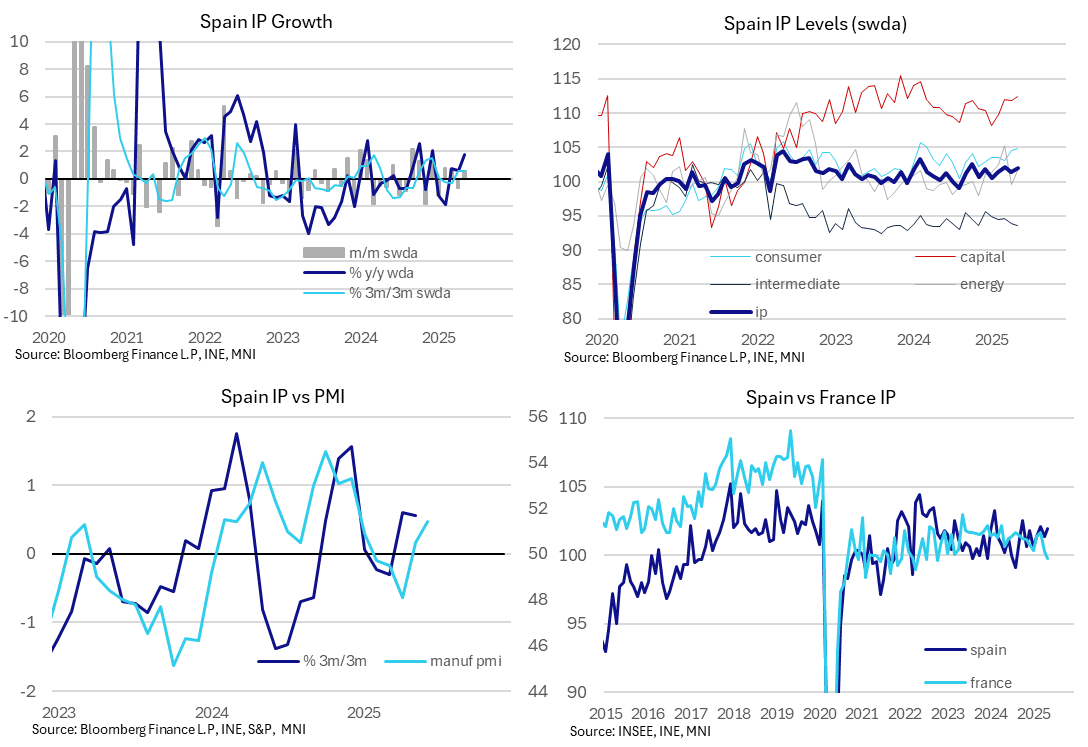

SPAIN DATA: Industrial Production Trend Remains Positive In Line With PMIs

Spanish industrial production rose 0.6% M/M in May, above April’s soft -0.7% reading and the 0.4% consensus (albeit based on just five projections ranging between -0.6% and +1.0%). Spain’s economic outperformance post Covid has been more driven by the services sector (i.e. tourism) rather than industry, but in recent months IP has shown some outperforming divergence from the likes of France.

- 3m/3m IP growth was steady at 0.6% in May, after -0.3% in March and -0.2% in February. On an annual basis, growth of 1.7% Y/Y (vs 0.6% prior) was the strongest since December.

- Consumer goods production rose 0.3% M/M (durables -0.5%, nondurables +0.4%), while capital goods production rose 0.6%. Intermediate goods fell 0.3%, while energy rose 2.1%

- As in France, Spanish intermediate goods production has seen the most sluggish trend since 2022. Meanwhile, capital goods production has outperformed. That goes some way in explaining the divergence in gross fixed capital investment trends between Spain and France since Covid (albeit with Spain recovering from a lower base).

- Looking ahead, the Spanish June manufacturing PMI rose to 51.4, above the 50.5 consensus and prior for the highest since December 2024. There were some signs of softness in the report though, particularly in export markets. From the release:

- “Operating conditions in Spain’s manufacturing economy improved in June. Output increased to a solid degree, whilst orders rose for the first time since January. Employment growth was sustained, and confidence in the outlook edged up to its highest since February”.

- “However, some panellists reported a subdued business environment overall, especially in international markets where tariff related uncertainty led to a drop in new export sales. Manufacturers also remained reluctant to purchase new inputs, preferring instead to utilise existing stocks especially in the face of ongoing supplier delivery delays”.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

SWAPS: Long End Of German ASW Curve Continues To Outperform

German ASWs vs. 3-month Euribor 0.2-0.7bp firmer on the day, with the long end of the swap curve outperforming once again.

- The Buxl spread hovers around -35bp, eying January closing highs at -34.08bp.

- In outright swaps, Commerzbank note that “Dutch dynamics are increasingly visible at the ultra-long end. The 10-/30-Year curve has pushed to a new high, accompanied by a tightening in the 3s/6s basis, pointing to fixed paying interest in the ultra-long curve. The decoupling of Buxl spreads from the swap curve also indicates that the dynamics are swap-driven. Over the past five sessions, Buxl spreads have richened by ~4bp, outperforming the entire ASW structure”.

- They go on to flag that “it is hard to tell whether these dynamics are the result of Dutch flows in anticipation of the pension fund transition, or fast money anticipating these flows. If anything, the collapse of the Dutch government has probably removed the tail risk of a delay to the pension reform. The normalisation of the EUR curve compared to other markets therefore has further to run”.

EUROZONE DATA: May Services PMI Revised Higher; Composite Remains Just Above 50

The Eurozone May services PMI was revised up to 49.7 (vs 48.9 flash, 50.1 prior), following an upward revision in France and a stronger-than-expected Italian print. We estimate the Germany/France combined services PMI at 47.9 (vs 48.3 prior), and the ex-Germany/France measure at 52.8 (vs 51.6 flash, 53.2 prior).

That helps the composite PMI remain just about in expansionary territory for the fifth consecutive month (it has had a range of 50.2-50.9 through this year), consistent with positive, but sluggish growth. A reminder that the ECB is expected to revise its GDP projections lower at tomorrow's decision, but this will likely be centred in 2026. See more in our ECB preview.

Notes from the Eurozone-wide services release:

- "New business continued to decline, stretching the current sequence of decrease to four months. The deterioration in demand for services was the most pronounced in six months, albeit modest. A sharper drop in international orders was partly to blame, with export sales also falling to the quickest degree since November last year".

- "Outstanding business volumes were depleted for a thirteenth successive month in May. This was facilitated to some degree by greater workforce numbers, with services employment rising again"

- "Muted hiring activity came amid another month of subdued business confidence. Although future output expectations strengthened, they remained weak by historical standards".

- "There was little movement on the inflation front, with rates of input cost and output charge inflation holding fairly close to those seen in April and remaining above the respective survey averages".

BONDS: Longer end Futures are leading Bonds lower

- US Cash USTs are trading cheaper and the belly is underperforming.

- While the early price action saw the US Curves mostly unchanged, worth watching the longer end part of the Curve in US Treasuries and on this side of the Pond, Buxl (UBM5) look to break below 121.00, USU5 tests 112.00 and WNU5 is through 115.00.