US DATA: Labor Secretary Wants NFP Report Publication "As Soon As" Gov't Reopens

Following the non-release of September's nonfarm payrolls data, Labor Sec Chavez-Deremer in a Fox Business appearance didn't directly answer the host's initial question about whether the report would be released after the gov't reopens ("certainly what we want to see at BLS is to have those numbers out"). Then the host followed up, directly asking: "just to be clear, when would you expect to release the September jobs numbers"

- Chavez-Deremer replied: "As soon as this government opens, I hope that the Democrats understand, as soon as they open this government, we want to get these numbers out so that we can determine what this market looks like, and we can work hard again to fulfill the needs of the American people. We need that data. We need the accurate data points. It's a 30 day snapshot, certainly, but we can see over the last six months that the economy is growing. "

- Note there wasn't really a tip-off in the conversation as to what the actual September data might show, rather a discussion of longer-term trends etc.

- Historic precedent albeit limited suggests it would be at least a few days after government reopening before the NFP report is released.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BOE: Lombardelli: Neutral could be close to (or at) 4%

Lombardelli's comments are significant. She is saying that neutral could be close to (or at 4%). And she is deviating from the wider Bank guidance that rates are still "meaningfully restrictive." Highlights on her views below:

- In August "I judged it appropriate to pause the reduction of monetary restriction, due to my concerns about the current and expected above-target rates of underlying inflation and my judgements about the balance of supply and demand in the economy. I preferred to maintain the level of monetary restriction for longer rather than continue to reduce it at the previous pace."

- "At the time of the August decision headline inflation was 3.6% and it is expected to remain roughly between 3.5 and 4.0% for the remainder of this year. This is driven in part by inflation in food and energy - the most salient prices - and comes after a long period of relatively high inflation. This increases the risk of an inflation persistence scenario such as the one we considered in May."

- "It is less clear if the disinflation process is continuing in services prices"

- "While previous policy restrictiveness continues to weigh on the economy, I am less confident that the current policy stance as embodied in the market curve continues to be meaningfully restrictive. At the time of the August MPC vote, we had reduced rates by 100 basis points and I judged that there might not be that much further to go before the current policy stance is effectively neutral. Looking at history, it’s plausible that neutral may be closer to the upper end of the 2-4% range from Bank analysis. If so, this would mean we don’t have many more rate cuts to go as we potentially approach the end of the cutting cycle. I am not predicting that we are already at neutral, but nor am I confident that if we reduce restrictiveness much further we will still be sufficiently restrictive to return inflation to target sustainably."

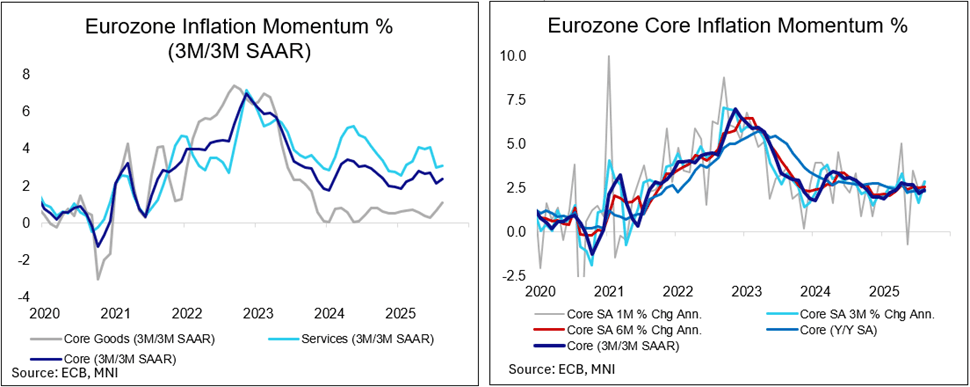

EUROPEAN INFLATION: MNI Eurozone Inflation Insight – August 2025

We have published the MNI Eurozone Inflation Insight, with the full report found here.

- Eurozone August headline HICP inflation printed marginally below consensus expectations on Tuesday, at 2.05% (cons 2.1) for essentially unchanged from the 2.04% in July.

- As we flagged in our preview ahead of country-level data, such a marginal downside surprise was not sufficient to ensure a dovish tilt in EUR rates, with markets pricing for both the September and October ECB meetings to remain largely out of play.

- A cumulative 7-8bps of cuts are currently priced to year end, which some Governing Council members appear to be leaning against.

- One of the stronger views here, but not a surprising one, was executive board member Schnabel in a Reuters interview Tuesday morning, while some other ECB officials continue to flag a further cut as a possibility – as Bank of Lithuania Chairman Simkus, also in an interview on Tuesday morning.

- ECB President Lagarde meanwhile said on Monday (Sep 1) that the Eurozone inflation goal of 2% has been met, building on her comment from the Jul 24 press conference that “Inflation is currently at our two per cent medium-term target”.

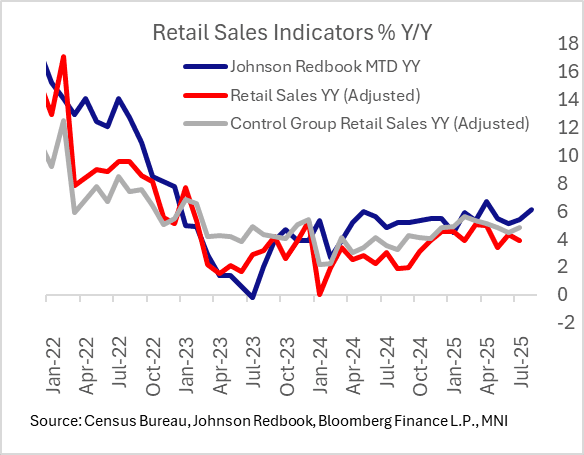

US DATA: Redbook Retail Sales Closes August Strong, "De Minimis" Noted As Factor

Johnson Redbook retail sales rang up a 6.1% Y/Y increase in August, following consecutive weekly 6.5% Y/Y gains to end the month. This brought sales close to retailers' targeted 6.2% gains for the month.

- The report notes a preliminary target for September of 6.3% Y/Y sales growth.

- The anecdotal portion of the report highlights potential shifts in shopping habits due to the recent elimination of de minimis exemptions on small value imports: "Most companies in our sample reported strength in back-to-school apparel categories, particularly for children's and juniors' clothing and shoes. Shoppers are prioritizing value and are increasingly shopping at warehouse clubs and discount stores. This trend has also been somewhat influenced by the loss of duty-free status for cheap imports priced at $800 or less in the United States. For most retailers, the August sales period concluded on Saturday, the 30th, which means that the bulk of Labor Day shopping will not be reflected in this week's report."

- August Census Bureau advance retail sales are only out on Sep 16th; there is no consensus yet but the Redbook report continues to point to fairly robust dynamics (on a nominal basis, at least). Y/Y Control Group printed 4.8% Y/Y in July vs 5.4% for Johnson Redbook.