EM LATAM CREDIT: LATAM Credit Market Wrap

Source: Bloomberg Finance L.P.

Measure Level Δ DoD

5yr UST 3.79% -4bp

10yr UST 4.23% -5bp

5s-10s UST 43.6 -1bp

WTI Crude 64.9 -0.6

Gold 3307 +33.0

Bonds (CBBT) Z-Sprd Δ DoD

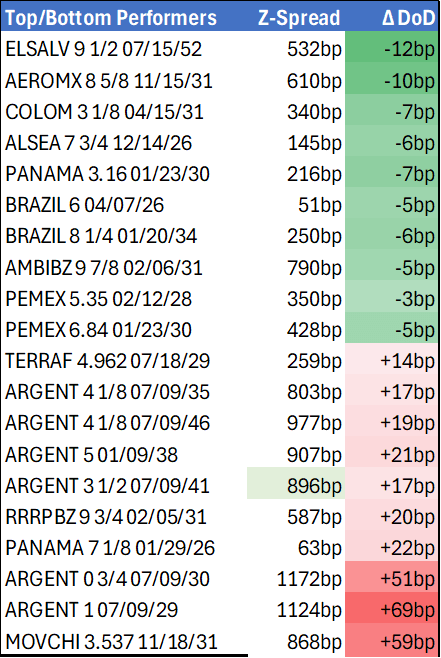

ARGENT 3 1/2 07/09/41 896bp +18bp

BRAZIL 6 1/8 03/15/34 257bp -3bp

BRAZIL 7 1/8 05/13/54 359bp -3bp

COLOM 8 11/14/35 421bp -2bp

COLOM 8 3/8 11/07/54 494bp -2bp

ELSALV 7.65 06/15/35 442bp -8bp

MEX 6 7/8 05/13/37 257bp -5bp

MEX 7 3/8 05/13/55 320bp -2bp

CHILE 5.65 01/13/37 151bp -1bp

PANAMA 6.4 02/14/35 309bp -3bp

CSNABZ 5 7/8 04/08/32 591bp +3bp

MRFGBZ 3.95 01/29/31 291bp +3bp

PEMEX 7.69 01/23/50 616bp -2bp

CDEL 6.33 01/13/35 215bp +1bp

SUZANO 3 1/8 01/15/32 180bp -3bp

FX Level Δ DoD

USDBRL 5.43 -0.06

USDCLP 931.46 -9.18

USDMXN 18.8 -0.06

USDCOP 4087.62 -10.65

USDPEN 3.54 -0.01

CDS Level Δ DoD

Mexico 108 (0)

Brazil 149 (3)

Colombia 222 (3)

Chile 53 (1)

CDX EM 97.51 0.21

CDX EM IG 101.20 0.07

CDX EM HY 93.69 0.27

Main stories recap:

Comments

· U.S. equity indexes moved higher as trade negotiators appeared to move closer to completing trade deals while congress raced to meet President Trump’s July 4th deadline for a budget agreement.

· U.S. Treasury yields fell 3-6bp across the curve as Treasury Secretary Scott Bessent signaled less interest in issuing long maturity Treasuries at rate levels he described as at the wide end of the range.

· The EM primary market was quieter than last week but still active as we saw one mandate out of Asia, a Poland sovereign € dual tranche deal and a growing pipeline of GCC subordinated debt.

· EM secondary market benchmark bond spreads trended wider in both Asia and CEEMEA while in LATAM bond spreads were generally tighter.

· Argentina bucked the trend with bonds moving ½ point lower as a U.S. court ordered the country to give up its 52% stake in energy company YPF as partial payment for its USD16bn court judgement from 2023 even as the appeals process continued.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE 10-YEAR TECHS: (M5) Bear Cycle Remains Intact For Now

- RES 3: 96.501 - 76.4% of the Mar 14 - Nov 1 ‘23 bear leg

- RES 2: 96.207 - 61.8% of the Mar 14 - Nov 1 ‘23 bear leg

- RES 1: 95.960 - High Apr 7

- PRICE: 95.745 @ 14:57 BST May 30

- SUP 1: 95.415/95.300 - Low May 15 / Low Jan 14

- SUP 2: 95.275 - Low Nov 14 (cont) and a key support

- SUP 3: 94.707 - 1.0% 10-dma envelope

Aussie 10-yr futures rallied well on the RBA rate decision last week, reversing a small part of recent weakness. Recent price action pressured prices through to new pullback lows last week. Next support undercuts at 95.420 (pierced), the Feb 13 low, ahead of 95.275, the Nov 14 low and a key support. Clearance of this level would strengthen a bearish condition. To the upside, a recovery of recent losses would shift attention to resistance at 96.207, a Fibonacci retracement point.

US-JAPAN: Trump To Deliver Remarks On Nippon Steel-US Steel Deal Shortly

US President Donald Trump is shortly due to deliver remarks in Pittsburgh, Pennsylvania, where he is expected to endorse Nippon Steel's takeover of US Steel. LIVESTREAM The announcement comes as the US and Japan remain far apart on a new bilateral trade deal.

- Trump said in a Truth Social message on May 23 that the planned partnership "will create at least 70,000 jobs, and add $14 Billion Dollars to the U.S. Economy," over the next 14 months.

- Semafor writes: “The US government will get a “golden share” in US Steel …, with the power to determine who sits on the board and control over production levels. It’s a dramatic provision that could lay out a roadmap for how deals get done in the Trump administration.”

- Japanese Prime Minister Shigeru Ishiba yesterday “expressed determination today to defend rules-based, free and multilateral trade systems and work on expanding the main Asia-Pacific trade group”, per AP.

- Ishiba said: “High tariffs will not bring economic prosperity. A prosperity built on sacrifices by someone or another country will not make a strong economy.”

- AP notes: “His comment comes as Japan’s chief tariff negotiator Ryosei Akazawa travels to Washington, D.C., for a fourth round of talks aiming to convince the U.S. to drop all recent tariff measures. So far Japan has not been successful in gaining U.S. concessions and is reportedly considering purchases of more U.S. farm products and defense equipment as bargaining chips.”

- Ishiba said after a call with Trump yesterday, “[we now] deeper understanding about each other,” but noted to reporters there has been no change to Japan’s position on the tariffs.

MACRO OUTLOOK: MNI US Macro Weekly: Jury’s Still Out On Q2 Downturn

We've just published our US Macro Weekly - Download Full Report Here

While the past week may be remembered for court decisions suspending the majority of the White House’s tariffs, it also brought further data evidence that the US economy did not fall off a cliff at the start of Q2.

- Consumer surveys (UMichigan, Conference Board) showed a downtick in consumer inflation expectations and improved sentiment, reflecting the US-China trade de-escalation on May 12.

- And while updated GDP data showed downwardly revised Q1 domestic demand, April personal consumption slowed but remained positive as underlying income growth remained solid.

- Likewise, though core durable goods orders retreated from Q1, a clear dropoff at the start of Q2 was not in full evidence. Regional Fed surveys signaled that activity stabilized in April-May, albeit at relatively weak levels, and labor market data pointed to incremental rather than sharp weakness.

- The point was underlined by the Atlanta Fed's nowcast for Q2 GDP growth which jumped to 3.84% on Friday from 2.18% in its May 27 update. Even if dramatic upgrade was due to a lower trade deficit in April as tariff front-running reversed, final domestic demand is still expected to be robust overall.

- Of course, things can change quickly: note Friday’s apparent re-escalation in US-China trade tensions and the temporary nature of the judicial tariff freeze (which in any case looks to be circumvented by the Trump administration), as well as the July “reciprocal” tariff negotiation deadline continuing to loom large.

- For the moment though, while uncertainty looks to be a constant, the data aren’t (yet) showing the degree of deterioration that had until recently been feared.

- Next week’s data highlights include key checkpoints for May, including ISM Manufacturing and Services surveys (which look likely to show some recovery versus April) and the US Employment report.

- Nonfarm payrolls growth is expected to moderate in May after a surprisingly robust 177k in April, with consensus currently around the 130k mark. The unemployment rate meanwhile is seen holding at 4.2% for what would be a third consecutive month.