EM LATAM CREDIT: LATAM Credit Market Wrap

Source: Bloomberg Finance L.P.

Measure Level Δ DoD

5yr UST 3.69% -3bp

10yr UST 4.22% -4bp

5s-10s UST 52.3 -1bp

WTI Crude 63.7 -1.9

Gold 3559 +26.3

Bonds (CBBT) Z-Sprd Δ DoD

ARGENT 3 1/2 07/09/41 1119bp -14bp

BRAZIL 6 1/8 03/15/34 245bp +1bp

BRAZIL 7 1/8 05/13/54 333bp +2bp

COLOM 8 11/14/35 361bp -0bp

COLOM 8 3/8 11/07/54 421bp -3bp

ELSALV 7.65 06/15/35 425bp -0bp

MEX 6 7/8 05/13/37 252bp +4bp

MEX 7 3/8 05/13/55 302bp +3bp

CHILE 5.65 01/13/37 140bp -1bp

PANAMA 6.4 02/14/35 263bp -4bp

CSNABZ 5 7/8 04/08/32 575bp +2bp

MRFGBZ 3.95 01/29/31 266bp -2bp

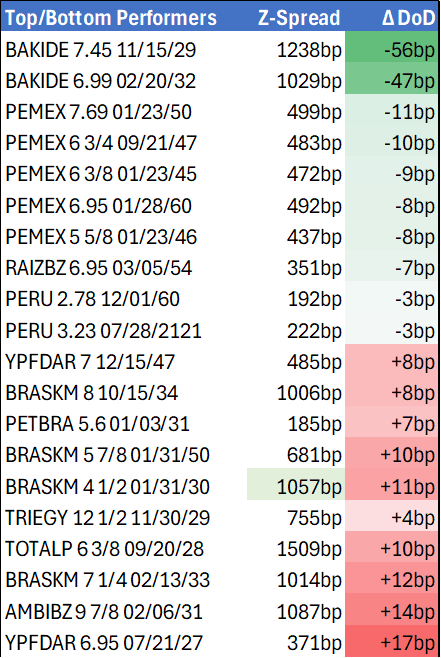

PEMEX 7.69 01/23/50 499bp -11bp

CDEL 6.33 01/13/35 202bp +1bp

SUZANO 3 1/8 01/15/32 177bp -1bp

FX Level Δ DoD

USDBRL 5.45 -0.01

USDCLP 968.94 -4.48

USDMXN 18.7 +0.00

USDCOP 4006.24 +1.76

USDPEN 3.53 -0.00

CDS Level Δ DoD

Mexico 98 (1)

Brazil 138 (2)

Colombia 194 (1)

Chile 51 (1)

CDX EM 98.01 0.02

CDX EM IG 101.42 0.01

CDX EM HY 94.48 0.01

Main stories recap:

· Weak labor market data ahead of this Friday’s monthly jobs report triggered a bull flattener with a nearly 7bp rally in the long bond.

· It was another active day in EM primary with a couple of sovereign/quasi sov deals out of CEEMEA as well as a few GCC deals priced and/or mandated.

· In LATAM we saw a similar pattern with Petrobras printing a USD2bn 2-part deal of 5s/10s following through on Brazil sovereign issuance yesterday. Additionally we saw a Chilean utility Colbun follow through from its investor meetings late last week with a new 10-year and Brazil based global paper company Suzano priced a new 10-year as well.

· In corporate bond secondary trading, Raizen outperformed with bonds tightening 10-15bp as local media reported that co-owner Cosan was talking with some Japanese investors about taking a strategic stake in Raizen and that interest from other parties would be be due by October.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

USDCAD TECHS: Slips Sharply on USD Downdraft

- RES 4: 1.4111 Apr 10

- RES 3: 1.4019 38.2% retracement of the Feb 3 - Jun 16 bear leg

- RES 2: 1.3920 High May 21

- RES 1: 1.3879 High Aug 1

- PRICE: 1.3779 @ 17:25 BST Aug 4

- SUP 1: 1.3716/3557 20-day EMA / Low Jul 03

- SUP 2: 1.3540 Low Jun 16 and the bear trigger

- SUP 3: 1.3503 1.618 proj of the Feb 3 - 14 - Mar 4 price swing

- SUP 4: 1.3473 Low Oct 2 2024

A short-term bullish corrective phase in USDCAD remains in play despite sharp weakness Friday. On the recent run higher, price traded through the 50-day EMA at 1.3739 and this has been followed by a break of resistance at 1.3798, the Jun 23 high. Clearance of 1.3798 represents an important short-term bullish development, signaling scope for a stronger recovery. Sights are on 1.3920 next, the May 21 high. On the downside, initial firm support to watch lies at 1.3716, the 20-day EMA.

US TSYS: Holding Firm, Focus on Tuesday PMIs, ISM Services Data

- Treasuries remain firmer after the bell, Sep'25 10Y futures drifting near session highs for much of the second half. Curves reversed early steepening as bonds rebounded, focus on dovish rate cut pricing instead of Friday's slowing labor market data.

- Tsy Sep'25 10Y futures currently trades +4.5 at 112-11 vs. 112-14 high, curves flatter: 2s10s -2.157 at 50.855, 5s30s -1.554 at 104.770.

- The weak payrolls report dominated what had been a decent-sized hawkish reaction from a patient Fed Chair Powell not giving a nod to a September rate cut at Wednesday’s FOMC press conference. Nonfarm payrolls growth underwhelmed at 73k in July (cons 104k) but the major headline was the -258k two-month downward revision, of which -139k came from the private sector and -119k from the public sector.

- Projected rate cut pricing holds +/- .5bp vs pre-open highs (*) levels: Sep'25 at -23.2bp (-22.6bp), Oct'25 at -40.6bp (-41.1bp), Dec'25 at -61.4bp (-61.6bp).

- Factory orders fell -4.8% M/M (sa, cons -4.8) in June after 8.3% (initial 8.2) in May as they confirmed gyrations driven by nondefense aircraft in the previously released durable goods data (-52% M/M in June after 232% in May).

- Look ahead to Tuesday: China composite and manufacturing PMI data, final PMI prints across Europe and the US as well as the US ISM services index for July.

AUDUSD TECHS: Retracement Mode

- RES 4: 0.6700 76.4% retracement of the Sep 30 ‘24 - Apr 9 bear leg

- RES 3: 0.6688 High Nov 7 ‘24

- RES 2: 0.6677 0.764 proj of the Jun 23 - Jul 11 - 17 price swing

- RES 1: 0.6530/6625 High Jul 29 / 24 and the bull trigger

- PRICE: 0.6465 @ 17:24 BST Aug 1

- SUP 1: 0.6419 Low Aug 1

- SUP 2: 0.6373 Low Jun 23 and a bear trigger

- SUP 3: 0.6354 38.2% retracement of the Apr 9 - Jul 24 upleg

- SUP 4: 0.6323 Low Apr 16

AUDUSD rallied well off the week’s lowest levels last week on broad USD weakness. Last week, the pair traded through both the 20- and 50-day EMAs. This undermined the recent bullish theme and signals the likely start of a corrective cycle. Note that support 0.6455 the Jul 17 low, has also been cleared. The breach strengthens a bearish threat and signals scope for an extension towards 0.6373, the Jun 23 low. Key resistance has been defined at 0.6625 the Jul 24 high. It also represents the bull trigger.