EM LATAM CREDIT: LATAM Credit Market Wrap

Source: Bloomberg Finance L.P.

Measure Level Δ DoD

5yr UST 3.67% +1bp

10yr UST 4.11% +2bp

5s-10s UST 43.8 +1bp

WTI Crude 63.7 -0.4

Gold 3646 -14.1

Bonds (CBBT) Z-Sprd Δ DoD

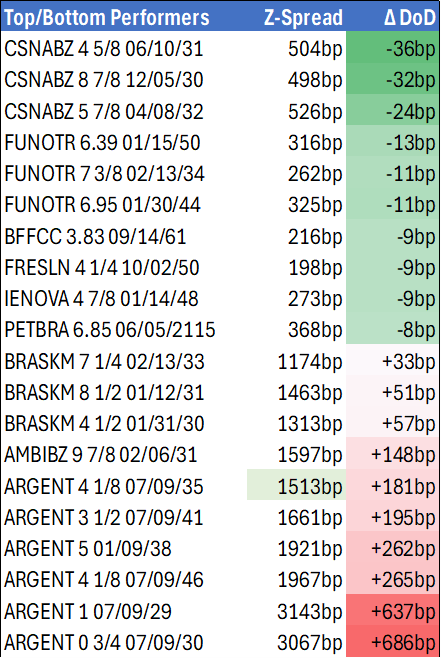

ARGENT 3 1/2 07/09/41 1661bp +196bp

BRAZIL 6 1/8 03/15/34 225bp -0bp

BRAZIL 7 1/8 05/13/54 315bp -1bp

COLOM 8 11/14/35 326bp -3bp

COLOM 8 3/8 11/07/54 381bp -1bp

ELSALV 7.65 06/15/35 381bp -2bp

MEX 6 7/8 05/13/37 232bp -1bp

MEX 7 3/8 05/13/55 281bp -2bp

CHILE 5.65 01/13/37 131bp -1bp

PANAMA 6.4 02/14/35 232bp +2bp

CSNABZ 5 7/8 04/08/32 526bp -24bp

MRFGBZ 3.95 01/29/31 227bp -2bp

PEMEX 7.69 01/23/50 460bp +4bp

CDEL 6.33 01/13/35 176bp -3bp

SUZANO 3 1/8 01/15/32 162bp -1bp

FX Level Δ DoD

USDBRL 5.31 +0.01

USDCLP 954.10 +3.57

USDMXN 18.4 +0.06

USDCOP 3895.63 +16.29

USDPEN 3.48 +0.01

CDS Level Δ DoD

Mexico 86 (0)

Brazil 126 (0)

Colombia 170 (0)

Chile 47 (0)

CDX EM 98.24 (0.11)

CDX EM IG 101.68 (0.01)

CDX EM HY 94.67 (0.17)

Main stories recap:

· U.S. Treasury yields rose 1-2bp as U.S. continuing claims fell more than expected, suggesting the labor market wasn’t nearly as weak as feared.

· The EM primary market slowed with only two new issues out of CEEMEA today.

· LATAM secondary benchmark bond spreads generally tightened a few bp but there were a few interesting outliers.

· Argentina sovereign bonds fell about 4 points today as the central bank had to spend scarce USD reserves to intervene in the FX market. The weakness was triggered by multiple losses for Milei in maintaining budget restraint as Congress overrode his vetoes of spending bills and provincial transfer payments.

· Ecuador sovereign bonds fell 2 points as opposition to a cut in fuel subsidies grew with indigenous groups now planning a general strike.

· CSN bonds rose more than a point as a Japanese steel company was in talks to add to their existing stake in CSN’s iron ore subsidiary

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

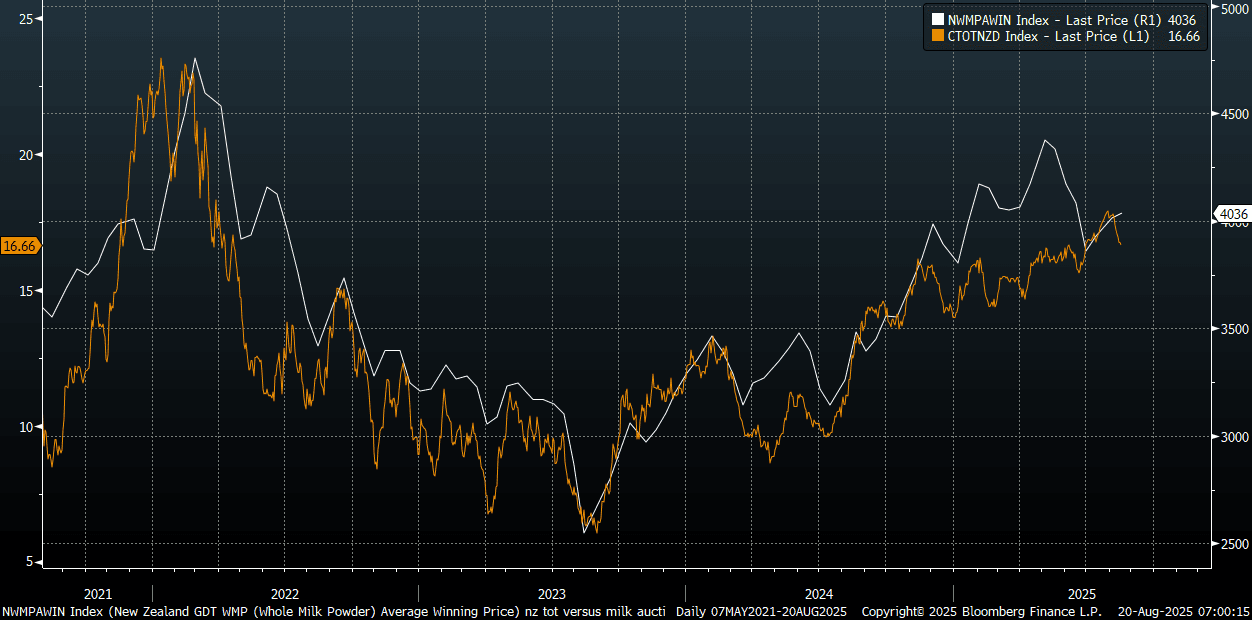

NEW ZEALAND: Whole Milk Prices Edge Higher At Latest Auction

Overnight the whole milk powder auction (held around 2 times per month) saw average prices rise 0.3% to $4036. The chart below overlays this series versus the Citi NZ terms of trade proxy. Whole milk powder prices are up from recent lows but still around 7.7% off 2025 highs (albeit presenting a supportive backdrop for NZ's terms of trade).

- BBG noted: "The GDT price index change, which is a weighted average of the percentage changes in individual milk products between trading events, was a decrease of 0.3%." See this link to GlobalDairyTrade website.

Fig 1: NZ Whole Milk Powder Prices & Citi NZ Terms Of Trade

Source: Citi/Bloomberg Finance L.P./MNI

ASIA: Coming Up In Asia Pac Markets On Wednesday

| 0050BST | 0750HKT | 0950AEST | Japan July Trade Data |

| 0050BST | 0750HKT | 0950AEST | Japan June Core Machine Orders |

| 0200BST | 0900HKT | 1100AEST | China Loan Prime Rates |

| 0200BST | 0900HKT | 1100AEST | Australia 2032 Bond Sale |

| 0300BST | 1000HKT | 1200AEST | RBNZ Decision |

| 0300BST | 1000HKT | 1200AEST | RBA'S McPhee, Jones-Panel Discussion |

| 0400BST | 1100HKT | 1300AEST | RBNZ Governor Press Conference |

| 0400BST | 1100HKT | 1300AEST | South Korea 2Q External Debt |

| 0600BST | 1300HKT | 1500AEST | Japan July Tokyo Condominiums For Sale |

Source: Bloomberg Finance L.P./MNI

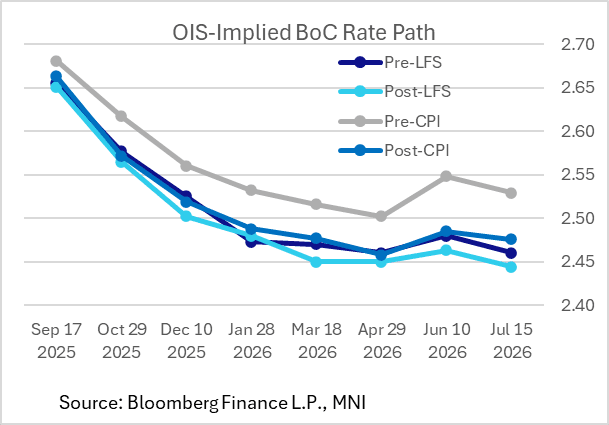

BOC: Implied Cuts Increase Post-CPI, But Still Some Data To Go Before September

The implied BOC rate path shifted lower following the July CPI data, with about 4bp in cuts added by year-end and improving the probability of a September rate cut to around 36% from 28%. The first full 25bp cut is cumulatively priced by January, vs (not quite) March as seen pre-CPI.

- The two key pieces of data since the July decision - the other was the July Labour Force Survey - have thus each received a dovish reaction, even if implied rates have ticked up between LFS and CPI.

- Current OIS implied cumulative rate cuts, vs the current 2.75% policy rate: Sep (9bp), Oct (17bp), Dec (24bp), Jan (28bp).

- There is another inflation report before the BOC's Sep 17th rate announcement (Sep 16), but most of Governing Council's deliberations will be complete by then so it's not clear it would have much impact on the decision.

- That leaves attention on other data: the next release of note is Friday's retail sales, though that's likely to be overshadowed by Federal Reserve Chair Powell's speech later that morning.

- Most attention for the rest of the month will be on June/Q2 GDP data out on August 29, with the August Labour Force Survey out a week later.