FED: June Communications Have Hawkish Tilt, Dovish Reaction Function (1/2)

The June FOMC communications had a hawkish tilt overall, despite the immediate dovish reaction to the updated Dot Plot retaining the median expectation of 50bp in rate cuts by end-2025. Chair Powell was far from emphatic about the prospect of rate cuts, all but taking a cut at the July meeting off the table. That said, the FOMC still remains committed to cutting, if only in half-hearted fashion.

- The rate "steepener" implied by the rate path shift was a little puzzling. Of 33 analyst notes coming into the meeting, none expected the FOMC to retain the 3.9% 2025 median while simultaneously upping 2026 and 2027 by 25bp each (to 3.6%, 3.4%). While the 2026 upward shift was fairly narrow in terms of the distribution, 2027's was more broad-based. It was thought that retaining the 2025 dot intact at 3.9% would naturally imply that the Fed clearly saw tariff inflation as transitory, and maintained concern over labor market developments.

- The Committee indeed sees tariffs as more inflationary and worse for growth and employment than 3 months ago, and the Statement changes and Chair Powell's press conference commentary suggested participants also more certain (or at least, less uncertain) about that outcome. And that outcome is that inflation is going to be a problem through 2026, i.e. not exactly transitory, and certainly problematic in the near-term. Overall, the increase to the 2026 and to a greater extent 2027's inflation forecasts was a surprise to consensus.

- Regarding the potential transitory nature of tariff inflation, Powell said re the new inflation forecasts that "people do generally expect inflation to move up and then to come back down. But we can't just assume that." The central tendency for core PCE (ie the middle 13 of 19 submissions) went up from 2.7-3.0% for this year, to 2.9-3.4%. That is consistent with the likely Y/Y inflation hit from already-announced tariffs. But the central core PCE tendency for 2026 went up to 2.3-2.7%, from 2.1-2.4%, which is pretty non-transitory and doesn't really square with them cutting rates if inflation is on that kind of trajectory. It also suggests that the Committee is pretty dismissive of the recent downside inflation surprises.

- The implication there is that even if some participants (in this case, 7 of 19) see rates on hold through the rest of 2025, there will be enough policy certainty and data-based evidence to warrant them supporting at least one cut next year. That's despite the lack of conviction that inflation will get back to target through 2027. Again, the FOMC is setting policy in anticipation of achieving the 2% target at some point, reminiscent of 2024 and suggesting that the median Fed participant has a dovish reaction function: even with inflation ascending through end-year, it's appropriate to cut.

- The propensity to ease could be explained in part by a higher unemployment forecast, which rate cuts would ostensibly be keeping from rising any further, but Chair Powell sounded largely dismissive of labor market weakness developing (apart from the caveat that hiring has been subdued so when labor demand falls, the unemployment rate could rise quickly), saying "I would say you can see perhaps a very, very slow continued cooling. But nothing that's troubling at this time."

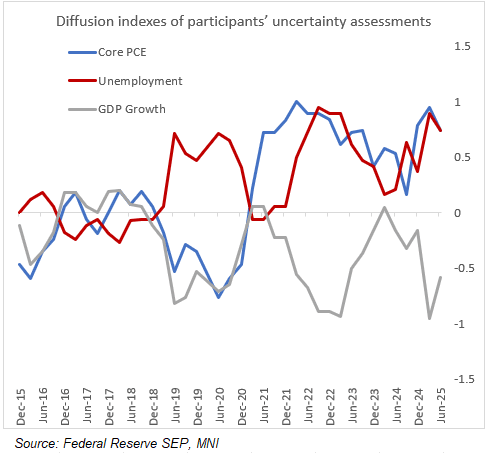

- Having now moved unemployment and inflation forecasts higher and growth forecasts lower, diffusion indices of analysts' risk weightings shifted in a less stagflationary manner vs March. But while there was slightly less perceived risk of higher inflation or unemployment than forecast, there was substantially less risk perceived of a downside growth miss (the diffusion index moved to -0.58 from -0.95) with a couple of participants seeing risks weighted to the upside. Overall uncertainty (in either direction) remained unchanged for inflation, even while dipping very slightly for GDP and unemployment. This is natural given GDP has been marked-to-marked lower, but possibly also indicates that the FOMC doesn't see the risk of a recession materializing to the same degree as in March, which makes sense given the data.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FED: Dallas's Logan Advocates For Standing Repo Enhancement As Reserves Shrink

Dallas Fed Pres Logan, formerly the head of the Fed's SOMA portfolio at the NY Fed, continued to advocate for banks to use Fed facilities including the standing repo facility and discount window in times of stress.

- Logan: "Depository institutions have greatly improved their operational readiness to borrow from the discount window. We should continue to reinforce the value of operational readiness so firms maintain these gains. And readiness is a partnership. At the Federal Reserve Banks, we are working to enhance our capacity to serve customers efficiently when they come to borrow...We should also continue to emphasize that borrowing from the window is an appropriate way for healthy banks to meet short-term funding needs—not something investors, ratings agencies or supervisors should criticize or question."

- "We can also enhance the SRF. As Roberto [Perli, current SOMA manager] described in his recent speech, experiments and market outreach by the New York Fed’s Open Market Trading Desk have found that conducting and settling the SRF operation in the morning, in addition to the current afternoon timing, makes the facility more effective by addressing intraday funding needs. I’m pleased that...the Desk plans to soon introduce regular early-settlement SRF operations. Central clearing of SRF operations would also make the facility more attractive and enhance rate control. That’s because central clearing would allow bank-affiliated dealers to net down their balance sheets when they borrow from the SRF and lend onward to other firms."

- Commentary at the panel discussion chaired by Logan was also noteworthy in pointing out that the Fed should look at a wide array of rates to signal reserve scarcity. Wrightson ICAP's Crandall noted that the Fed funds effective rate could be late in providing a signal: “The last way you want to measure the availability of liquidity in the overnight market is the fed funds market...the rate will eventually respond to changes in market conditions but it may very well be the last rate to do that.”

- Logan said (quoted by Bloomberg): “In my view, rate control is not just about keeping the fed funds rate in the target range...the fed funds market is small. And the FOMC’s desired stance of monetary policy must transmit smoothly into larger and broader markets — especially the repo market.”

- Of course, using the SRF and discount window are ways of ensuring market functioning while reserves shrink, allowing the Fed balance sheet to wind down further.

USDCAD TECHS: Corrective Cycle

- RES 4: 1.4296 High Apr 7

- RES 3: 1.4111 High Apr 4

- RES 2: 1.4024 50-day EMA

- RES 1: 1.4016 High May 12 / 13

- PRICE: 1.3925 @ 16:44 BST May 19

- SUP 1: 1.3814/3751 Low May 8 / 6 and the bear trigger

- SUP 2: 1.3744 76.4% retracement of Sep 25 ‘24 - Feb 3 bull run

- SUP 3: 1.3696 Low Oct 10 ‘24

- SUP 4: 1.3643 Low Oct 9 ‘24

Despite the latest move higher, the trend condition remains bearish in USD/CAD and Monday’s weakness confirms recent strength as corrective. A fresh cycle low on May 6 reinforces the bearish theme. A resumption of weakness would open 1.3744, a Fibonacci retracement. Note that moving average studies are in a bear mode position, highlighting a dominant downtrend. Key resistance is seen at 1.4024, the 50-day EMA.

US TSYS: 30Y Holds 5% Level Amid Broad Post-Downgrade Rally

Treasuries recovered from early weakness to close flat/stronger Monday, with bull steepening in the curve.

- Following on from Friday's post-close surprise downgrade of the US's AAA credit rating by Moody's, yields rose sharply in the early going.

- While over the weekend White House officials shrugged off Moody's decision, there was significant attention on the apparently deteriorating fiscal trajectory overnight as House Republicans cleared a procedural hurdle to get the "Big, Beautiful" tax bill closer to completion.

- 30Y yields notably touched their highest since Nov 1 2023 (5.0353%) - up 13.5bp from Friday's ratings downgrade announcement - before an impressive reversal lower on the day (just 1+bp up from pre-downgrade).

- Despite little in the way of headline catalysts - China expressed displeasure with the US's guidance against the use of some Huawei chips, bringing a brief risk-off reaction - Treasuries rallied alongside equities for the rest of the session (the TY upturn started with the equity cash open).

- We heard from multiple Fed speakers, including Bostic, Jefferson, Williams, and Kashkari, all of whom reiterated the FOMC's patient approach on cuts amid economic uncertainty, and Williams and Bostic in particular suggesting that the next cut wouldn't seriously be contemplated until after the summer. Reaction was limited however given the market's already-low implied probability of a cut before September.

- Data was relatively thin - Conference Board leading economic index had its sharpest drop since 2023 but avoided an outright recession signal.

- Latest levels: the 2-Yr yield is down 3.1bps at 3.9681%, 5-Yr is down 3.2bps at 4.0611%, 10-Yr is down 2.2bps at 4.4553%, and 30-Yr is down 2.6bps at 4.9183%.

- Jun 10-Yr futures (TY) down 2.5/32 at 110-08 (L: 109-20 / H: 110-09)

- Tuesday's schedule includes the Philly Fed nonmanufacturing survey along with another slew of Fed speakers, including Collins, Barkin, Musalem, Kugler, Hammack and Daly.