FED: Kugler: Appropriate To Hold Rates As Inflation Likely To Accelerate

Gov Kugler continues to sound very patient on the next rate easing in a speech today - we have her penciled in as one of the 7 FOMC members who don't see any rate cuts this year. In short, she remains concerned about the incoming inflation impact from tariffs, and elevated short-run inflation expectations. Keep in mind she'll almost certainly be replaced in January when her term as governor expires.

- On her view that rates should be on hold "for some time": "Inflation.. remains above the FOMC's 2 percent goal and is facing upward pressure from implemented tariffs. Moreover, I judge that inflation is likely to increase further as tariff effects build up during the rest of the year...Given the stability in the employment side of our mandate, with the unemployment rate still at historically low levels, elevated short-run inflation expectations, and goods inflation rising due to the upward pressure from tariffs, I find it appropriate to hold our policy rate at the current level for some time. This still-restrictive policy stance is important to keep longer-run inflation expectations anchored. "

- She also highlights signs of tariff passthrough in this week's CPI and PPI reports (see MNI's Inflation Insight on this topic), and in her speech offers several reasons to expect "that larger effects of tariffs are still coming": "I see firmer core goods inflation as already partially reflecting the pass-through of increased tariffs, which has been shown by research done at the Fed.18 In addition, CPI and PPI reports released in the past two days show that increases in core goods prices were more broad-based in the month of June."

- Re the reasons to expect future price increases: "While many forecasters may have been expecting a sooner and sharper increase in overall inflation, there are many reasons to think that larger effects of tariffs are still coming. First, businesses built up inventories ahead of anticipated tariff increases, giving them leeway to still sell goods at pre-tariffed prices. Second, given the many changes in implemented tariff policies, businesses may not yet be passing the higher tariffs to their selling prices because they are waiting for greater clarity. Third, businesses, especially larger ones, may also be waiting to capture market share from others that hike prices sooner. Fourth, the current environment of still-elevated short-run inflation expectations makes it easier for workers to seek higher wages and business to charge higher prices, which could increase the persistence of price hikes going forward. Fifth, tariff rates could increase further, as seen in newly proposed reciprocal tariffs for several countries and the new tariffs on copper introduced last week, putting further upward pressure on prices."

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EQUITY TECHS: E-MINI S&P: (U5) Trend Condition Remains Bullish

- RES 4: 6200.00 1.500 proj of the Apr 7 - 10 - 21 price swing

- RES 3: 6172.50 High Feb 24

- RES 2: 6134.00 High Feb 26

- RES 1: 6128.75 High Jun 11 and the bull trigger

- PRICE: 6070.25 @ 14:31 BST Jun 17

- SUP 1: 5979.00/5890.99 Low Jun 13 / 50-day EMA

- SUP 2:5811.50 Low May 23

- SUP 3: 5645.75 Low May 7

- SUP 4: 5500.00 Low Apr 30

The trend condition in S&P E-Minis is unchanged, it remains bullish and the contract traded to a fresh cycle high last Wednesday, reinforcing current bullish conditions. For now, the most recent pullback is considered corrective. The contract has pierced support at 6000.18, the 20-day EMA. A clear breach of this average would expose the 50-day EMA, at 5890.99. Key short-term resistance has been defined at 6128.75, the Jun 11 high.

SOFR OPTIONS: BLOCK: Dec'25 SOFR Call Condor Sale

- -9,000 SFRZ5 97.00/97.25/97.75/98.00 call condors, 0.75 ref 96.09.5 at 0926:18ET

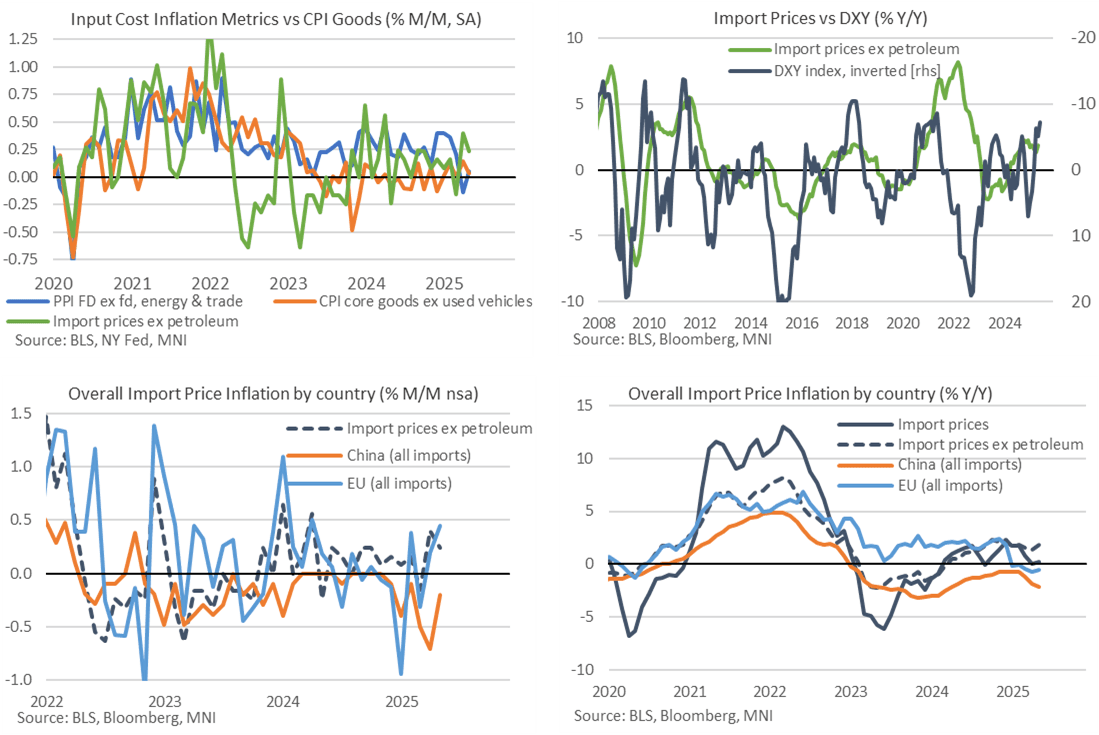

US DATA: Import Prices Show Most Exporters Didn’t Take Tariff “Hit” In Apr/May

- Import prices were a little stronger than expected in May at 0.0% M/M (cons -0.2) after 0.1% in April whilst ex petroleum prices increased 0.2% M/M (cons 0.1) after 0.4% in April.

- For ex-petroleum prices, it’s a solid increase after the 0.4% in April was its strongest in twelve months. It saw the Y/Y accelerate from 1.36% to 1.8% Y/Y for its highest since February and with some further increases possible judging by USD weakness - see charts below.

- Whilst these data do not take account of tariffs (which are considered taxes in the national accounts), they importantly point to little sign of exporters taking part of the “hit” of US tariffs in the form of lowering their prices to remain more competitive against countries with lower tariff rates.

- That’s on a widespread basis, and likely a factor of the baseline ‘reciprocal’ 10% tariff rates seen for many countries during the current 90-day pause. There are however signs of some discounting from those that have been targeted more heavily, with China a clear standout.

- For example, overall import prices from China fell -0.2% M/M in May after a heavy -0.7% M/M in April whereas prices from the EU increased 0.4% M/M after 0.2% M/M.

- Overall declines in Canada (-1.0%) and Mexico (-0.3%) have to be taken with caution, as this was driven by fuel prices, with non-manufacturing import prices +0.7% M/M from Canada and 0.0% M/M from Mexico.

- China import price inflation stands at -2.1% Y/Y (weakest since Apr 2024) whilst EU import price inflation lifted from -0.8% to -0.5% Y/Y after what had been its weakest since May 2020.