97 +9.21

USDMXN 18.6 +0.18

USDCOP 3925.35 +39.08

USDPEN 3.44 +0.01

CDS Level Δ DoD

Mexico 99 10

Brazil 159 17

Colombia 210 16

Chile 59 6

CDX EM 97.36 (0.46)

CDX EM IG 101.20 (0.28)

CDX EM HY 92.84 (0.70)

Main stories recap:

· U.S. major equity indexes fell 2-3% and Treasury yields dropped 9bp as President Trump declared a massive increase of U.S. tariffs on Chinese products.

· Bond spread changes in Asia and CEEMEA ranged from -2 to +5bp, much milder than LATAM as their market had already closed prior to the trade flare up.

· The LATAM secondary market was weaker today. Benchmark bond spreads for LATAM investment grade sovereign and corporates widened about 10-15bp. Argentina sovereign bond prices declined a point while Ecuador bonds fell 2-3 points.

· Brazil corporate bonds were the worst behaved in the market. Brazil sovereign bonds were down on average only a point while some corporate bonds with idiosyncratic issues like Raizen fell 8 points. Several other Brazil high yield corporate names fell 2-3 points.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US OUTLOOK/OPINION: Wells Fargo: Sticky Services To Continue

Wells Fargo is on the low end of sell-side expectations for unrounded core CPI, seeing a 0.29% M/M increase in August, but still expect “sticky services inflation alongside the rebound in goods prices” continuing.

- Core goods are set to rise 0.25% M/M: “New vehicle inflation, which has been tame, is poised to strengthen as a rebound in auto sales has helped to reduce inventory and the use of incentives has slowed. Price growth for other import-heavy items, such as apparel, recreational goods and communication hardware, should remain solid as well with another 0.3% increase.”

- Meanwhile core services prices to rise 0.30% M/M: “Travel-related service prices started to rebound in July, and we estimate another solid gain in August (+1.0%), led by lodging away from home. While spending on discretionary services remains generally weak, consumers' appetite for travel shows signs of rebounding with hotel occupancy and TSA screenings up again on a year-ago basis, suggestive of some stabilization in consumer demand.”

- However, medical care services could moderate after July’s jump and primary shelter inflation “should run a touch under its 0.31% year-to-date average through the remainder of 2025”.

AUDUSD TECHS: Pierces Bull Trigger

- RES 4: 0.6688 High Nov 7 ‘24

- RES 3: 0.6677 0.764 proj of the Jun 23 - Jul 11 - 17 price swing

- RES 2: 0.6667 3.0% Upper Bollinger Band

- RES 1: 0.6636 High Sep 10

- PRICE: 0.6625 @ 16:32 BST Sep 10

- SUP 1: 0.6511 20-day EMA

- SUP 2: 0.6463/6415 Low Aug 27 / Low Aug 21 / 22 and a bear trigger

- SUP 3: 0.6373 Low Jun 23

- SUP 4: 0.6354 38.2% retracement of the Apr 9 - Jul 24 upleg

AUDUSD built on the recent firmer tone, ending the corrective phase that started on Jul 24. Price pierced key resistance and the bull trigger at 0.6625, the Jul 24 high on Wednesday. A clear breach of this level would resume the uptrend and open 0.6677, a Fibonacci projection. Support to watch is 0.6415, the Aug 21 / 22 low. A clear break of it would instead highlight a stronger reversal.

US OUTLOOK/OPINION: Goldman At High End Of Core CPI Views On Cars, Airfares

From our inflation preview, at the top end of sell-side analysts' unrounded core CPI expectations is Goldman Sachs seeing 0.36% M/M in August, corresponding to a Y/Y rate of 3.13% (vs. +3.1% consensus).

- Four trends to watch:

- Used car prices seen rising 1.2%, “reflecting an increase in auction prices, and new car prices (+0.2%), reflecting a decline in dealer incentives.”

- Car insurance seen rising 0.4% M/M “based on premiums in our online dataset”.

- Airfares seen rising 3% M/M, “reflecting a boost from seasonal distortions and an increase in underlying airfares based on our equity analysts’ tracking of online price data”.

- “We have penciled in upward pressure from tariffs on categories that are particularly exposed, such as communication, household furnishings, and recreation, worth +0.14pp on core inflation.”

- Their forecast is consistent with core PCE inflation of 0.29% M/M in August.

- They see headline CPI at 0.37% M/M, reflecting higher food (+0.35%) and energy (+0.6%) prices.

- “Over the next few months, we expect tariffs to continue to boost monthly inflation and forecast monthly core CPI inflation around 0.3%. Aside from tariff effects, we expect underlying trend inflation to fall further, reflecting shrinking contributions from the housing rental and labor markets.”

- They see core CPI at 3.1% Y/Y and core PCE at 3.2% Y/Y in Dec 2025 “(or +2.3% for both measures excluding the effects of tariffs)”.