FOREX: JPY Crosses - GBP/JPY Marked Lower

US stocks outperformance is now widening out to the broader market and global risk sentiment remains very positive. The JPY bounced against the GBP overnight which sold off across the board as Gilts collapsed on UK centric news.

- EUR/JPY - Overnight range 169.04 - 169.79, Asia is trading around 169.50. The pair seems to be consolidating in a 168.50 - 170.00 range, can NFP help this breakout tonight ? A break back above 170.00 is needed to reengage the upward momentum.

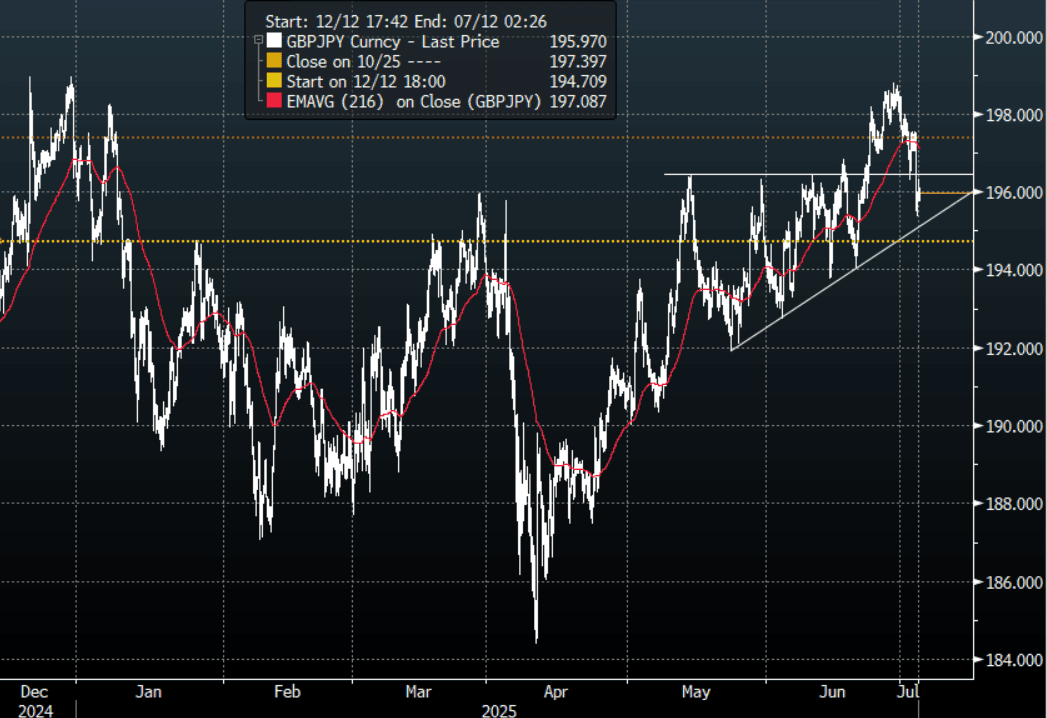

- GBP/JPY - Overnight range 195.37 - 197.55, Asia trades around 195.90. Speculation about a possible exit by Rachel Reeves made investors nervous and the GBP got hit across the board. The pair technically remains in an uptrend but a close sub 194.00 would get JPY bulls excited again.

- NZD/JPY - Overnight range 87.03 - 87.60, Asia is currently dealing 87.25. NZD/JPY continues to trade sideways as it consolidates, a sustained break above 88.00 is needed for the market to turn its focus back to the 90.00 area. The longer this cross stalls up here the greater the chance of it turning back towards the 96.00 area.

- CNH/JPY - Overnight range 20.0277 - 20.1237 Asia is currently trading around 20.0650. A big reversal from the 20.50/20.60 resistance area. In the middle of its recent range awaiting clearer direction with a bias to sell rallies.

Fig 1 : GBP/JPY Hourly Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Viewpoint of Jim Bianco On Rates

Jim Biance posted a thread on X on why the risk is that long-term rates go higher: “Polymarket recession odds peaked at 65% on May 1st, the April ISM release date, suggesting Liberation Day and the 20% stock market correction did not damage the economy, as the "soft data" warned. Subsequent April data confirmed this. Will May see more of the same?”

- “The prevailing narrative in the market for months has been that the labor market is going to fall apart, forcing the Fed to cut rates. This has not happened, and so far, the "soft" (survey) data have been wildly off in predicting the economy.’

- “ISM Employment upticked in May from April. The first monthly "May" data point suggests the labor market is still not weakening.”

- “ISM New Orders are included in the Index of Leading Economic Indicators (LEI). They slightly increased in May compared to April. In other words, this component of LEI is also NOT slowing.

- “This series, along with the release of construction spending today, pushed the Atlanta Fed's GDPnow to an eye-popping 4.6%.”

- “No way an organization worried about its reputation is going to cut rates if we're pushing towards 5% Q2 GDP. The market views it this way. The June 18 FOMC has only a 5% probability of a cut, or 95% of no move. July 30 is just 21%, or 79% of no move.”

“Long rates are already in an uptrend (below). Throw in a rate cut with a 5% GDP growth, and the risk is that long-term rates soar, damaging the Fed's reputation.”

Fig 1 : US 30-Year Yield Weekly Chart

Source: MNI - Market News/Bloomberg

AUSTRALIA DATA: Net Exports Detracted From Q1 Growth

Not only was the current account deficit larger than expected but Q4 was revised significantly wider, but that meant that it narrowed in Q1. It was $14.7bn in Q1 after $16.3bn in Q4. Net exports detracted 0.1pp from growth while the 0.2pp contribution in Q4 was revised down to a 0.1pp detraction.

- The Q1 improvement in the current account was due to a smaller net income deficit as lower coal prices resulted in less dividends paid to overseas investors. The primary income deficit narrowed $2.2bn to $19.4bn.

- The goods & services surplus narrowed $0.2bn to $5.2bn due to a widening in the services deficit. Exports rose 1.9% q/q while imports picked up 2.2% q/q.

Australia current account $bn

Source: MNI - Market News/ABS

- Goods exports rose 2.9% q/q but were down 2.4% y/y. The quarterly increase was driven by non-monetary gold (volumes & prices rose) and rural goods, while non-rural posted its fifth consecutive quarterly decline. Services fell 1.7% q/q but were up 7% y/y.

- The ABS noted that the Q1 shipment of gold to the US was larger than the total of the last four years, as producers aimed to beat US tariffs. Excluding gold, total goods exports would have declined 1% q/q due to disruptions to coal production and lower prices.

- Merchandise imports were up 3.1% q/q & 2.7%y/y with consumer goods +0.3% q/q and intermediate +7.1% q/q, due to a pickup in fuel prices, but capital down 1.1% q/q, consistent with weak investment. Services fell 0.5% q/q as overseas travel became less popular.

- The terms of trade appear to have stabilised with Q1 +0.1% q/q, second straight increase, to drive an improvement in the annual rate to -4.0% from -4.6%. Export prices rose 2.8% q/q with both goods and services higher, while import prices increased 2.6% q/q driven by goods with services little changed.

Australia terms of trade indices

Source: MNI - Market News/ABS

JGBS AUCTION: Poll: 10-Year JGB Auction

*JAPAN 10Y GOVT BOND AUCTION MAY HAVE 98.95 LOWEST PRICE: POLL– BLOOMBERG