OIL: Iraq Set for Key Oil Cargo Surge

Jul-18 17:29

Iraq will raise shipments of a key crude grade in August, part of an enlarged export programme indicating that the OPEC+ member is boosting its oil production.

- Iraq will lift shipments of destination free Basrah Medium to 17m-18m bbl in August, around 4m bbl, or 20%-30% above typical monthly quantities.

- OPEC+ rolled out a series of hikes in recent months, a policy reversal following years of constraint. This has sparked concerns of a looming supply glut.

- Overall export plans for August have not been released by SOMO, the state marketer, Bloomberg said.

- The full programme contains both destination free and destination restricted supplies of Basrah Medium and Basrah Heavy crude.

- Iraq’s crude shipments were up to around 3.35m b/d in June, 60% of which were Basrah Medium.

- Flows have not been affected by recent drone attacks in Kurdistan as SOMO does not export any crude from that region.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

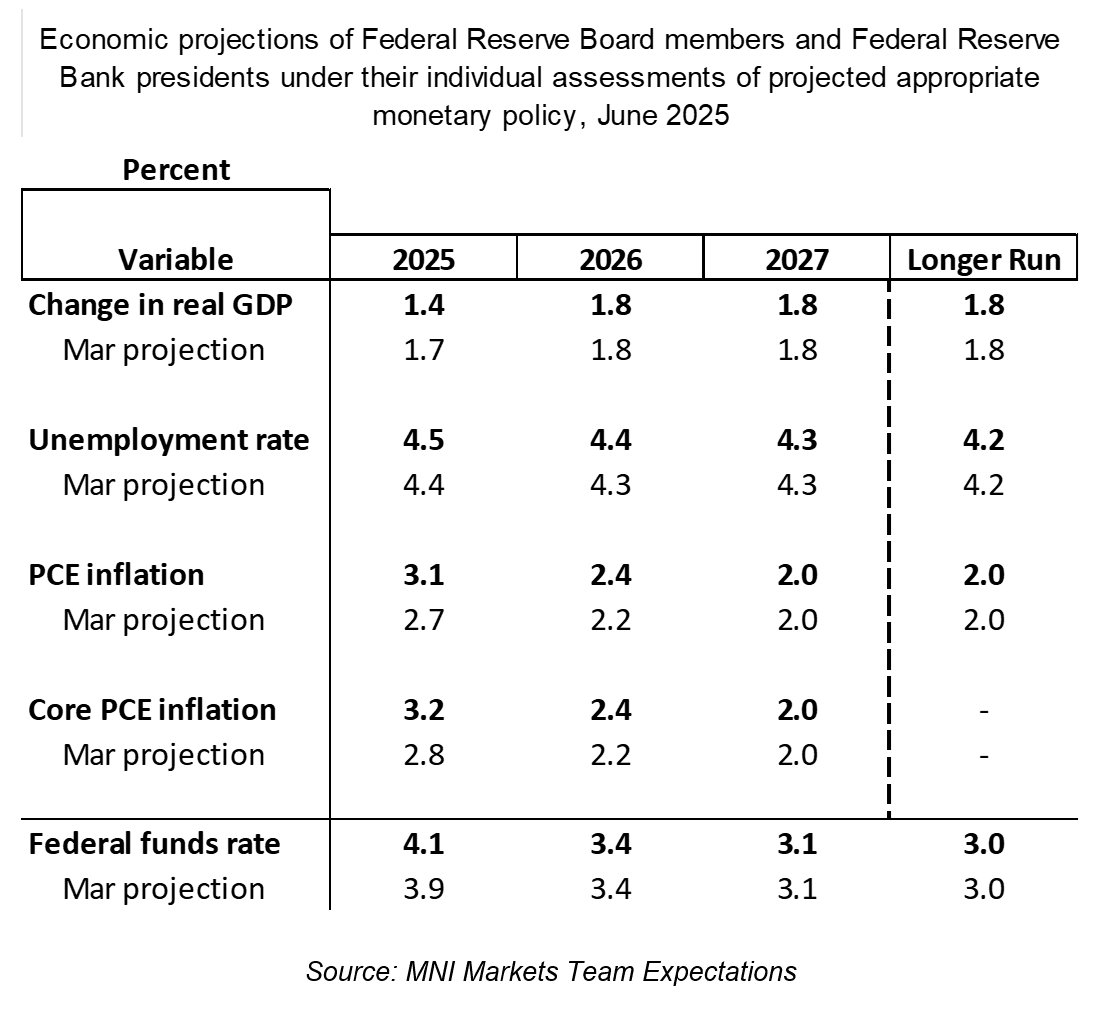

FED: Expectations For Today's FOMC Decision: Close Call On 2025 Dot (1/2)

Jun-18 17:24

Below are MNI's expectations for the new economic projections out at 2pm ET. Our full meeting preview, including analyst expectations, is Here.

- Starting with the macro projections: broad expectations are for 2025 GDP to be revised down, with inflation and unemployment revised up.

- Roughly speaking, analyst consensus is for the 2025 unemployment projection to rise 0.1pp to 4.5% (though many see unchanged), with real GDP lowered to 1.2-1.4% and core PCE increased 0.3pp to 3.1% (we've seen a range roughly of 2.9% to 3.3%). Most don't expect meaningful changes to 2026 forecasts.

- The FOMC's 2025 rate dot median meanwhile is seen unchanged by the median analyst, at 3.9% (2 cuts from current levels by year-end). However that's an extremely close call: 11 of 24 analysts who expressed an opinion expect it to shift up 25bp vs March's, to 4.1%, with the other 13 see it remaining at 3.9%.

- Of the 17 analysts who had a view on the 2026 median, 7 saw an upward shift by 25 to 3.6% (the remaining 10 saw no change at 3.4%).

- The longer-run dot is more unanimously seen remaining at 3.0%, with 12 of 15 analysts seeing no change (3 see a rise to 3.1%).

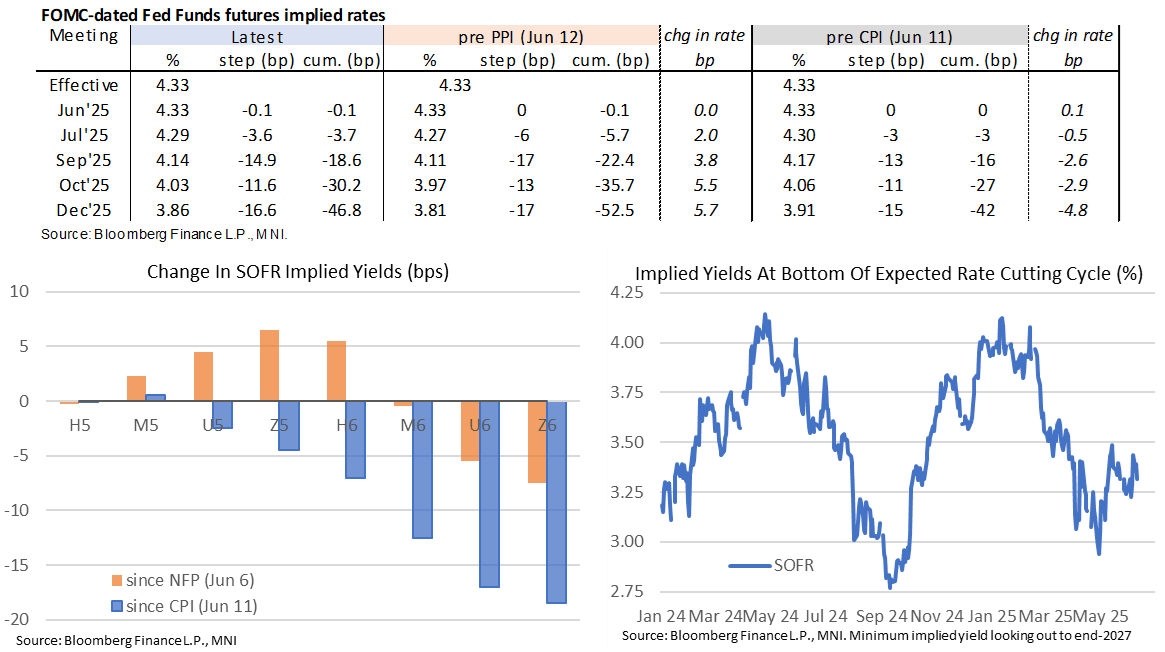

STIR: 47bp Of Cuts Priced For 2025 With FOMC And Dot Plot At 1400ET

Jun-18 17:13

- Fed Funds implied rates are a little off session lows as we head within an hour of the FOMC decision.

- It has been helped by crude oil futures paring losses but WTI still -0.6% as near-term inflationary implications from the Israel-Iran conflict continue to set the tone for pricing for intraday moves in 2025 meetings.

- Cumulative cuts from 4.33% effective: 0bp for today, 3.5bp Jul, 19bp Sep, 30.5bp Oct and 47bp Dec.

- SOFR futures have flattened further today as growth concerns weigh further out the curve, with SFRZ5Z6 at -0.65 (-0.02) although it’s off session lows of -0.66.

- The SOFR implied terminal yield has pushed a quarter out, now seen landing in the H7. The yield of 3.23% is 5bp lower on the day, having last closed lower on Jun 4.

- Dot plot and projections watched. From the MNI Preview: “The new quarterly projections will still signal the resumption of rate cuts later this year, but likely only one 25bp reduction instead of the two cuts envisaged at the March meeting.”

- “While risks to both the Fed’s inflation and employment mandates remain elevated, with the new 2025 forecasts looking increasingly reflective of stagflation, the Committee should still signal rate cuts through end-2026 of a similar magnitude to its previous set of projections”

- https://media.marketnews.com/Fed_Prev_Jun2025_With_Analysts_a9c8a317ff.pdf

BOC SAYS CORE CPI INDEXES MAYBE DISTORTED, TREND MORE LIKE 2%

Jun-18 17:10

- BOC SAYS CORE CPI INDEXES MAYBE DISTORTED, TREND MORE LIKE 2%

- BOC TRACKING BROADER RANGE OF TREND INFLATION MEASURES