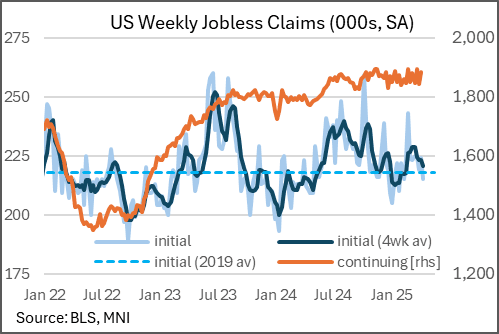

US DATA: Jobless Claims Solid In April Payrolls Reference Week

Initial claims for the week of April 12 (which is the nonfarm payrolls reference week for April) came in at a joint 11-week low 215k, below the 225k expected and down from 224k prior (upwardly revised 1k). This brought the 4-week average down 2k to 221k.

- Conversely, continuing claims printed 1,855 in the April 5 week, with the 41k rise largely reversing the prior week's 49k drop (1,870k expected, 1,844k prior rev from 1,850k).

- As such, both series remain well within their ranges of the last 6-9 months, suggestive of a labor market that may not be strengthening but likewise is not showing any signs of deterioration.

- There are few signs of rising federal government DOGE-related layoffs in the data either: federal employee initial claims ticked up to 542 (NSA) in the Apr 4 week, up 34 from prior but still well below the 1k+ seen in March weeks; likewise continuing claims fell to an 8-week low.

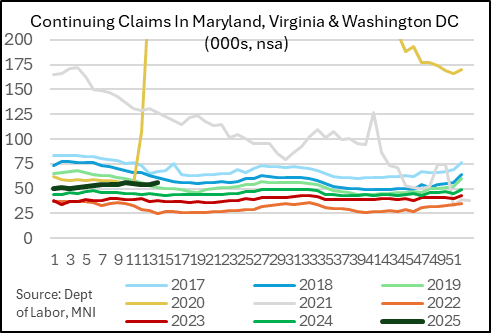

- Continuing claims are creeping up in the Washington Area (Maryland, Virginia, DC) - by 2k to 55,616 in the April 4 week which is somewhat above the normal trajectory seen in previous years at this time, so could bear watching - however, initial claims in those geographies remain subdued (6.2k in the April 12 week, very typical).

- On a non-seasonally adjusted basis, total initial claims ticked up 3k to 220k, while continuing dropped 35k to 1,951k, with the adjustment not appearing to be out of the ordinary for the respective weeks of the year.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EURIBOR OPTIONS: ERM5 98.125/98.375 Call Spread vs 97.625 Puts Position Sold Out

ERM5 98.125/98.375 call spread vs 97.625 puts, 10K given at 1.75 vs. 97.785-97.79. Market contacts point to an unwind of an existing position.

MNI: US REDBOOK: MAR STORE SALES +5.5% V YR AGO MO

- MNI: US REDBOOK: MAR STORE SALES +5.5% V YR AGO MO

- US REDBOOK: STORE SALES +5.2% WK ENDED MAR 15 V YR AGO WK

PIPELINE: Corporate Bond Update: Volkswagen 7pt on Tap, $2B ADB Launched

Absent for some time, VW 7-tranche debt expected today. This comes on the heels of Rheinmetall expressing interest in using VW plant for military vehicle production, not to mention debt brake reform headlines that roiled Bunds earlier in the month. Estimating the size of today's VW issuance around $5-$6B. Prior issuance for reference:

-- 09/05/23 $3.4B VW: $800M 2Y +85, $50M 2Y SOFR+93, $900M 3Y +105, $700M 5Y +130, $500M 10Y +165

-- 05/31/22 $3B VW: $500M 2Y SOFR+95, $900M 3Y +125, $1.1B 5Y +155, $500M 7Y +175

- Date $MM Issuer (Priced *, Launch #)

- 03/18 $Benchmark Volkswagen AM 2Y +120a, 2Y SOFR, 3Y +135a, 3Y SOFR, 5Y +155a, 7Y +170a, 10Y +180a

- 03/18 $2B #ADB 10Y SOFR+57

- 03/18 $Benchmark LG Energy 3Y, 5Y, 10Y

- 03/18 $Benchmark Bangkok Bank 15NC10 +215a

- 03/18 $Benchmark Korea National Oil 3Y +120a, 3Y SOFR, 5Y

- 03/18 $Benchmark ING 4NC3 +110a, 4NC3 SOFR, 6NC5 +125a, 11NC10 +150a