EM LATAM CREDIT: LATAM Credit Market Wrap

Source: Bloomberg Finance L.P.

Measure Level Δ DoD

5yr UST 3.84% +3bp

10yr UST 4.33% +4bp

5s-10s UST 48.1 +1bp

WTI Crude 63.1 -0.8

Gold 3336 +0.7

Bonds (CBBT) Z-Sprd Δ DoD

ARGENT 3 1/2 07/09/41 919bp -2bp

BRAZIL 6 1/8 03/15/34 231bp +1bp

BRAZIL 7 1/8 05/13/54 321bp -0bp

COLOM 8 11/14/35 354bp -2bp

COLOM 8 3/8 11/07/54 425bp -3bp

ELSALV 7.65 06/15/35 410bp -4bp

MEX 6 7/8 05/13/37 234bp -4bp

MEX 7 3/8 05/13/55 287bp -4bp

CHILE 5.65 01/13/37 129bp -2bp

PANAMA 6.4 02/14/35 249bp -5bp

CSNABZ 5 7/8 04/08/32 535bp +0bp

MRFGBZ 3.95 01/29/31 265bp -5bp

PEMEX 7.69 01/23/50 518bp -1bp

CDEL 6.33 01/13/35 186bp -3bp

SUZANO 3 1/8 01/15/32 159bp -6bp

FX Level Δ DoD

USDBRL 5.40 -0.02

USDCLP 963.85 -2.66

USDMXN 18.7 -0.05

USDCOP 4015.29 -38.11

USDPEN 3.56 -0.01

CDS Level Δ DoD

Mexico 97 0

Brazil 137 1

Colombia 191 1

Chile 51 (0)

CDX EM 98.03 (0.01)

CDX EM IG 101.41 0.01

CDX EM HY 94.61 0.00

Main stories recap:

· U.S. equity indexes and Treasuries were little changed in the morning session, ahead of anxiously awaited news from the Trump/Putin meeting in Alaska even as University of Michigan survey data sent stagflation signals with a lower consumer sentiment reading and higher inflation expectations reported.

· U.S. retail sales for the previous month were revised upward, and Atlanta Fed GDP forecasted a solid 2.5% 3rd quarter GDP print based on the new data, so higher inflation expectations were more worrisome than the weaker sentiment and Treasury yields did move higher this afternoon.

· That led to a modest tightening of 1-6bp in LATAM secondary benchmark bond spreads going into the close, a bit better than EM Asia and CEEMEA spread performance which was more mixed.

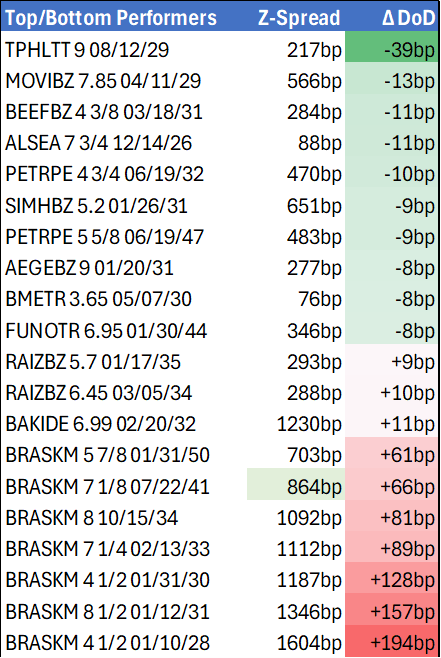

· Braskem bonds underperformed again, dropping about 3 points today, as Moody’s reacted to the Brazil based chemical company’s disappointing 2Q earnings report with a double notch downgrade to ‘B2’ and left a negative outlook.

· Raizen bonds also underperformed, widening 10bp, in the wake of yet another weak earnings report yesterday for the Brazil ethanol processor as the market braced for a potential downgrade.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

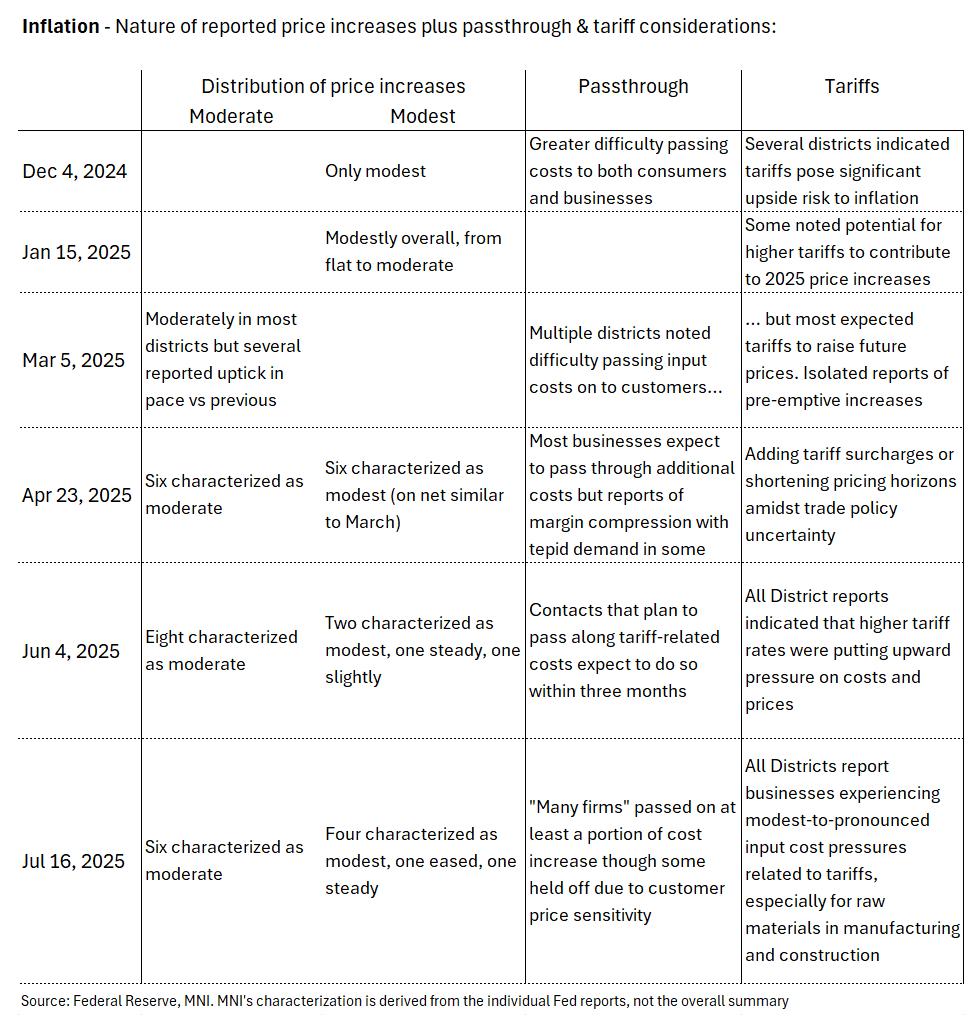

FED: Beige Book: Inflation Seen Rising More Rapidly By Late Summer (1/3)

The July Beige Book's description of inflation suggested relatively steady price pressures compared with the June report, though it seems that what were previously "plans" to pass through tariff-related costs to customers have begun to materialize.

- In probably the most important finding for the FOMC, the biggest price increases are yet to come: "Contacts in a wide range of industries expected cost pressures to remain elevated in the coming months, increasing the likelihood that consumer prices will start to rise more rapidly by late summer."

- District-by-district, 4 Feds reported selling prices increased "modestly" (Boston, Philadelphia, Cleveland, San Francisco), 6 "moderately" (New York, Richmond, Atlanta, Chicago, St Louis, Kansas City), one "eased" (Minneapolis) and one "steady" (Dallas).

- The table below summarizes the recent evolution of the Beige Book's inflation characterization. (Our characterization is derived from the individual Fed reports, not the overall summary.)

- From the July report: "Prices increased across Districts, with seven characterizing price growth as moderate and five characterizing it as modest, mostly similar to the previous report. In all twelve Districts, businesses reported experiencing modest to pronounced input cost pressures related to tariffs, especially for raw materials used in manufacturing and construction. Rising insurance costs represented another widespread source of pricing pressure. Many firms passed on at least a portion of cost increases to consumers through price hikes or surcharges, although some held off raising prices because of customers' growing price sensitivity, resulting in compressed profit margins. Contacts in a wide range of industries expected cost pressures to remain elevated in the coming months, increasing the likelihood that consumer prices will start to rise more rapidly by late summer."

EURGBP TECHS: Bullish Price Sequence

- RES 4: 0.8800 Round number resistance

- RES 3: 0.8781 2.236 pro of the Mar 3 - 11 - 28 price swing

- RES 2: 0.8738 High Apr 11 high and a key resistance

- RES 1: 0.8697/98 High Jul 15/16

- PRICE: 0.8661 @ 17:03 BST Jul 16

- SUP 1: 0.8630 Low Jul 14

- SUP 2: 0.8599 20- day EMA

- SUP 3: 0.8537 50-day EMA

- SUP 4: 0.8508 Low Jun 27

A bullish condition in EURGBP remains intact and the cross is trading closer to its recent highs. Fresh cycle highs this week maintain the price sequence of higher highs and higher lows and note too that moving average studies are in a bull-mode position, highlighting a dominant uptrend. Scope is seen for a climb towards key resistance at 0.8738, the Apr 11 high. Support to watch lies at 0.8599, the 20-day EMA.

PIPELINE: Corporate Bond Update: $4B JPM 11NC10 Debt Launched

- Date $MM Issuer (Priced *, Launch #)

- 07/16 $4B #JP Morgan 11NC10 +112.5

- 07/16 $2.75B #Citigroup PerpNC5 6.875%

- 07/16 $2.2B #Indonesia Sukuk $1.1B 5Y 4.55%, $1.1B 10Y 5.2%

- 07/16 $2.2B #Kioxia Holdings $1.1B 5NC2 6.25%, $1.1B 8NC3 6.625%

- 07/16 $500M #Golub Capital Private Cr 3Y +183