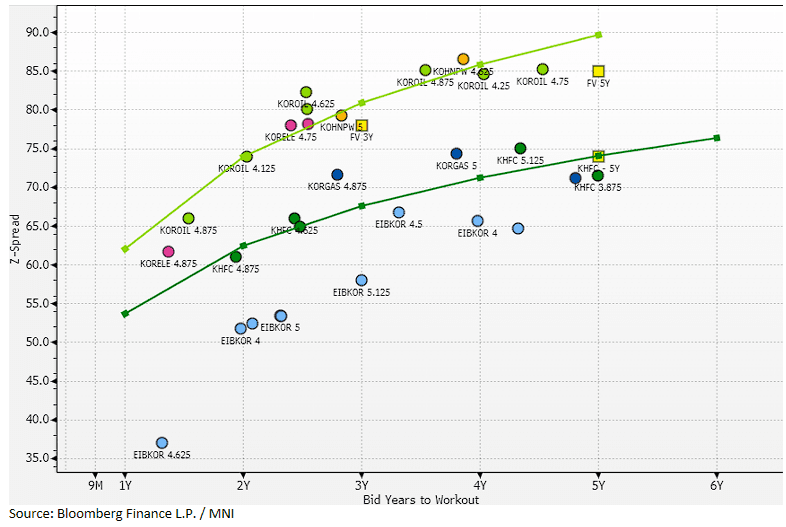

EM ASIA CREDIT: Korea Oil: New $ mandate FV estimate

(KOROIL, Aa2/AA/NR)

Mandate: $benchmark, 3Y FIXED/FRN and/or 5Y FIXED/FRN

FV on FIXED: We estimate T+49bp area for a 3Y and T+48bp area for a 5Y

Korea Oil (KOROIL, Aa2/AA) has mandated banks for a dual-tranche $ deal, including $benchmark 3Y and/or 5Y either as FIXED of FRN. Investor calls started yesterday, with a deal expected next week. Korea Oil last came to the market in March. We take a look at the possible FV of a 3Y and 5Y FIXED deal.

In terms of comparable issuers we take into account the Korea Oil curve, which is well-developed, as well as Korea Hydro (KOHNPW,Aa2/AA), Korea Electric (KORELE, Aa2/AA) and recent deals from Korea Housing Finance Corp (KHFC, Aa2/AA), Korea Development Bank (KDB,Aa2/AA/AA-) and Export-Import Bank Korea (EIBKOR, Aa2/AA/AA-). We focus on the more liquid bonds issued in the last 2 years.

In terms of fair value, we see a 10-15bp spread differential to the KHFC curve based on the existing curve, and use the recent 5Y deal as an anchor point. This would give a z-spread of around z+85bp (T+48bp) at 5Y. In terms of a 3Y deal, we see fair value around z+78bp (T+49bp), a few basis points inside the existing Korea Oil curve.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BONDS: NZGBs: Gap Richer After RBNZ Gives Dovish Guidance

NZGBs gap 9-12bps richer after the RBNZ cut the OCR by 25bps to 3.0%, as expected (4–2 vote; some favoured a 50bp cut).

- Forward guidance sees the OCR averaging 2.71% in 4Q 2025, 2.56% in 2Q 2026, and 2.59% in 3Q 2026 (down from May’s trough forecast of 2.9%). Indicates scope for further rate cuts if inflation pressures ease; forecasts imply a good chance of two more 25bp cuts.

- GDP seen contracting 0.3% q/q in 2Q 2025 but growing 0.3% q/q in 3Q 2025. Risks to the outlook remain both to the upside and downside.

- Bottom line: RBNZ delivered a widely expected rate cut to 3%, signalled a lower future OCR path, and left the door open for further easing if inflation moderates. Markets responded with a weaker NZD and higher local equities.

- Swap rates are 9-12bps lower after the decision.

- RBNZ dated OIS pricing has shunted softer for meetings beyond August. Pricing is 14-18bps softer out to July 2026. 31bps of cumulative easing is priced by November 2025.

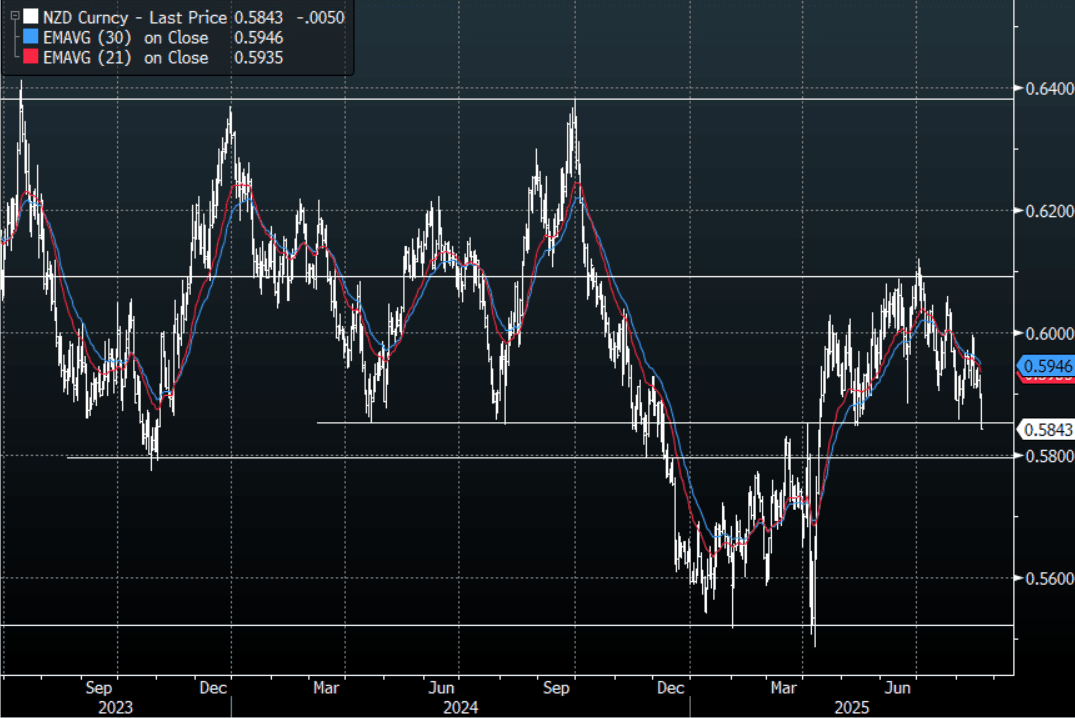

NZD: NZD/USD - Probing Pivotal Support After The RBNZ

With policy makers signaling there is scope to lower borrowing costs further if inflation pressure ease the NZD/USD has quickly moved lower and is now testing some pivotal support. Is this enough for the NZD to break lower and reignite the momentum lower ? Together with a market that is paring back USD shorts into Jackson Hole it does leave the NZD vulnerable.

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

RBNZ SEES LOWER OCR SHOULD INFLATION EASE FURTHER

- RBNZ SEES LOWER OCR SHOULD INFLATION EASE FURTHER

- RBNZ DISCUSSED 50BP CUT, ALONGSIDE HOLD AND 25BP REDUCTION