RBNZ: Increased Spare Capacity Drove OCR Path Lower

Governor Hawkesby reiterated that Q2 growth had disappointed and MPC member Silk clarified it was due to an “uncertainty shock”. This lower starting point then drove the downward revision to the OCR path as there was more spare capacity than previously estimated and needed to keep inflation sustainably in the band. Whether the MPC follows its OCR profile will be determined by developments.

- While views over the risks were diverse, the MPC was unanimous over the central profile for the OCR. This range of opinions reflects current heightened uncertainty.

- Chief Economist Conway noted that policy is now “around neutral” which means that it’s about the effect on the economy rather than exactly where it is relative to neutral. The concept is more important when rates are clearly above or below it.

- The MPC expected the NZD to decline following its decision given the vote and OCR path and is happy that the market moves will help to ease monetary conditions.

- The focus remains on the medium-term, which Hawkesby stated the RBNZ can influence. He noted that there is a 50% chance that inflation will exceed the 3% band ceiling in the short term, but that is a time frame they can’t control. He advised economic participants to make decisions based on “low and stable” inflation.

- The worst is over for the economy with the “uncertainty shock” now waning. It is estimated that around 50% of the 250bp of monetary easing has been transmitted and so there is a lot to come which is expected to boost consumption and dwelling investment.

- It appears that the replacement for external MPC member Buckle will be made by October but Hawkesby gave little away regarding when there will be a new Governor or who. He has applied but Chief Economist Conway and Assistant Governor Silk have not.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

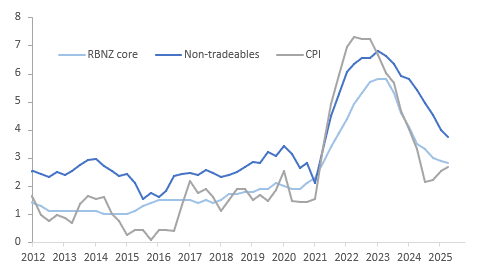

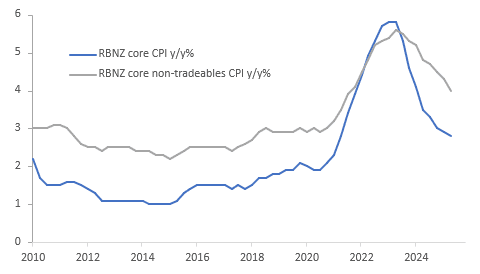

NEW ZEALAND: RBNZ Core Inflation Measure Moderates Slightly

The RBNZ’s sector factor model result for Q2 was in line with other underlying CPI measures showing that core inflation remained below the top of the 1-3% target band. Its measure of core inflation eased 0.1pp to 2.8% y/y, the lowest rate since Q2 2021, and is now only 0.1pp above headline CPI. Underlying non-tradeables also continued to moderate. Thus with activity data still lacklustre, another 25bp rate cut on August 20 seems likely coinciding with an update in staff forecasts.

NZ inflation y/y%

- The sector factor model’s estimate of core non-tradeable inflation declined to 4.0% y/y in Q2 from 4.3%, the lowest in almost 4 years. The headline measure dropped 0.3pp to 3.7%.

- Underlying tradeable inflation remained very low at 0.7% y/y up slightly from Q1’s 0.5%, compared to the headline at 1.2% y/y.

- Earlier today Q2 trimmed mean CPI was steady at 2.5% y/y but CPI ex food, fuel & energy ticked up 0.1pp to 2.7% y/y.

NZ underlying inflation y/y%

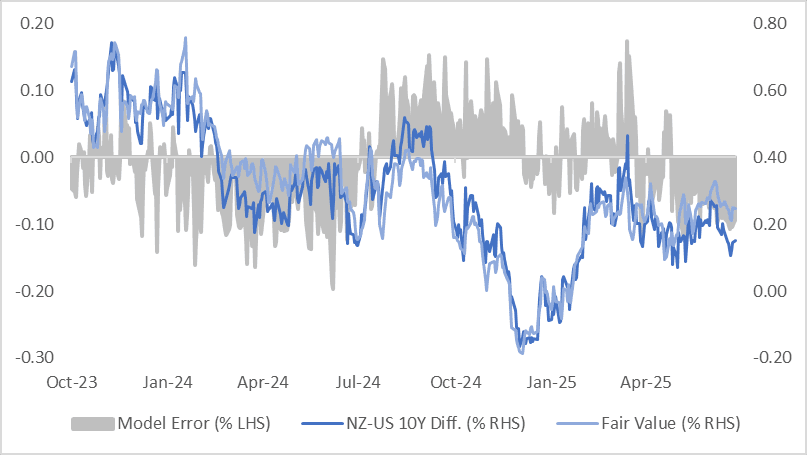

BONDS: NZ-US 10Y Differential Near Mid-Point Of This Year’s Range

NZGBs are 3-5bps richer today on the day and after today’s Q2 CPI data.

- With cash U.S. Treasuries not trading during today’s Asia-Pac session (due to the Japan holiday), and U.S. futures trading slightly higher, the move leaves the NZ–US 10-year yield differential around +15bps.

- At this level, the spread remains near the midpoint of the -20bps to +40bps range observed year-to-date.

- However, a simple regression of the 1Y3M forward swap spread against the 10-year yield differential over the past 18 months suggests the differential is currently about 10bps below its estimated fair value of +25bps.

- The regression’s standard error has remained within ±15bps over the past year, underscoring some inherent variability in the relationship.

- The 1Y3M spread continues to anchor market expectations around the longer-term path of yield convergence.

Figure 1: NZ-US 10-Year Yield Differential

Source: Bloomberg Finance LP / MNI

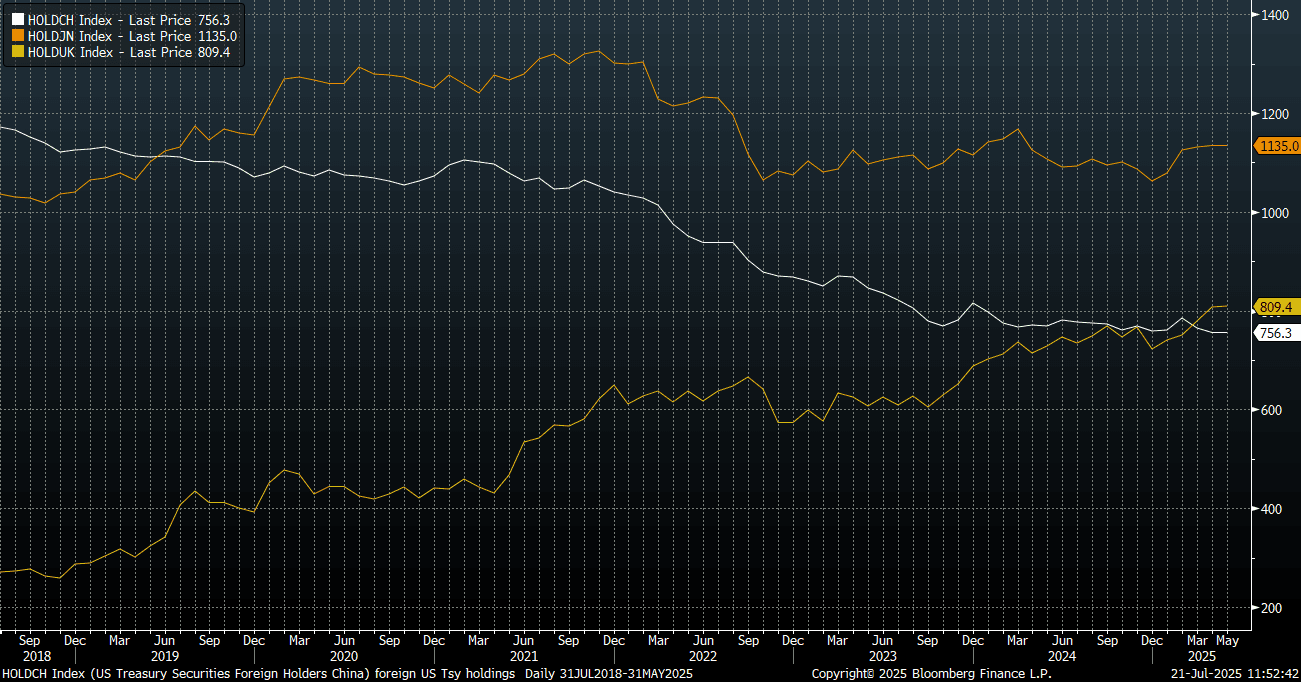

CHINA: China To Reduce UST Holdings Further

- A news article from the Government run China Daily this morning indicates that a strategic move is beginning in China, that may have profound implications for the US and their fiscal position.

- China Daily reports that is is a 'strategic necessity' for the scaling back of holdings in US Treasuries, given the declining confidence in the dollar as the reserve global currency.

- The article states that China intends to pursue a more balanced, controllable allocation of FX reserves and likely to increase its holdings of non-dollar assets, including financial instruments of Asian trading partners.

- Yu Yongding, an academic member of the Chinese Academy of Social Sciences, called for China to continue reducing US government debt holdings in an orderly manner and that in extraordinary times, extraordinary measures are called for.

- The latest Treasury holding data shows the UK taking over China as the third largest holder of US Treasury securities, see the chart below (China holdings are the white line).

- China has total holdings of USD 756.3 billion, to now rank third in largest holdings behind Japan and UK, according to US Treasury data. This shift marks a significant moment in the global financial landscape. The last time the UK ranked ahead of China in US debt ownership was in 2000—more than two decades ago. China holdings have flatlined somewhat in recent years, after falling through much of 2021-2023.

- The Governor of the PBOC Pan Gongsheng has been clear in his assessment of the risks associated with the USD dominance and that the fiscal position of the US economy, could spill over into global markets.

- China's FX reserves recently increased to US$3.32tn, its highest level in a decade.

Fig 1: China, Japan and UK Treasury Holdings

Source: Bloomberg Finance L.P./MNI