EGB SYNDICATION: Ireland 10-year Jun-36 : Allocations

* Size: E5bln (above MNI's E3-4bln expectation) * Books closed in excess of E43bln (inc E2.2bln JLM ...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

OUTLOOK: Price Signal Summary - Bear Mode Condition In Bunds Intact

- In the FI space, Bund futures are in consolidation mode. A bear-mode cycle is intact and the contract is trading closer to its recent lows. Scope is seen for an extension towards the 127.00 handle. Key short-term resistance is 128.75, the Dec 3 high. Note that the contract is oversold. A stronger corrective bounce would allow this oversold condition to unwind. The price pattern on Dec 10 is a doji candle - a short-term reversal signal.

- Recent price action in Gilt futures highlights 90.53, the Nov 25 / 26 low, and 91.93, the Nov 27 high, as two important short-term directional triggers. A breach of 90.53 would signal scope for a deeper retracement towards 89.86, the Nov 19 low and bear trigger. For bulls, a stronger resumption of gains and a breach of 91.93, would instead signal scope for a climb to resistance at 92.55, the Nov 11 high.

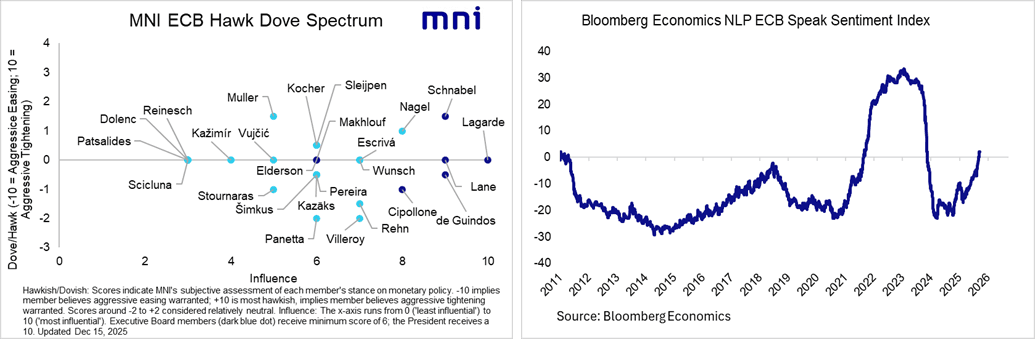

ECB: ECB Speak Wrap (Dec 4 – Dec 15)

This week’s ECB speak wrap provides a broader summary of Governing Council communication since October. It will be included in our full ECB preview, set to be released tomorrow. See here for the full publication

MNI Policy Team Sources (Dec 9):

- The European Central Bank’s December projection round to be unveiled at the 18 Dec. Governing Council meeting is not expected to depart significantly from September’s figures, with communication as 2026 dawns balancing hawk-dove differences by seeking to reinforce two-way risks around the 2.0% policy rate, Eurosystem sources have told MNI.

Rate Decision and Rate Outlook: Since the October decision, Governing Council (GC) speakers have coalesced around President Lagarde’s guidance that rates are in a “good place”. Given recent hawkish repricing in EUR rates (which now assign a ~25-30% implied probability of a hike by end-2026), we will be interested in whether redeployment of this phrase would be considered a marginally net dovish signal – in contrast to prior meetings.

Updated Macroeconomic Projections: The December decision communication will be shaped by an updated set of macroeconomic projections. We think GC policymakers will pay most attention to the core inflation projections.

Relative to our mid-October update, we’ve made a few net hawkish tweaks to our ECB Hawk/Dove matrix. Overall, these revisions are consistent with recent moves in Bloomberg’s NLP-based ECB speak sentiment model, which crossed into net hawkish territory following Schnabel’s recent interview.

FOREX: NZDUSD Continuing Post-Breman Recovery

- Although NZD remains among the weakest in G10 on Monday, constructive risk sentiment and a softer dollar backdrop has continued to support the NZDUSD recovery ahead of the NY crossover. NZDUSD is now just 0.17% lower at 0.5797, representing a solid bounce from the overnight lows of 0.5766.

- As a reminder, the Kiwi dollar notably declined amid comments from the newly appointed RBNZ Governor Breman, indicated that market conditions have tightened “beyond what is implied by our central projection” for the official cash rate. ANZ said that “markets were caught by surprise by the comments, which weren’t scheduled, and it looks like a deliberate attempt to address market pricing and the tightening in financial conditions.”

- While the upcoming US data will likely be the most meaningful driver of NZDUSD sentiment, it is worth pointing out we have New Zealand Q3 GDP during Thursday’s APAC session. After activity contracted 0.9% q/q in the second quarter, some rebound is expected in Q3 and into Q4. The RBNZ forecast a 0.4% q/q rise in Q3 GDP in November.