EM LATAM CREDIT: LATAM Credit Market Wrap

Source: Bloomberg Finance L.P.

Measure Level Δ DoD

5yr UST 3.98% -1bp

10yr UST 4.39% -0bp

5s-10s UST 40.3 +1bp

WTI Crude 74.9 +0.0

Gold 3366 -22.3

Bonds (CBBT) Z-Sprd Δ DoD

ARGENT 3 1/2 07/09/41 926bp +22bp

BRAZIL 6 1/8 03/15/34 259bp -1bp

BRAZIL 7 1/8 05/13/54 360bp +2bp

COLOM 8 11/14/35 414bp +2bp

COLOM 8 3/8 11/07/54 494bp +1bp

ELSALV 7.65 06/15/35 445bp +3bp

MEX 6 7/8 05/13/37 257bp -0bp

MEX 7 3/8 05/13/55 320bp +1bp

CHILE 5.65 01/13/37 147bp +0bp

PANAMA 6.4 02/14/35 304bp +2bp

CSNABZ 5 7/8 04/08/32 571bp +8bp

MRFGBZ 3.95 01/29/31 275bp +1bp

PEMEX 7.69 01/23/50 639bp -1bp

CDEL 6.33 01/13/35 207bp +1bp

SUZANO 3 1/8 01/15/32 186bp -3bp

FX Level Δ DoD

USDBRL 5.50 +0.00

USDCLP 944.71 -0.48

USDMXN 19.0 +0.02

USDCOP 4068.75 -32.58

USDPEN 3.58 -0.03

CDS Level Δ DoD

Mexico 108 3

Brazil 158 5

Colombia 227 5

Chile 56 2

CDX EM 96.97 (0.11)

CDX EM IG 101.03 (0.13)

CDX EM HY 92.99 (0.27)

Main stories recap:

Comments

· Treasury yields dropped a few bp early on and then continued lower as we saw weak U.S. housing data but then the direction reversed going into the FOMC meeting.

· The FOMC left the policy rate unchanged as expected and lowered their forecast for economic growth while raising their estimate for inflation. The average rate projection was for two rate cuts this year but with a wide disparity in views from the committee.

· Equity indexes moved in a narrow range as people contemplated whether the U.S. would take a more active role in the Iran-Israel war.

· In the EM primary market, we saw a couple of Asia mandate announcements while in CEEMEA and LATAM there was no new issue activity today.

· In the EM secondary market, there was a widening trend that began in Asia and continued through to CEEMEA and then on to LATAM.

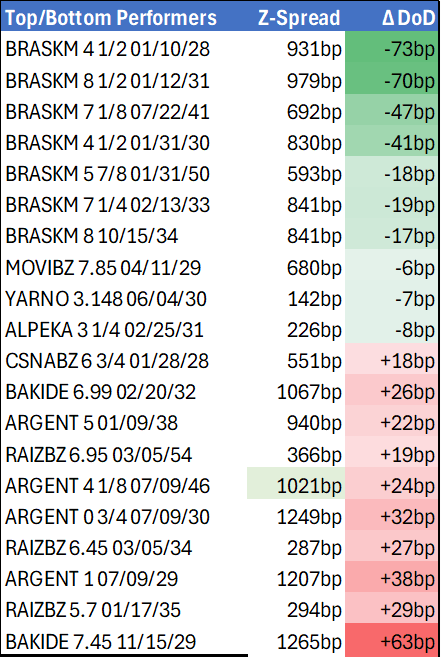

· LATAM spreads generally widened about 2-5bp. Braskem bonds outperformed, moving 1-3 points higher despite any news regarding the potential debt restructuring.

· Raizen bonds underperformed, moving almost 2 points lower in the wake of Fitch lowering its outlook for the ‘BBB’ rated Brazil ethanol processor and gasoline distribution company to negative.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

USDCAD TECHS: Corrective Cycle

- RES 4: 1.4296 High Apr 7

- RES 3: 1.4111 High Apr 4

- RES 2: 1.4024 50-day EMA

- RES 1: 1.4016 High May 12 / 13

- PRICE: 1.3925 @ 16:44 BST May 19

- SUP 1: 1.3814/3751 Low May 8 / 6 and the bear trigger

- SUP 2: 1.3744 76.4% retracement of Sep 25 ‘24 - Feb 3 bull run

- SUP 3: 1.3696 Low Oct 10 ‘24

- SUP 4: 1.3643 Low Oct 9 ‘24

Despite the latest move higher, the trend condition remains bearish in USD/CAD and Monday’s weakness confirms recent strength as corrective. A fresh cycle low on May 6 reinforces the bearish theme. A resumption of weakness would open 1.3744, a Fibonacci retracement. Note that moving average studies are in a bear mode position, highlighting a dominant downtrend. Key resistance is seen at 1.4024, the 50-day EMA.

US TSYS: 30Y Holds 5% Level Amid Broad Post-Downgrade Rally

Treasuries recovered from early weakness to close flat/stronger Monday, with bull steepening in the curve.

- Following on from Friday's post-close surprise downgrade of the US's AAA credit rating by Moody's, yields rose sharply in the early going.

- While over the weekend White House officials shrugged off Moody's decision, there was significant attention on the apparently deteriorating fiscal trajectory overnight as House Republicans cleared a procedural hurdle to get the "Big, Beautiful" tax bill closer to completion.

- 30Y yields notably touched their highest since Nov 1 2023 (5.0353%) - up 13.5bp from Friday's ratings downgrade announcement - before an impressive reversal lower on the day (just 1+bp up from pre-downgrade).

- Despite little in the way of headline catalysts - China expressed displeasure with the US's guidance against the use of some Huawei chips, bringing a brief risk-off reaction - Treasuries rallied alongside equities for the rest of the session (the TY upturn started with the equity cash open).

- We heard from multiple Fed speakers, including Bostic, Jefferson, Williams, and Kashkari, all of whom reiterated the FOMC's patient approach on cuts amid economic uncertainty, and Williams and Bostic in particular suggesting that the next cut wouldn't seriously be contemplated until after the summer. Reaction was limited however given the market's already-low implied probability of a cut before September.

- Data was relatively thin - Conference Board leading economic index had its sharpest drop since 2023 but avoided an outright recession signal.

- Latest levels: the 2-Yr yield is down 3.1bps at 3.9681%, 5-Yr is down 3.2bps at 4.0611%, 10-Yr is down 2.2bps at 4.4553%, and 30-Yr is down 2.6bps at 4.9183%.

- Jun 10-Yr futures (TY) down 2.5/32 at 110-08 (L: 109-20 / H: 110-09)

- Tuesday's schedule includes the Philly Fed nonmanufacturing survey along with another slew of Fed speakers, including Collins, Barkin, Musalem, Kugler, Hammack and Daly.

AUDUSD TECHS: Trend Structure Remains Bullish

- RES 4: 0.5682 High Nov 12 ‘24

- RES 3: 0.6550 61.8% retracement of the Sep 30 ‘24 - Apr 9 bear leg

- RES 2: 0.6528 High Nov 29 ‘24

- RES 1: 0.6515 High May 7

- PRICE: 0.6463 @ 16:42 BST May 19

- SUP 1: 0.6356 50-day EMA

- SUP 2: 0.6275 Low Apr 14

- SUP 3: 0.6181 Low Apr 11

- SUP 4: 0.6116 Low Apr 10

The trend condition in AUDUSD is unchanged, it remains bullish. The May 13 rally signals the end of the recent corrective pullback and attention is on key resistance at 0.6515, the May 7 high. Note that moving average studies remain in a bull-mode position, highlighting an uptrend. A resumption of the trend would open 0.6550, a Fibonacci retracement. Key support to monitor is 0.6356, the 50-day EMA.