FED: Largely Dovish Tilt Since Pre-September Meeting But Divisions Persist (2/3)

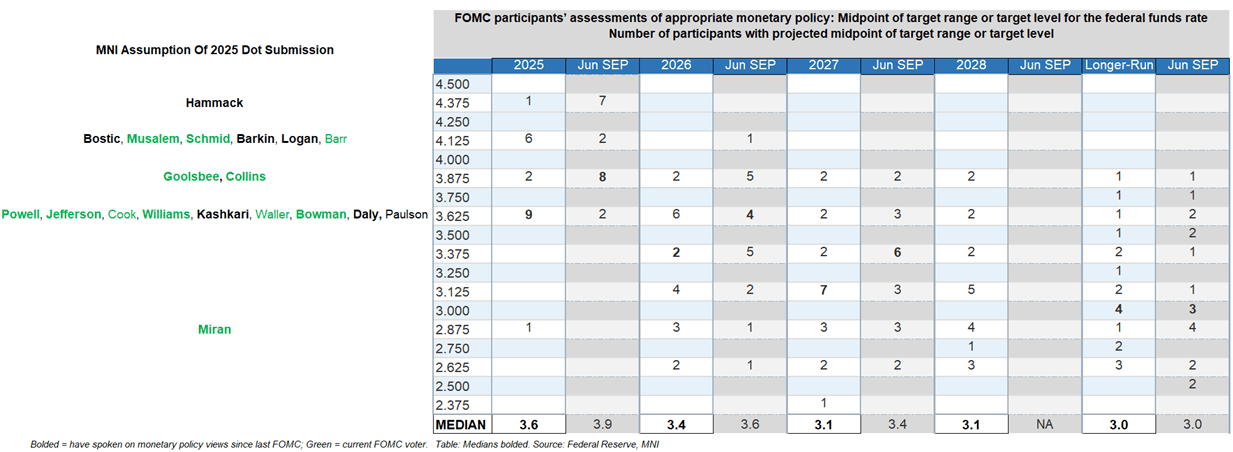

In the September Dot Plot, there were 9 rate dots at 3.9% or above for this year and 10 at 3.6% or below, making the latter the 2025 median. We presume that includes the leadership of the Committee including Chair Powell. But interesting that one saw no cuts this year (and it wasn't a voting dissenter) and 6 see this as the last reduction. For 2026 the highest dot has shifted lower by 25bp to 3.9%, but again it's a fairly split median. 8 members are at 3.6% or higher (was 10 previously), with 11 at 3.4% or below (vs 9 prior). And while the longer-run median was unchanged at 3.00%, the new distribution and post-meeting participant commentary point to rising longer-run neutral rate estimates. See below for our assumption of participants’ 2025 submissions.

- Since the meeting, the rest of the FOMC largely following their own pre-meeting scripts albeit most expressed a slightly more dovish tilt in keeping with the shift in the broader Committee’s perception of the balance of risks. We go through all the key commentary in our PDF preview (sent separately). All participants acknowledged that recent labor market indicators have signaled rising risks to that side of the dual mandate, and largely noted that tariff impacts on inflation were more limited than foreseen, though the conclusions differed on what that means for monetary policy.

- Current voters Musalem and Schmid for example supported the September cut, but it’s doubtful they anticipate support for any more this year given inflation risks. Non-2025 voters Hammack, Logan, and Bostic also suggested they didn’t see any further cuts this year, with Bostic the most open-minded of the three about another easing.

- As for the other two 2025 regional voters, Goolsbee cautioned against too much front loading of cuts, while Collins eyes “a bit” more easing – suggesting that they may only see one further cut this year.

- But a majority of the 12-member FOMC voters – including 7 of 8 permanent voters – are likely to see at least another 2 cuts this year. Waller, Bowman, and (especially) Miran are the strongest proponents of further cuts, but Powell, Jefferson, Cook, and Williams are all likely in the camp of two further cuts. The latter are joined by Kashkari and Daly, and, in an assumption, Paulson who is yet to speak on monetary policy since joining the FOMC this summer.

- Among the 19 we have the least conviction on dot placement for Barkin, Barr, and Goolsbee, but given the numbers we think they are either on the side of 1 or 2 further cuts.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSY FUTURES: BLOCK: Dec'25 10Y Ultra-Bond Buy

- +3,500 UXYZ5 115-30.5, buy through 115-30 post time offer at 1115:38ET, DV01 $320,000.

- The 10Y ultra contract trades 115-31 last (+9.5)

US 10YR FUTURE TECHS: (Z5) Bullish Structure

- RES 4: 114-10 High Apr 7 (cont.)

- RES 3: 114-00 Round number resistance

- RES 2: 113-26+ 2.764 proj of the Jul 15 - 22 - 28 price swing

- RES 1: 113-21+ High Sep 5

- PRICE: 113-16+ @ 16:14 BST Sep 8

- SUP 1: 112-28+/112-07+ Low Sep 5 / 20-day EMA

- SUP 2: 111-24 50-day EMA

- SUP 3: 111-13+ Low Aug 18 and a key support

- SUP 4: 110-25 Low Aug 1

Treasury futures rallied sharply higher on Friday and the contract remains closer to its recent highs The move higher highlights an acceleration of the uptrend. Note too that moving average studies are in a bull-mode position, highlighting a dominant uptrend. This paves the way for an extension through 113-21 next (piered), the 2.618 projection of the Jul 15 - 22 - 28 price swing. Initial firm support to watch is 112-07+, the 20-day EMA.

FED: US TSY 13W AUCTION: NON-COMP BIDS $2.256 BLN FROM $82.000 BLN TOTAL

- US TSY 13W AUCTION: NON-COMP BIDS $2.256 BLN FROM $82.000 BLN TOTAL