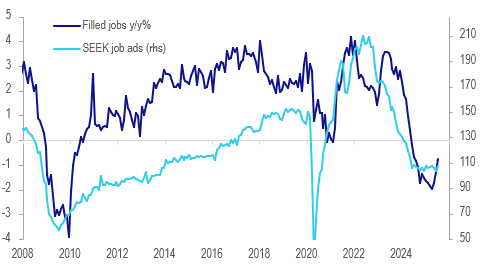

NEW ZEALAND: Labour Market May Be Stabilising

NZ filled jobs rose for the second straight month in July, which is a tentative sign of some stabilisation in the labour market but the increases remain slight. July was up 0.2% m/m after 0.1% but was still down 0.7% y/y but an improvement from June’s -1.3% y/y and April’s -2.0% y/y. Q3 labour market data is not out until 5 November and so August/September filled jobs will be monitored closely (29 Sep/28 Oct).

- SEEK reported a 3.9% m/m rise in July job ads to be down 0.5% y/y after -2.4% y/y in June and -30.7% in August 2024. It noted that vacancy levels have been going sideways for 10 months suggesting no further labour market deterioration - another sign of stabilisation but at weak levels.

- The services sector drove the increase in filled jobs rising 0.3% m/m. Primary industries also hired (+0.5%), while goods-producers cut by 0.1% m/m. Over the last year, construction, admin services and manufacturing drove job shedding, while the health and education sectors saw an increase in employment.

- Only the 35-39 year old age group has seen an increase in employment over the last year (+2.2% y/y), while 15-19 years fell 8.5% y/y and 20-24 years 3.2% y/y.

NZ labour market

Source: MNI - Market News/SEEK/Statistics NZ

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GOLD: Gold Weaker As Trade Worries Ease, Event Risks High This Week

Gold prices fell 0.7% to $3314.61/oz on Monday as trade risks dissipated with the US-EU trade deal and the start of US-China talks in Stockholm. The higher US dollar (BBDXY USD +0.8%) and US yields also pressured bullion. It is now only 0.4% higher this month and down 3.6% from the July 22 peak. Gold has started today slightly lower at $3312.8.

- Trade is just one event this week that could drive direction. There are also the Fed’s decision on July 30, Q2 GDP & June PCE July 30 & 31, and US July payrolls August 1. A dovish Fed or weak US data would be supportive of gold prices.

- Bullion fell to a low of $3301.85, below initial support at $3323.2 (50-day EMA), before recovering somewhat. The bear trigger is at $3248.7 but short-term weakness continues to be seen as corrective. Moving average studies are still in a bull-mode position highlighting the dominant uptrend. Initial resistance is at $3439, 23 July high.

- Silver was flat on Monday at $38.169 and has started today in line with this. It is up 5.7% this month and trend conditions remain bullish. Initial resistance is at $39.655 with support at $37.809, 20-day EMA. The sequence of higher highs and higher lows continues.

- Equities were mixed with the S&P flat but Euro stoxx down 0.3%. Oil prices rose sharply following news of US pressure on Russia to stop fighting in Ukraine. WTI rose 2.8% to $66.98/bbl. Copper fell 2.9%.

JGBS: Futures Unchanged Overnight, FOMC (Wed) & BoJ Decision (Thu)

In post-Tokyo trade, JGB futures closed unchanged compared to settlement levels, after US tsys were slightly underwater all day. Unwinding of haven trades, risk-on flows, and set up for this week's auctions weighed.

- Trading was subdued ahead of an event- and data-filled week. However, trade optimism after the weekend news of an EU-U.S. trade agreement, on top of last week's framework with Japan, did lift the S&P 500 and NASDAQ to more record highs.

- It’s virtually unanimous that there will be two dissents in favour of a cut at Wednesday’s FOMC meeting, with Gov Waller widely expected to do so and Gov Bowman also likely (among analysts who expressed an opinion on this).

- Kyodo News via BBG - "Japan's long-term interest rates fell due to speculation that the Bank of Japan will refrain from further interest rate hikes at its monetary policy meeting to be held on the 30th and 31st. Selling of the yen and buying of the dollar was dominant, due to the widening interest rate gap between Japan and the United States."

- Today, the local calendar will be empty apart from 2-year supply.

AUSSIE BONDS: Little Changed, Q2 CPI & FOMC On Wednesday

ACGBs (YM +0.5 & XM -0.5) are little changed after US tsys finished with modest losses ahead of Wednesday's widely expected steady FOMC rate announcement.

- It’s virtually unanimous that there will be two dissents in favour of a cut at this meeting, with Gov Waller widely expected to do so and Gov Bowman also likely.

- Cash ACGBs are unchanged with the AU-US 10-year yield differential at -5bps.

- The focus of this week will be Wednesday's Q2 CPI data, which is expected to show the underlying trimmed mean measure making further progress towards the band midpoint of 2.5%. Bloomberg consensus is forecasting a 0.7% q/q rise, bringing the annual rate to 2.7% after 0.7% & 2.9% in Q1. This is slightly higher than the RBA's May Q2 forecast of 2.6%. Services developments will also be monitored. The RBA is expected to cut rates 25bp on August 12.

- The bills strip is slightly stronger, with pricing flat to +1.

- RBA-dated OIS pricing is slightly softer across meetings today. A 25bp rate cut in August is given a 90% probability, with a cumulative 59bps of easing priced by year-end.

- This week, the AOFM plans to sell A$1000mn of the 2.25% 21 May 2028 bond today and A$1200mn of the 2.75% 21 June 2035 bond on Friday.