OIL: India’s BPCL Signs Oil Supply Deal with Petrobras: Reuters

Jan-23 13:26

India's Bharat Petroleum Corp (BPCL) will lift 12m bbl of crude from Brazil's Petrobras in 2027, dou...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

STIR: Repo Reference Rates

Dec-24 13:03

- Secured Overnight Financing Rate (SOFR): 3.66% (-0.02), volume: $3.255T

- Broad General Collateral Rate (BGCR): 3.64% (-0.02), volume: $1.306T

- Tri-Party General Collateral Rate (TCR): 3.64% (-0.02), volume: $1.272T

- (rate, volume levels reflect prior session)

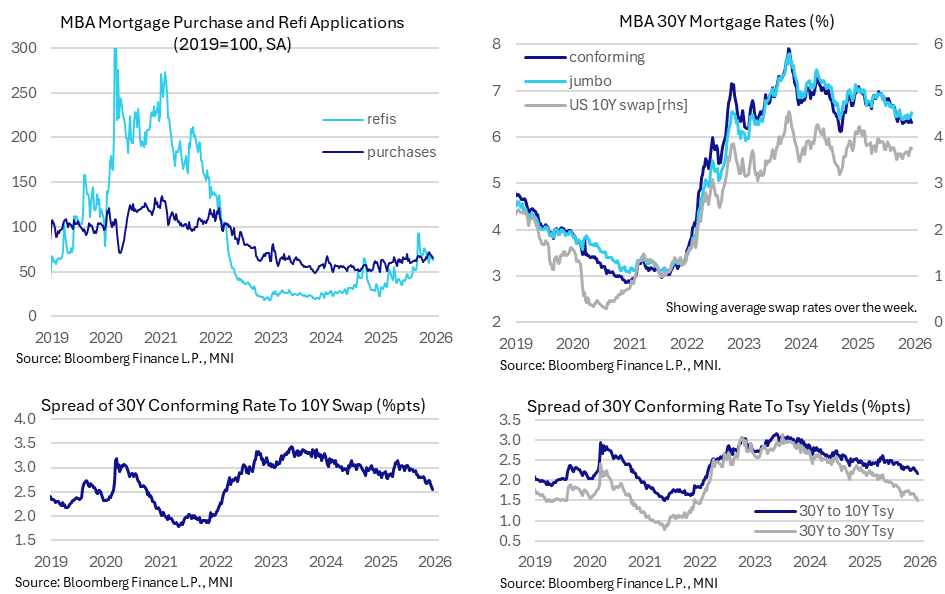

US DATA: Mortgage Applications Slip Further Despite Latest Spread Tailwind

Dec-24 12:31

- MBA composite mortgage applications slipped another -5.0% (sa) last week after the -3.8% in the week prior, on balance more than reversing a refi-driven increase in early December.

- Refis fell -5.6% after -3.6% and +14.3%, whilst new purchases fell -3.7% after -2.8% and -2.4%.

- Relative levels to 2019 averages: 62% for composite, 66% for new purchases (this peaked at 72% in late November) and 62% for refis (this peaked at 93% in a mid-September spike).

- There was little sign of response from a 7bp decline in the 30Y conforming rate to 6.31%, reversing the 5bp increase the week prior to come close to the 6.30% in October that was the lowest since Sep 2024.

- There could however be some distortion ahead of Christmas, with an unusually sharp divergence with jumbo rates which increased 8bp on the week to 6.52%. That 21bp spread over conforming was the widest since Oct 2024.

- There continues to be an increasingly significant tailwind from narrowing spreads over swap rates, with the 30Y conforming to the average 10Y swap rate spread narrowing 6.5bps to 255bp for a fresh low since Mar 2022.

- It compares with the peak of 315bp in May in post-tariff disruption, 285bp averaged in 1Q25 and 302bp averaged in 2024.

US TSYS: Mildly Firmer; Jobless Claims & 7Y Supply Ahead Before Early Close

Dec-24 12:10

Treasuries are mildly firmer overnight, sitting firmly within yesterday’s strong GDP-induced range amidst tiny futures volumes on Christmas Eve. Cash closes early at 1400ET and futures at 1315ET today.

- Reuters headlines that Japan is considering reducing super-long debt issuance and pausing an increase in 10Y issuance saw JGB futures gain on tiny volumes but with little spillover to Treasuries (after greater sensitivity to post-BoJ JGB moves).

- Cash yields are 0.5-1bp lower on the day, consolidating yesterday’s pullback after 10Y yields tested 4.20% with a high of 4.2001%, currently trading at 4.155%.

- TYH6 trades at 112-12 (+02+) in narrow ranges on tiny cumulative volumes of 120k.

- It sits comfortably within yesterday’s range of 112-17 (90mins before GDP) and 112-01+ (before a softer labor differential in the Conf Board survey and that yield test).

- Resistance remains intact at 112-21+ (50-day EMA) whilst yesterday’s low came close to the bear trigger at 111-29 (Dec 10 low). Further downside traction will again open the 4.20% yield level, which today equates to 112-02+ to continue to offer support just above that bear trigger.

- In rates space, Fed Funds futures see low chance of a Jan rate cut (3bp priced), with April less timely at a cumulative 17.5bp (22bp pre-GDP). A cut is still clearly expected in June under a new Fed chair (30.5bp vs 34.5bp pre-GDP).

- SOFR futures are unchanged to 1 tick firmer, with the terminal implied yield at the higher end of recent ranges at 3.155% (Z6).

- Today’s data focus is on weekly jobless claims at 0830ET.

- Attention should then turn to issuance, with the $44bn 7Y auction at 1130ET plus 4wk/8wk/17wk bills (1000/1000/1130ET). Yesterday’s 5Y saw little reaction to a small 0.1bp tail and the bid-to-cover slipping from 2.41 to 2.35.