JAPAN DATA: Labor Earnings Better Than Forecast, Supports Near Term BoJ Action

Japan Apr labor cash earnings were mostly stronger than forecast. The headline rose 3.5%y/y (against...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

CNH: USD/CNH Capped By 20-day EMA Resistance, Trump Downplays Tensions

USD/CNH spot sits near 6.8240 in early Wednesday dealings, with onshore markets returning today from the early May Labor day break (with markets out since last Friday). Ranges were fairly tight through Tuesday trade, with highs of 6.8360 coinciding with the 20-day EMA resistance point. Downside remains fairly limited at this stage, with earlier May lows, just under 6.8160, still intact. Broader USD sentiment eased as Tuesday trade unfolded (albeit with the BBDXY finishing up off lows). These trends have continued in early Wednesday dealings as Trump posted on Truth Social that he is pausing Project Freedom (re-opening Hormuz) to see if a complete and final agreement can be made with Iran. These headlines have helped USD/CNH to tick lower.

- Spot USD/CNY ended last Thursday trade at 6.8280, so little basis differential with current spot CNH levels. The CNY basket tracker was at 100.16, edging up from late Apr lows (near 99.73), consistent with slightly higher USD index levels over the same period.

- Next week's planned Xi/Trump summit continues to be in focus (set for May 14-15). Via BBG: "US President Donald Trump said he would discuss the Iran war with Chinese counterpart Xi Jinping during their summit next week and sought to downplay tensions over the conflict."

- We have the RatingDog services PMI out today, expected at 52.0 by the consensus forecast, little changed from March's 52.1 if realized. Local media notes over the recent Labor Day holiday period, via BBG/Xinhua: "Average daily interregional passenger trips likely rose 4% from the same period last year to 305 million"

AUSSIE BONDS: Unchanged After Little Changed US Tsys, AU-US 10Y Lowest Since Feb

ACGBs (YM +0.5 & XM +0.5) are little changed after cash US tsys finished modestly richer after ISM Services prices paid comes out lower than expected, as did New Orders. Meanwhile, March JOLTS job openings vs. Feb declined less than expected while Quits and Layoffs levels surge higher.

- The ISM services index was very close to expectations in April at 53.6 as it dipped slightly from 54.0 in March to extend a drop from February's 56.1 (highest since Jul 2022).

- Cash ACGBs are unchanged with the AU-US 10-year yield differential at +54bps. At current levels, the spread is at its lowest since early February and sits just above the lower end of the 50–80bp range that has prevailed this year. This followed a sustained shift away from the tighter ±30bp band that had contained the differential from November 2022 until the breakout earlier this year.

- The bills strip is little changed across contracts.

- RBA-dated OIS pricing shows tightening across all meetings, with the probability of a 25bp hike rising from 23% for June to 77% by August and 140% by December 2026.

- Today, the local calendar will be empty.

- The AOFM plans to sell A$1000mn of the 4.25% 21 March 2036

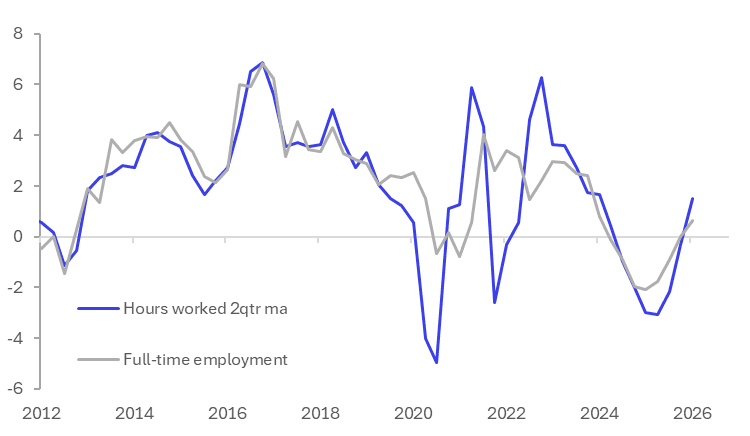

NEW ZEALAND: Ongoing Labour Market Recovery Modest, Wages Contained

The labour market continued its modest recovery in Q1. The unemployment rate was lower, there was job growth in both full-time (FT) and part-time (PT) sectors and hours worked were higher. While the unemployment rate dip to 5.3% was in line with the RBNZ’s February forecast, employment growth was softer. Wage growth also remained contained, thus labour market conditions argue for the RBNZ to remain on hold but the onset of the Iran War has complicated decision making. The next announcement is 27 May.

- Employment rose 0.2% q/q to be up only 0.4% y/y after 0.5% q/q & 0.2% y/y. The RBNZ projected in February an increase of 0.4% & 0.7%. The majority of job growth was in part-time positions suggesting employer caution. PT rose 0.5% q/q with FT up 0.1% q/q.

NZ employment y/y%

Source: MNI - Market News/LSEG

- The unemployment rate eased 0.1pp to 5.3% as the participation rate fell 0.1pp to 70.4%. Also the number of unemployed was down 1.2% q/q, the largest quarterly decline since Q4 2021. However, youth not in employment or education/training rose 1.1pp to 14.4% in Q1, which as a lead indicator signals ongoing labour market weakness.

- Hours worked increased 0.8% q/q to be up 2.2% y/y. The underutilization rate remains high though at 12.9%.

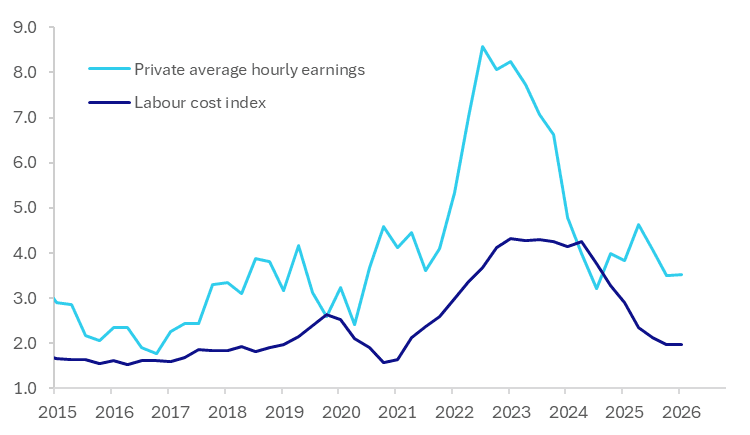

- Private wages including overtime rose 0.4% q/q, as expected, but excluding overtime were stronger at 0.5% q/q but only 2.0% y/y unchanged from Q4. Wage growth is currently not a problem for the inflation outlook and with labour demand still moderate, high pay outcomes are unlikely.

- Private average hourly earnings were also moderate up 0.2% q/q and 3.6% y/y. Total labour costs rose 0.5% q/q & 2.0% y/y.

NZ wages y/y%

Source: MNI - Market News/LSEG