OIL PRODUCTS: India’s Crude Throughput to Dip in Q3: Platts

Jul-10 10:47

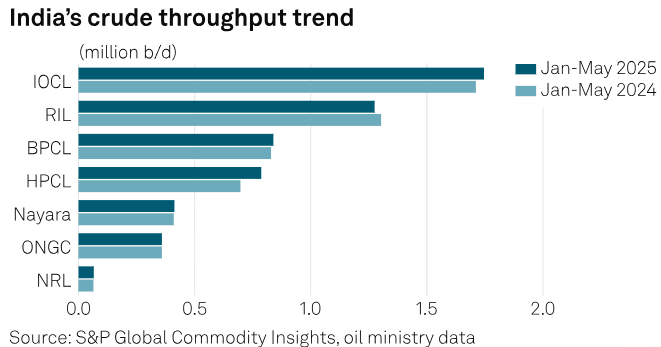

India’s crude oil throughput is expected to dip in Q3 2025 due to reduced transport fuel demand during the monsoon, Platts said.

- However, analysts forecast a rebound in Q4 driven by festive season demand and rising exports.

- Crude processing between January- May rose over 2% year-on-year to 5.49m b/d, supported by strong performance at HPCL’s Vizag refinery and IOC’s Panipat and Paradip plants.

- Refinery utilisation remained robust, averaging 106% in May and 105% for April–May.

- Private refiners also showed strength, though Reliance’s throughput dropped slightly in the April–May period.

- However, January–May imports were up 1.5%, supported by strong domestic and export demand. Russia remained India’s top crude supplier, while US imports surged 51% year-on-year.

- With the monsoon impacting short-term runs, the outlook for Q4 remains positive. India’s increasingly diversified import strategy—now sourcing less than 45% from the Middle East—adds resilience amid ongoing geopolitical tensions, Platts said.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

OPTIONS: Expiries for Jun10 NY cut 1000ET (Source DTCC)

Jun-10 10:46

- EUR/USD: $1.1300-20(E1.5bln), $1.1370-75(E920mln), $1.1400-25(E2.1bln)

- USD/JPY: Y143.90-00($1.1bln), Y144.85-00($805mln)

- AUD/USD: $0.6420(A$771mln), $0.6460(A$529mln)

- USD/CAD: C$1.3695($869mln)

GILTS: Basis trade unwind

Jun-10 10:45

G U5 3.9k at 92.54.

- This is an unwind from the G U5 3.9k at 92.56 before the syndication earlier.

STIR: Fed Implied Rates A Touch Softer One Day Out From CPI

Jun-10 10:44

- Fed Funds implied rates are up to 1.5bp lower on the day for 2025 meetings, following a pullback off overnight highs in US equity futures following weakness in China and HK equities.

- US-China talks in London have entered a second day today.

- Cumulative cuts from 4.33% effective: 0bp Jun (next week), 3.5bp Jul, 18bp Sep, 30bp Oct and 46bp Dec.

- The SOFR implied terminal yield of 3.355% (SFRZ6, -2bp) is back closer to ~100bp of cuts having closed Friday at ~90bp of cuts ahead.

- Markets will be on headline watch today with a blank data docket after the earlier release of the NFIB small business survey. US CPI is in focus tomorrow (MNI Preview).