FOREX: JPY Off Lows, But Still Nursing Sharp Weekly Losses

Jan-14 10:23

* In contrast to JPY weakness that pervaded across the first few sessions of the week, the currenc...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

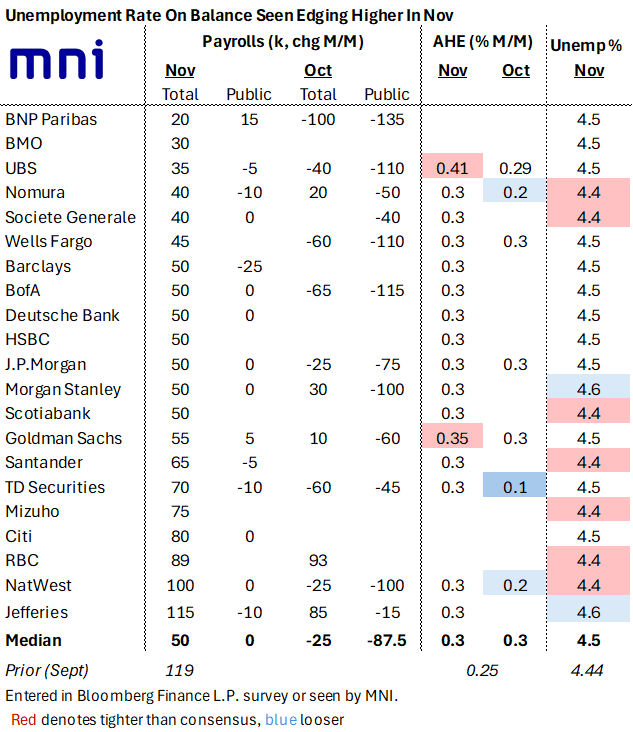

US OUTLOOK/OPINION: NFP Growth Eyed At 50k In Nov After -25k In Oct

Dec-15 10:20

- Our latest survey of primary dealer analyst expectations shows a median estimate of 50k nonfarm payroll gains in November after -25k in October (following +119k in September).

- Public sector payrolls are seen contracting heavily in October, largely reflecting deferred DOGE layoffs rather than the federal government shutdown, before a relatively flat figure in November. The October public sector range is wide, from -135k (BNP Paribas) to -15k (Jefferies) with a median of -87.5k that lands between -75k and -100k estimates.

- The unemployment rate is on balance seen ticking up to 4.5% in November from an unrounded 4.44% in September (reminder, no Household Survey and therefore no unemployment rate will be published for October).

- Two look for a further upward surprise at 4.6% (MS and Jefferies, the latter despite being the strongest for estimated NFP growth) but risk is generally skewed lower with seven analysts eyeing an unchanged 4.4%.

- Average hourly earning growth is seen relatively steady at 0.3% M/M in both months (vs 0.25% in September) but with risk skewed a little lower for October.

- The full MNI US Payrolls Preview will follow later today.

EQUITY OPTIONS: Estoxx Put Ladder

Dec-15 10:13

SX5E (19th dec) 5250/5000/4750p ladder, bought for flat in 3k.

FOREX: Negative Dollar Bias Dominates, USDJPY Returns to 155.00

Dec-15 10:12

- Approaching the busy central bank slate and US data calendar this week, the dollar is starting the week on the back foot once again. Moves for the dollar index have been relatively contained, with the DXY just 0.1% lower on the session, although we remain within 20 pips of last week’s pullback lows. The softer dollar backdrop has allowed the likes of gold and silver to extend higher, rising 1% and 3% respectively, while the Japanese Yen outperforms across the G10.

- USDJPY has been pressured by lower core yields on Monday, with the pair largely shrugging off the firmer tone for risk. USDJPY has exhibited a 105-pip range, with the latest dip below 155 now probing last week’s lows. Below here, the December 05 low at 154.35 and the 50-day EMA at 153.95 represent an important support area as we navigate both the US data releases and BOJ decision.

- At the other end of the G10 leaderboard, NZD has notably declined amid comments from the newly appointed RBNZ Governor. Breman said the forward path for the OCR published in the November policy statement “indicates a slight probability of another rate cut in the near term”, pushing back against any expectations for a hike in 2026. NZDUSD is 0.35% lower on the session and back below 0.58, while AUDNZD briefly rose to a recovery high of 1.1520.

- Elsewhere, USDKRW has extended session losses to nearly 1% after South Korea’s National Pension Service said it will conduct its strategic FX hedging in a “flexible” manner. USDKRW gathered downside momentum through the overnight lows at 1470 and notably, we are now below 20-day EMA support – a close below this average would be the first since September.