EM LATAM CREDIT: LATAM Credit Market Wrap

Source: Bloomberg Finance L.P.

Measure Level Δ DoD

5yr UST 3.96% -3bp

10yr UST 4.43% -2bp

5s-10s UST 46.9 +1bp

WTI Crude 67.5 -0.0

Gold 3349 +10.2

Bonds (CBBT) Z-Sprd Δ DoD

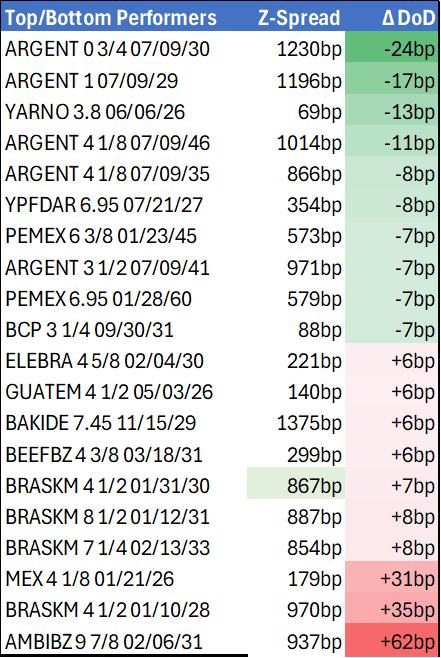

ARGENT 3 1/2 07/09/41 971bp -5bp

BRAZIL 6 1/8 03/15/34 249bp -0bp

BRAZIL 7 1/8 05/13/54 343bp +1bp

COLOM 8 11/14/35 388bp -5bp

COLOM 8 3/8 11/07/54 464bp -4bp

ELSALV 7.65 06/15/35 434bp +1bp

MEX 6 7/8 05/13/37 254bp -3bp

MEX 7 3/8 05/13/55 316bp -3bp

CHILE 5.65 01/13/37 140bp -2bp

PANAMA 6.4 02/14/35 295bp -5bp

CSNABZ 5 7/8 04/08/32 573bp +3bp

MRFGBZ 3.95 01/29/31 279bp +3bp

PEMEX 7.69 01/23/50 599bp -6bp

CDEL 6.33 01/13/35 197bp +0bp

SUZANO 3 1/8 01/15/32 172bp +2bp

FX Level Δ DoD

USDBRL 5.59 +0.04

USDCLP 964.93 +1.97

USDMXN 18.7 -0.04

USDCOP 4014.47 -7.43

USDPEN 3.57 +0.01

CDS Level Δ DoD

Mexico 107 (3)

Brazil 148 (0)

Colombia 209 (4)

Chile 56 0

CDX EM 97.62 0.03

CDX EM IG 101.28 0.02

CDX EM HY 93.90 0.08

Main stories recap:

Comments

· U.S. Treasury yields fell 2-3bp across most of the curve as Fed governor Waller reiterated his call for a July rate cut.

· There was limited market reaction to the U.S. economic data as housing data was reported better than expected but still weak while University of Michigan inflation expectations were lower than expected but still elevated.

· EM secondary benchmark sovereign bond spreads trended tighter across CEEMEA and LATAM while corporate bonds spreads widened as prices were little changed while Treasuries rallied.

· Argentina bonds outperformed after declines in past days as Moody’s upgraded the country’s ratings by two notches to Caa1, citing the lifting of some capital controls and the USD20bn IMF agreement.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

MNI: US TSY TICS NET FLOWS IN APR -$14.2B

- MNI: US TSY TICS NET FLOWS IN APR -$14.2B

- US TSY TICS NET L-T FLOWS IN APR -$7.8B

USDCAD TECHS: Path Of Least Resistance Remains Down

- RES 4: 1.4200 Round number resistance

- RES 3: 1.4111 High Apr 4

- RES 2: 1.3843/1.4016 50-day EMA / High May 12 and 13

- RES 1: 1.3713 20-day EMA

- PRICE: 1.3688 @ 15:55 BST Jun 18

- SUP 1: 1.3540/3517 Low Jun 16 / 1.0% 10-dma envelope

- SUP 2: 1.3503 1.618 proj of the Feb 3 - 14 - Mar 4 price swing

- SUP 3: 1.3473 Low Oct 2 2024

- SUP 4: 1.3410 1.764 proj of the Feb 3 - 14 - Mar 4 price swing

The trend needle in USDCAD points south and fresh cycle lows last week and again on Monday, reinforce a bearish theme. Short-term gains are considered corrective. Support at 1.3686, the May 26 low and a bear trigger, has been cleared, confirming a resumption of the downtrend. This maintains the price sequence of lower lows and lower highs. Sights are on 1.3517 next, envelope-based support. Resistance at the 20-day EMA is at 1.3713.

US TSYS: Late SOFR/Treasury Option Roundup

Mixed SOFR & Treasury option flow on net, underlying futures well off initial gap bid post FOMC, curves mildly steeper while projected rate cut pricing gains slightly on longer dates vs. this morning's levels (*) as follows: Jul'25 at -2.6bp (-3.6bp), Sep'25 at -18.7bp (-17.7bp), Oct'25 at -31.6bp (-29.1bp), Dec'25 at -48.2bp (-45.1bp).

- SOFR Options:

- +3,000 SFRH6 95.50 puts, 3.0 vs. 96.325/0.10%

- +2,500 SFRZ5 96.25/96.37/96.62/96.75 call condors, 1.75

- -1,000 SFRZ5 96.12 straddles, 42.5

- +4,000 SFRU5 95.68/95.81/96.00/96.12 put condors, 4.5

- +2,000 SFRZ5 95.75 puts, 3.75

- -5,000 SFRN5 95.68/95.81 put spds, 1.75 ref 95.89

- Pit/screen over +55,000 SFRU5 95.50/95.62 put spds, .25 ref 95.86, bid for more

- 3,700 SFRZ5 96.25/96.50 call spds vs. 95.68 puts ref 96.115

- -3,000 0QN5 97.25/97.31 call strip vs. SFRN5 96.50/96.56 call strip, cab net 0QN over

- +4,000 SFRQ5 95.68/95.75 put spds, 2.5 ref 95.855

- +5,000 0QH6 97.25/98.00 call spds, 13.0 vs. 96.745/0.18%

- 2,000 SFRV5 96.18/96.43 call spds ref 96.09

- 2,800 SFRU5 95.93/96.00/96.06 call flys

- +3,000 SFRU5 95.56/95.62/95.68 put flys, 1.25 ref 95.86

- +12,800 SFRH6 96.50/97.00/98.00 broken call flys, 2.5 ref 96.32 to -.33

- 1,600 3QZ5 96.25/96.62/97.00 call flys, 8.0

- Treasury Options: (July serial options expire Friday)

- 5,000 FVU5 111 calls, 10.5 ref 108-07.75 to -08

- 2,500 TUN5 103.25/103.37/103.5/103.62 put condors, ref 103-22

- 1,250 FVN5 108.25/108.5/109/110 broken call condors ref 108-09.75

- 1,800 FVN5 107.25/107.75/108.25 put flys ref 108-09.5

- 2,000 USU5 114/116/118 call flys ref 114-06

- +5,000 TYQ5 110.5/111.5/112 1x3x2 call flys 4 over TYQ5 112/113/113.5 1x3x2 call flys

- +2,000 TYQ5 114.5 calls, 8

- -3,000 TYN5 110.75 calls, 16 vs 110-22.5/0.50%

- +3,000 TYN5 111.5 calls, 6

- +1,500 Wed wkly TY 110.75/111/111.25 call flys, 3.0

- +6,500 Wed wkly FV 107.5/107.75 put spds, 1 (exp today)

- +2,000 TYN5 110.5/111/111.5 call flys, 8