SOUTH KOREA: Inflation Remains Above BoK Target As Imported Inflation Rising

December CPI inflation printed in line with consensus with headline rising 0.3% m/m to 2.3% y/y down from November’s 2.4%. Core held at 2.0% y/y, around where it has been for most of 2025. 2025 headline inflation moderated 0.2pp to 2.1%, just above the Bank of Korea’s 2.0% goal. With inflation remaining above target and import price inflation creeping up while mortgage debt is growing due to rising house prices, the central bank is likely to leave rates at 2.5% for now, where they have been since May.

- The moderation in headline was driven by lower food inflation which moderated to 3.6% y/y from 4.7% in November, which should reassure the BoK given its concern over rising living costs. Transportation inflation remained elevated though at 3.2% y/y unchanged from October. Other categories were little changed except miscellaneous goods & services which may have been impacted by higher global gold & silver prices.

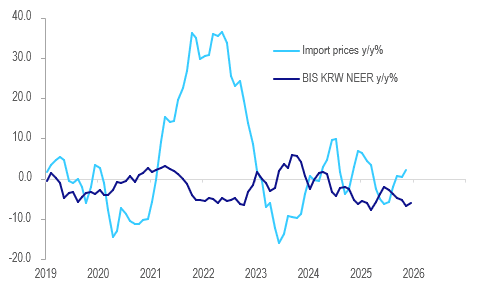

- The BIS KRW NEER is down 5.9% y/y in December after recording six consecutive monthly declines. The weaker currency is pushing imported inflation higher which rose 2.2% y/y in November up from 0.5%. It has risen each month since July, in line with the fall in the NEER.

- The next BoK decision is on 15 January.

South Korea import prices vs BIS KRW NEER y/y%

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US STOCKS: S&P(ESZ5) - Looks To Retest Highs

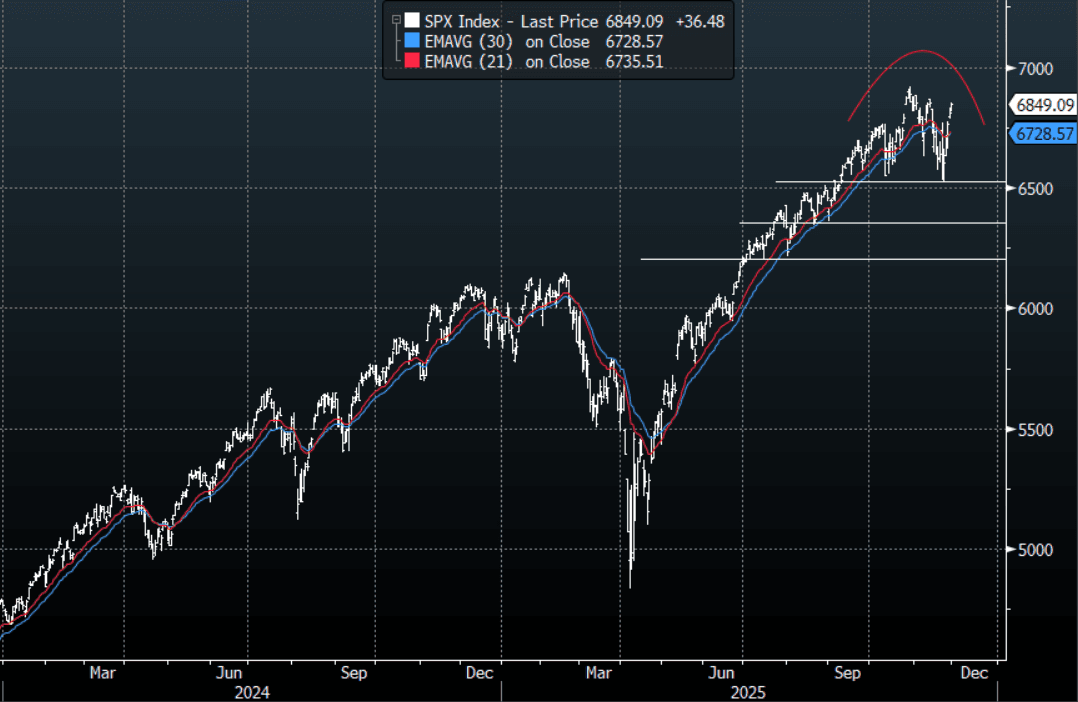

The S&P(ESZ5) Friday night range was 6831.25 - 6863.75, SPX closed +0.54%, Asia is currently trading around 6850. The market continues to build on its move higher as more cuts look to be priced into the US. The Bulls will be cheering on this constructive price action and with Hassett now the leading front-runner to replace Powell so is their confidence for cuts. I remain wary of getting bullish up here, I suspect we could potentially see sellers return toward this 6850-6900 area. This morning the futures opened a little lower, E-minis(S&P) -0.10%, NQZ5 -0.05%. On the day I suspect dips toward 6750-6780 should now be supported as the market looks to challenge the 6850-6900 area again. Over the medium-term though will be watching for any signs of stalling up here, or if this market just goes on to start a new series of all-time highs.

- Wei Li(CIS BlackRock) on LinkedIn - Narrowness in US equities merely MIRRORS narrowness in the US economy, with non-residential investment contribution to growth 3X this year driven by AI related spend. Mag 7 earnings this quarter is tracking 27%, far exceeding the 14% expected at the beginning of the reporting season. Concerns over circular financing will be tested by eventual demand, and no one can know with conviction at this point. Meanwhile I stay overweight AI+.

- Thomas Thornton posted on X: “SPX with new DeMark Sequential sell Countdown 13 on Friday.”

- Bloomberg reports: “A Hawkish December Fed Cut Would Be a Problem for Risk Sentiment. The Federal Reserve would confirm it prioritizes a fading inflation scare over weakening labor markets and tightening credit conditions with a hawkish December rate cut, unwilling to ease further until something breaks. This message would drag risk sentiment lower as markets reprice a Fed that’s making a policy error.” {NSN T6GB0AKIJH8M <GO>}

- The S&P 500 Index Average True Range(ATR) for the last 10 Trading days: 97 Points

Fig 1: S&P 500 Index Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

US TSYS: A Weak End Friday, 10-Yr Above 4.00%

US treasury futures finished weak on Friday on low volumes, impacted by Thanksgiving Holidays. The 10-Yr bond future finished the US session at 113-11+ -0-07 for the day but remained up +0-04+ for the week. The move lower from TYZ5 sees it move away from RSI overbought having touched +63 (+70 is overbought), whilst it remains above all major moving averages. TYZ5 has opened in Asia at 113-11 this morning, and is down -02 at 113-09+

On a day that was expected to be a light trading day with many market participants out, yields finished higher, with the long end weakest. For the 10-Yr the 4.00% level continues to act as a semi-anchor that it oscillates around. At one stage last week, driven primarily by FEDSpeak, the 10-Yr had declined -7bps for the week to a closing low of 3.995% only to weaken into the end of the week to finish above 4.00%

- The 2-Yr ended up +1.4bps at 3.491%

- The 5-Yr up +2.7bps at 3.597%

- The 10-Yr up +2bps at 4.015%

- The 30-Yr up +2.2bps at 4.664%

As the data flow continues, looking at the week ahead, the bond market will eye key data releases for potential further guidance on the upcoming rates decisions, specifically:

- Monday, December 1: ISM Manufacturing PMI, Construction Spending, and S&P Global Manufacturing PMI.

- Wednesday, December 3: ADP Employment Change, Industrial Production, Capacity Utilization, and ISM Services PMI.

- Thursday, December 4: Initial Jobless Claims and Continuing Jobless Claims.

- Friday, December 5: Personal Consumption Expenditures (PCE) price index, Personal Income, Personal Spending, and Michigan Consumer Sentiment.

For the issuance calendar overnight the focus for Monday will be Bill issuance with a 6-week maturity.

JGBS: Futures Downtrend Intact, Dec Hike Pricing Around 64%, Ueda Speech Later

On Friday, JGB futures finished the post Tokyo close period at 134.95, -.18 versus settlement levels. This leaves the technical bias in a downtrend, with downside focus on the Nov 19 low at 134.56, which is also the cycle low. Key short-term resistance has been defined at 137.30, the Sep 8 high.

- The key focus today will be on BoJ Governor Ueda's speech. The Japan Times via Bloomberg: "Market participants are increasingly speculating that the Bank of Japan could raise its policy interest rate in December, in light of recent remarks by senior BOJ officials indicating the central bank's willingness to revise its monetary policy soon."

- Market pricing for a Dec hike has risen in recent sessions, with an implied rate around 0.63%, versus a current effective policy rate of 0.477%. The Jan meeting has close to a full 25bps hike priced in. These odds could shift depending on Ueda's bias today. A wait and see bias from Ueda (needing to see early 2026 data etc) could lower Dec hike odds notably.

- Before Ueda speaks (which is due around 10:05am local time), we have Q3 capex spending, along with company sales and profits. Capex (ex software) is expected at 5.4%y/y, versus 5.2% prior.

- In the cash JGB space the 10yr finished last week just above 1.81%. Recent cycle highs were around 1.845%. The 2yr was near 0.98%, eyeing an upside test of 1.00%, although has only moved moderately higher in recent weeks. The 30yr finished up last week at 3.35%. The 2/30s curve was at +237bps, just under recent highs (+242bps).