US STOCKS: Key Day Reversal On S&P Could Signal Some Reversion

The ESU5 overnight range was 6357.50 - 6468.50, Asia is currently trading around 6353. The momentum higher in risk could not be maintained and a higher than expected PCE print overnight brought the hawkish tone of the Fed back into view. This saw the early Equity rally on better earnings stall and quickly move lower again. That looks like a key reversal day for US Stocks and could signal its time for risk to take a breather which opens the possibility of some reversion back to the mean. This morning has seen US futures take another leg lower as the Asian markets open soft reacting to the overnight price action, ESU5 -0.35%, NQU5 -0.45%. The broader market outside of Tech gave us an inkling of what was to come and continue to struggle, Regional US Banks - 1.20%, Russell -0.93%, Down Transports -0.41%. First support in ESU5 is towards the 6250 area, a sustained break of this level could signal a deeper correction.

- Lance Roberts(RIA) - “With markets turning in one of the best July performances ever and technical conditions overbought and extended, this setup bodes well for some caution in August and September, which tend to be weaker from a seasonality perspective.”

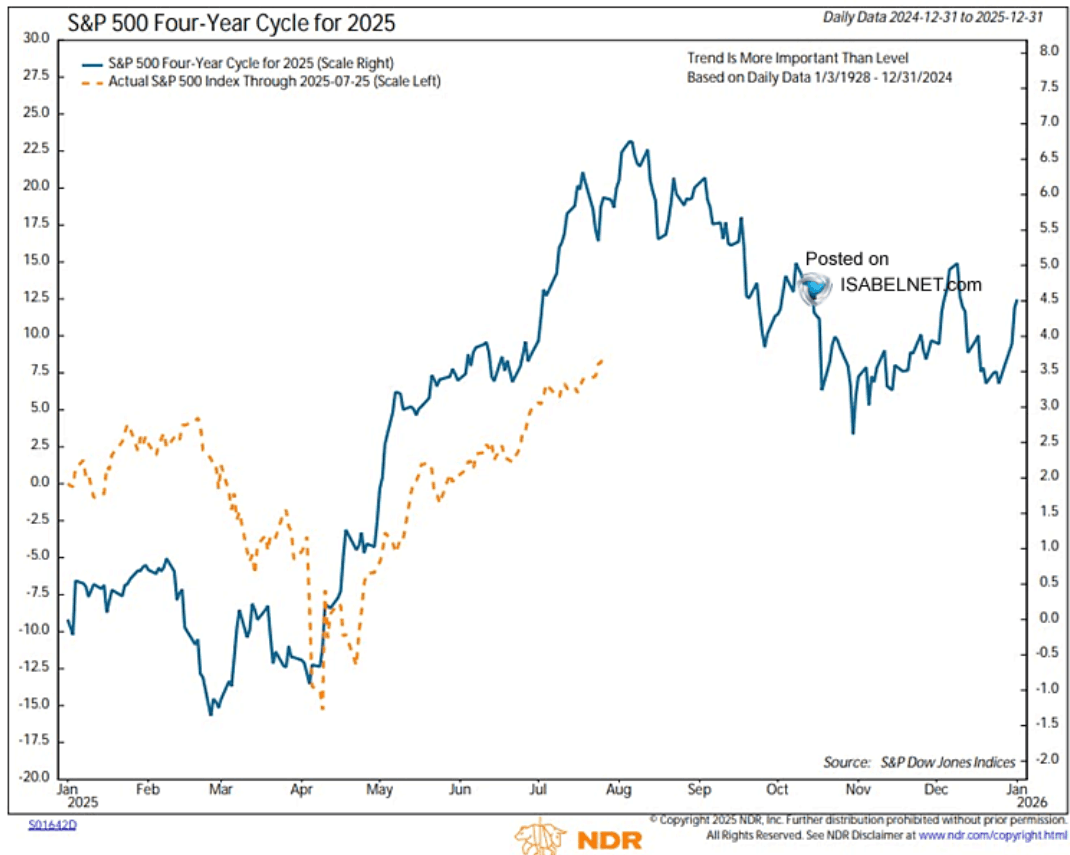

- ISABELNET on X: ”The behavior of the S&P 500—peaking in early August with a softer year-end rally—is a typical post-election year trend observed historically in US presidential election cycles” h/t @edclissold. See Fig.1 below.

- “US stocks are trading near their post-pandemic peak levels, leaving little margin for error and increasing the market's vulnerability to negative news despite ongoing optimistic drivers.”

- Daily Chartbook on X: "Market breadth (% of companies outperforming the S&P 500) is getting narrower and hitting low points more often."-HSBC Inui via @_JoshSchafer

- "There has been a lot of focus around the timing of a potential correction. These conversations will heat up during late August."-Citadel Rubner via Zerohedge

- Short-term this continues to look stretched but it's very hard to fight a market with this type of momentum. First support is back towards the 6000/6100 area.

Fig 1: S&P Post Election Seasonality

Source: MNI - Market News/@ISABELNET_SA

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE BONDS: ACGB Jun-35 Supply Faces A Lower Yield But A Similar Curve

The Australian Office of Financial Management (AOFM) will today sell A$1200mn of the 2.75% 21 June 2035 bond, issue #TB145. The line was last sold on 2 May 2025 for A$900mn. Bidding is likely to be shaped by several key factors:

- The current yield for this bond is approximately 10bps below the level of the previous auction and 60bps below the high recorded in early November 2024.

- The 3/10 yield curve is around the same level as the previous auction but sits 20bps below its recent high.

- Notably, investor sentiment toward longer-dated global bonds has improved over June.

- The inclusion of the Jun-35 line in the XM basket may also lend support to demand.

- Results are due at 0200 BST / 1100 AEST.

AUSSIE BONDS: AUCTION PREVIEW: ACGB Jun-35 Supply Due

The Australian Office of Financial Management (AOFM) will today sell A$1200mn of the 2.75% 21 June 2035 bond, issue #TB145. The line was last sold on 2 May 2025 for A$900mn.

- The sale drew an average yield of 4.2413%, at a high yield of 4.2425% and was covered 3.4444x. There were 34 bidders, 13 of which were successful and 6 were allocated in full. The amount allotted at the highest yield as a percentage of the bid at that yield was 94.2%.

- This week's ACGB supply is above the top end of the recent average weekly issuance of $1500-2000mn, with A$1000mn of the 2.25% 21 May 2028 bond on Friday.

- During the first half of 2025-26, the AOFM plans to: issue a new October 2036 Treasury Bond (by syndication and subject to market conditions); conduct 2 Treasury Bond tenders most weeks; hold 1-2 Treasury Indexed Bond tenders each month.

- Issuance of Treasury Bonds (including Green Treasury Bonds) in 2025-26 is expected to be around $150 billion. Issuance of Treasury Indexed Bonds in 2025-26 is expected to be between $2 billion and $3 billion.

- Results are due at 0200 BST / 1100 AEST.

MNI EXCLUSIVE: MNI Discusses RBA's International Outlook