POWER: Italy Up on Energy Complex, Stronger Hydro Reserves Limit Gains

The Italian October base-load power contract is trading slightly higher to be supported by revised higher temperatures and gains in EU ETS and TTF. However, an uptick in hydro reservoirs in the country is adding downward pressure.

- Italy Base Power OCT 25 up 0.1% at 107 EUR/MWh

- EUA DEC 25 up 0.5% at 75.36 EUR/MT

- TTF Gas OCT 25 up 0.1% at 32.135 EUR/MWh

- TTF is holding steady within the €31.4/MWh to €32.7/MWh range so far this week with higher LNG imports helping to cover during the current Norwegian seasonal maintenance as storage builds towards target levels.

- EUAs Dec25 are rangebound, influenced by losses in EU gas and equities. TTF trended lower on higher LNG imports, while the STOXX was weighed by a dip in the healthcare sector, with other sectors remaining stable.

- The latest two-week ECMWF weather forecast for Rome suggests mean temperatures have been revised higher over 4-9 September. Average temperatures are expected to be above the seasonal average throughout the 14-day period.

- Mean temperatures in Rome are forecast at 23.78C on Friday from 23.6C on Thursday and above the seasonal average of 23.26C.

- The PUN index dropped to €113.22/MWh for Thursday’s delivery, compared with €106.56/MWh the day before.

- Wind output in Italy is forecast at 0.988GW during base load on Friday, down from 1.30GW on Thursday. Solar PV output is forecast at 11.21GW during peak load on Friday up from 10.98GW on Thursday, according to SpotRenewables.

- Residual load in Italy is forecast at 27.08GWh/h on Friday, relatively unchanged on the day, and down from 27.13GWh/h on Thursday, Reuters data showed.

- Italian hydropower reserves last week – calendar week 35 –rebounded on week to end their four consecutive week downward trend to be at 3.11TWh. This is the highest reserves have been since week 32.

- Italy’s hydro balance forecast has been revised higher on the day to -240GWh on 18 September from -477GWh previously.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BONDS: From session high to session lows for Gilt and wider Bonds

- From session high to session low for Gilt and now EGBs.

- The 4.50% Yield level provided good support for the UK 10yr Yield, printed a 4.496% low, and as noted, Gilt and Schatz are seeing heavy supply in early trade.

- As such, Gilt keeps the pressure in long end Govies, and Schatz underperforms within German Govies.

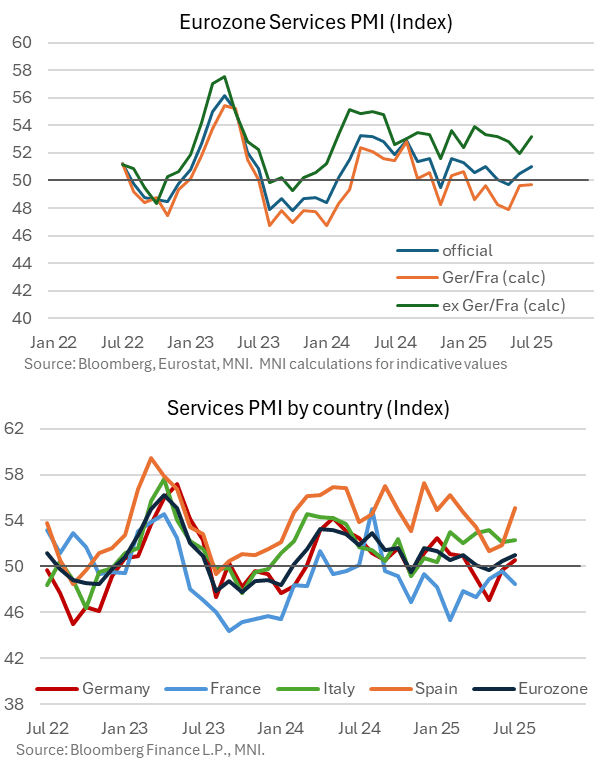

EUROZONE DATA: July Composite PMI Consistent With Weakly Positive Growth

The Eurozone July services PMI was revised down two tenths to 51.0, but that still marks a second consecutive increase from 49.7 in May and 50.5 in June.

- We estimate the France/Germany services PMI at 49.7 (vs 49.9 flash), with a notable 1.2 point downward revision in France to 48.5 partially offset by a 0.5 point upward revision in Germany to 50.6.

- The ex-France/Germany PMI is estimated at 53.2 (vs 53.4 flash). Spanish data this morning was much stronger-than-expected, while Italy was a little softer.

The composite PMI was 50.9 (vs 51.0 flash, 50.6 prior), the seventh consecutive month above the neutral 50 handle. Overall, the PMI continues to point to only weakly positive growth. The release notes that “the rate of increase in business activity remained sluggish and was weaker than the survey average as stagnant demand held back output.”

- The release also states “as was the case in June, new orders were down by a fraction at the beginning of the third quarter. The last time a rise in new business intakes was signalled was May 2024. Export sales remained a drag, stretching the current sequence of deteriorating international client demand to 41 months.”

“After a brief run of strengthening optimism across the eurozone private sector, July survey data indicated a drop in confidence for the first time since April”.

FOREX: FX OPTION EXPIRY - Large AUD on Friday

- Large AUD on Friday down to 4.27bn vs 4.32bn Yesterday.

Of note:

EURUSD 2.32bn at 1.1550.

EURUSD ~1bn at 1.1550 (wed).

USDJPY 1.37bn at 147.00 (wed).

USDJPY 1.14bn at 147.65 (thu).

AUDUSD 4.27bn at 0.6500 (fri).

EURGBP 2.4bn at 0.8675/0.8700 (fri).

EURUSD 1.23bn at 1.1550 (mon).

- EURUSD: 1.1500 (1.4bn), 1.1550 (2.32bn), 1.1585 (1.44bn), 1.1600 (1.77bn).

- USDJPY: 148.00 (558mln).

- USDCNY: 7.1490 (500mln), 7.1500 (565mln).