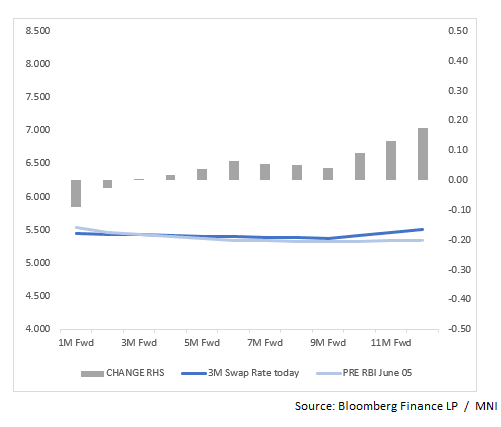

INDIA: India Updated Swaps Pricing Vs. Pre-RBI Meeting Levels

Jul-16 02:41

- We assess the change in expectations for rate move via an analysis of the swaps curve. We compare the three month on a forward basis each month out to 12 months. We look to use this as an indicator for a change in expectations from week to week, comparing it to the FBIL Overnight Mumbai Interbank Outright Rate (FBIL- Overnight MIBOR) as per market standard.

- The swaps curve has 4bps of increases over the next 12 months up from 12bps early last week. By way of comparison, the BBG MIPR function has decreases of 4bps over the next 12 months, and -2bps over the next 3 months

- The RBI has signaled that the recent cut of 50bps was designed to front load monetary policy, with markets suggesting that that could be the end of the cutting cycle. The market has progressively priced out cuts. Towards the end of May the swaps curve had priced in approximately 30bps of cuts over the following twelve months. The signaling from the RBI has done its job re-pricing expectations.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

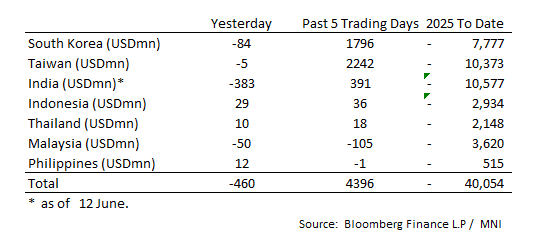

ASIA STOCKS: Large Outflow for India Thursday

Jun-16 02:34

Large inflows across major markets was the theme last week, despite India seeing large outflow on Thursday and flows tapering off on Friday for other markets.

- South Korea: Recorded outflows of -$84m Friday, bringing the 5-day total to +$1,796m. 2025 to date flows are -$7,777. The 5-day average is +$359m, the 20-day average is +$184m and the 100-day average of -$85m.

- Taiwan: Had outflows of -$5m as of Friday, with total inflows of +$2,242 m over the past 5 days. YTD flows are negative at -$10,373. The 5-day average is +$448m, the 20-day average of +$63m and the 100-day average of -$112m.

- India: Had outflows of -$383m as of the 12th, with total inflows of +$391m over the past 5 days. YTD flows are negative -$10,577m. The 5-day average is +$78m, the 20-day average of -$24m and the 100-day average of -$86m.

- Indonesia: Had inflows of +$29m Friday, with total inflows of +$36m over the prior five days. YTD flows are negative -$2,934m. The 5-day average is +$7m, the 20-day average +$14m and the 100-day average -$29m.

- Thailand: Recorded inflows of +$10m as of Friday, with inflows totaling +$18m over the past 5 days. YTD flows are negative at -$2,148m. The 5-day average is +$4m, the 20-day average of -$23m and the 100-day average of -$21m.

- Malaysia: Recorded outflows of -$50m as of Friday, totaling -$105m over the past 5 days. YTD flows are negative at -$3,620m. The 5-day average is -$24m, the 20-day average of -$28m and the 100-day average of -$24m.

- Philippines: Saw inflows of +$12m yesterday, with net outflows of -$1m over the past 5 days. YTD flows are negative at -$515m. The 5-day average is $0m, the 20-day average of -$15m the 100-day average of -$5m.

AUSTRALIA: Consensus Expects Labour Market Remained Tight In May

Jun-16 02:26

The highlight of the week, which doesn’t include many events, will be May jobs data on Thursday. Bloomberg consensus is expecting that the status quo continued last month with Australia’s labour market remaining tight. A 20k rise in new jobs is forecast, in line with the 3-month average, with the unemployment and participation rates stable at 4.1% and 67.1% respectively.

- Westpac’s lead index for May is released on Wednesday. It posted two straight monthly falls in March and April but the 6-month rate, which leads detrended growth by 3 to 9 months, remains positive. While it continues to signal a recovery over H2 it is now suggesting that it should be slower. April fell 0.01% m/m to be up 0.2% 6m/6m annualised down from 0.5%.

- There are no RBA events this week.

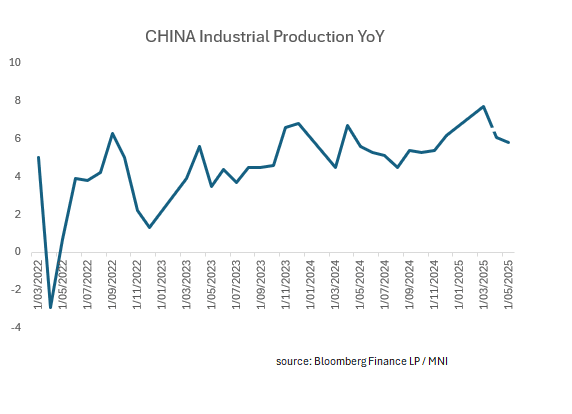

CHINA: Industrial Production Expands +5.8% YoY in May

Jun-16 02:18

- For a second consecutive month, China's industrial production grew less than the prior month.

- Peaking in March just prior to the implementation of tariffs at +7.7% May's result was lower at +5.8%.

- The 3 year average for Industrial Production expansion is +4.5%

- Mining was flat on last month at +5.7%.

- Manufacturing was lower at +6.2% (from +6.6%)

- Auto manufacturing rose by +11.2%