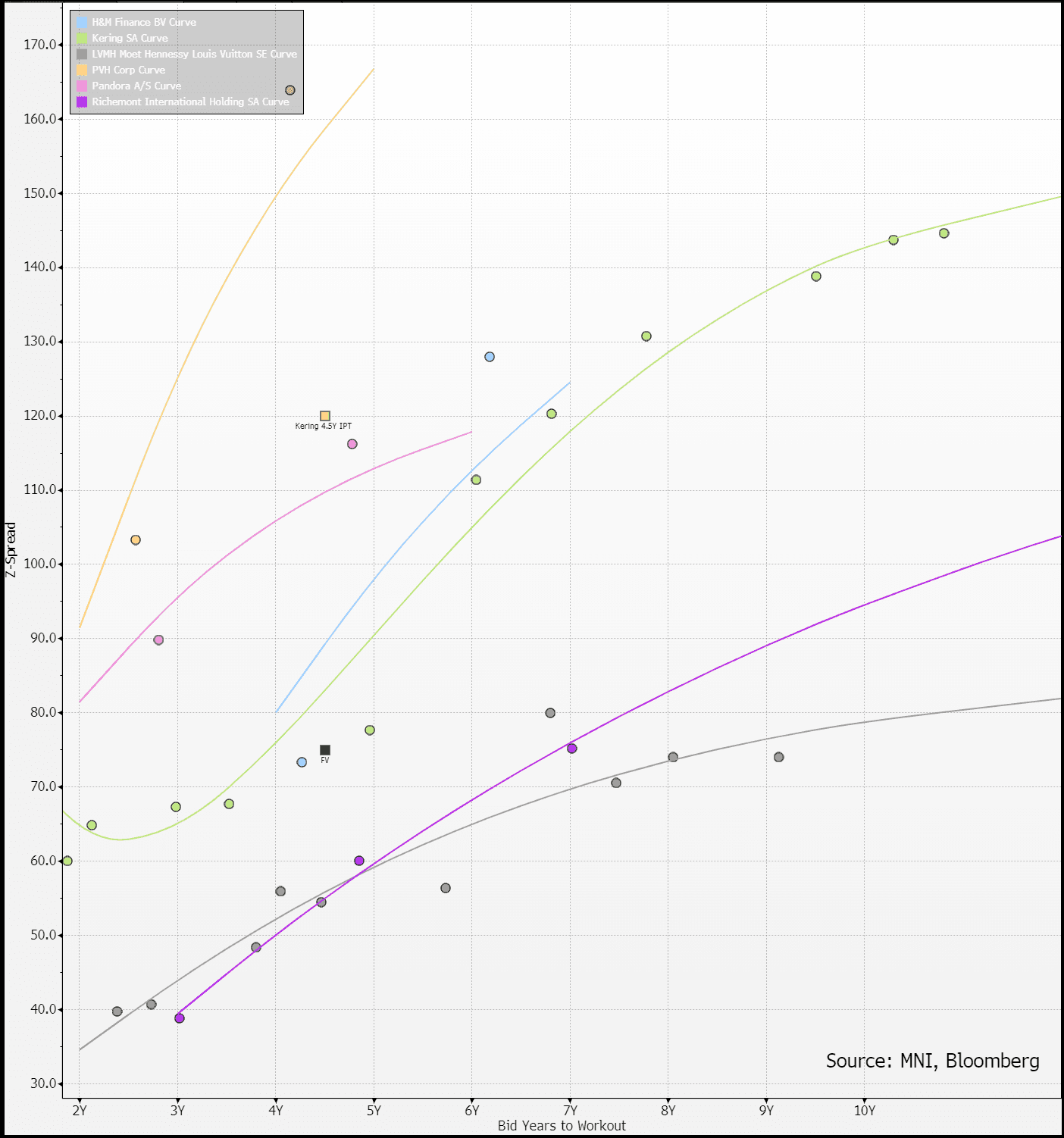

EU CONSUMER CYCLICALS: Kering | FV

(KERFP; NR/BBB+ Stable)

- €Bmrk 4.5y IPT +120 vs. FV +75 (-45)

- CoC, 2m par call, MWC, Clean-up call (75%)

- Likely will give a NIC but we will not see value unless it is sizeable

Kering's moves are rinse and repeat: tightens post earnings before selling off on the next release/miss. That led to bottom 10 returns in consumer/transport IG last year. Positive returns will likely emerge on the rebound and is a question of timing. Issue we have is it has nothing to show on that front yet. That will mean if macro weakens again sentiment around it will sour. More broadly, please do not confuse Kering's weakness as macro - it is clearly a brand heat issue with Gucci and to some extent YSL - both carry the bottom line.

Based on guidance remarks we see a -37% y/y fall in 1H EBIT when it reports in late July - consensus is at -36%. It is now doing ~€1b in EBIT/half - post Covid it was at €2.8b. Co is run by 2nd Gen Pinault.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

CARNEY ELECTION PLATFORM HAS CAD225B OF DEFICITS OVER FOUR YRS

- CARNEY ELECTION PLATFORM HAS CAD225B OF DEFICITS OVER FOUR YRS

- CARNEY SEES 2025-26 BUDGET DEFICIT OF CAD62.3B OR 2% OF GDP

- CARNEY PLANS TO REACH 2% NATO TARGET BEFORE 2030

- CARNEY SEES NEW CAD10B ANNUAL PLAN FOR GREEN TRANSITION BONDS

LOOK AHEAD: Eurozone Timeline of Key Events (Times BST)

| Date | Time | Country | Event |

| 25-Apr | 0745 | FR | Manufacturing Sentiment |

| 29-Apr | 0700 | DE | GFK Consumer Climate |

| 29-Apr | 0800 | ES | HICP (p) / GDP |

| 29-Apr | 0900 | EU | M3 / Consumer Expectations Survey |

| 29-Apr | 0900 | IT | ISTAT Confidence Indices |

| 29-Apr | 1000 | EU | Consumer Confidence, Industrial Sentiment |

| 30-Apr | 0630 | FR | GDP (p) / Consumer Spending |

| 30-Apr | 0700 | DE | Import/Export Prices / Retail Sales |

| 30-Apr | 0745 | FR | HICP (p) / PPI |

| 30-Apr | 0855 | DE | Unemployment |

| 30-Apr | 0900 | DE | GDP (p) / State level CPI |

| 30-Apr | 0900 | IT | GDP (p) |

| 30-Apr | 1000 | EU | GDP preliminary flash est. |

| 30-Apr | 1000 | IT | HICP (p) |

| 30-Apr | 1100 | IT | PPI |

| 30-Apr | 1300 | DE | HICP (p) |

JGBS: Twist-Steepener Holds Going Into W/E, BoJ Gov Ueda Reiterates Caution

JGB futures are stronger, +18 compared to settlement levels, sitting near the middle of the range after a choppy session.

- “Governor Kazuo Ueda reiterates his stance that the central bank will carefully monitor if its economic outlook will be realized, accounting for the effects of US tariff measures, without preconception. The BoJ will raise the benchmark rate if the outlook is realized, Ueda says in response to questions in parliament.” (per BBG)

- “Fukoku Mutual Life Insurance Co. plans to invest in Japan's super-long government bonds this fiscal year after their yields skyrocketed. The company aims to increase domestic government bond holdings by ¥30 billion, with gross purchases potentially reaching ¥300-400 billion.” (per BBG)

- Earlier today, Headline CPI for March showed +3.6% y/y versus +3.7% estimate. Core and Core-Core printed +3.2% y/y and +2.9% y/y, respectively, versus estimates of +3.2% and +2.9% and priors +3.0% and +2.6%.

- Cash US tsys are closed today for the Good Friday holiday.

- Cash JGBs have twist-steepened, pivoting at the 20-year, with yields 2bps lower to 5bps higher.

- Swap rates are 2bps lower to 2bps higher, with a steepening bias.

- On Monday, the local calendar will see Tokyo Condominiums for Sale data.