EM ASIA CREDIT: India: Reliance Industries Rating Upgraded

" Reliance's long-term rating was upgraded by S&P to A- from BBB+." - Bbg

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EURJPY TECHS: Corrective Pullback

- RES 4: 180.37 1.500 proj of the Jul 31 - Sep 29 - Oct 2 price swing

- RES 3: 180.00 Psychological round number

- RES 2: 178.94 1.236 proj of the Jul 31 - Sep 29 - Oct 2 price swing

- RES 1: 178.82 High Oct 30 and the bull trigger

- PRICE: 176.28 @ 16:17 GMT Nov 4

- SUP 1: 176.10 Low Nov 4

- SUP 2: 175.00 50-day EMA

- SUP 3: 173.92 Low Oct 6 and a gap high on the daily chart

- SUP 4: 173.36 Bull channel support drawn from the Feb 28 low

The trend in EURJPY is bullish and the latest pullback appears corrective. The cross traded to a fresh cycle high last Thursday, confirming a resumption of the primary uptrend. This opens 178.94 next, a 1.236 projection of the Jul 31 - Sep 29 - Oct 2 price swing. Today’s move down has resulted in a breach of 176.65, the 20-day EMA. This signals scope for a deeper correction towards the 50-day EMA, at 175.00. The bull trigger is 178.82, Oct 30 high.

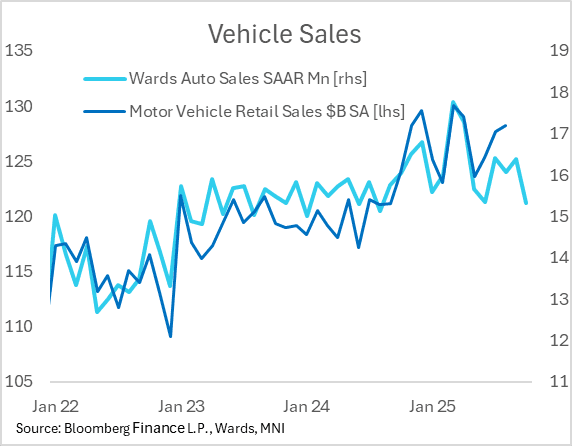

US DATA: Light Vehicle Sales Could Drag On October Retail Sales

Light vehicle sales weakened considerably in October per data from Wards Automotive, coming in at 15.32 million on a seasonally-adjusted, annual basis in volumes, down from 16.39 million prior (and weaker than the 15.50 million consensus).

- This was the lowest figure since August 2024 and represented a 6.5% M/M drop, the biggest in 5 months. The dropoff is due to the end-September expiry of tax credits for purchasing electric vehicles. Overall, sales are more or less where they typically printed in 2023-24 before tariff-related frontrunning/volatility in 2025.

- After falling 4.2% M/M in Jun in the Retail Sales report, it rose 1.4% in July and 1.9% in August (all nominal, SA terms) while of course we don't yet have the September report due to government shutdown. The Wards series saw a 2% fall in June, followed by a 7% rise in July, 2% fall in August, and a 2% rise in September.

- Autos is usually the largest single category of monthly retail sales so could prove to be a major drag if translated into the Retail Sales series (though ex-auto sales look to have remained solid per other indicators including Chicago CARTS and Redbook), not to mention overall PCE, though sometimes this is reflected into the Retail Sales series with a slight lag.

- With or without an official October release by the Census Bureau on the scheduled Nov 14 date, we will post a wrap-up of the "alternative" retail sales data at that time.

US TSYS/SUPPLY: Analysts Eye Distant Upsizings, Bill Sales To Rise (3/3)

Analysts' outlooks for Wednesday's refunding reflect almost no expectations for any major changes, but there is increasing attention being paid to the likelihood of increased bill issuance ahead as coupon sizes aren't increased until well into 2026 at least. Some selected views in alphabetical order of institution:

- Citi: Next coupon upsizing in Nov 2026 “but there is a growing risk that Treasury can avoid increasing coupons until 2027”. "“Treasury has not given strong guidance on the ‘optimal’ T-bill level, but we think there is scope for this to increase to 25%.”

- Danske: Next upsizing in 1H 2026. "“the Treasury could align with the TBAC recommendation that T-Bills should constitute 20% of net issuance. This would require increasing the size of coupon auctions by approximately USD250bn per year starting in FY26.”

- Deutsche: Next upsizing in August 2026 "with larger adjustments in the 2Y to 5Y sector". When coupons are eventually upsized, “increases would extend over many quarters, keeping net coupon issuance at around 75% of projected borrowing and stabilizing the bill share of total debt around 25% over the longer run.”

- Jefferies: Next upsizing not until after FY 2026.

- Morgan Stanley: Next upsizing in February 2027.

- NatWest: No changes to nominal coupon sizes in 2026, risks leaning to even further delays.

- TD Securities: Next upsizing in Nov 2026. Notes re this week's refunding “we see a risk that the Treasury market reacts positively if Treasury spends a significant amount of time focused on the Fed's balance sheet runoff ending and the resumption of reserve management purchases next year. This could hint to investors that Treasury intends to delay auction size increases (which we expect to occur late next year) or even decrease long-end auction sizes to help bring yields lower.”

- Wells Fargo: Next upsizing in early 2027. “There are some risks of additional federal budget deficit widening next year if the Supreme Court strikes down the President's IEEPA authority for imposing tariffs, but the end of quantitative tightening and the eventual resumption of balance sheet growth by the Federal Reserve should help soak up a big chunk of the bill supply that's coming in the year ahead.”