EMISSIONS: IETA Survey Shows 46% Respondents Expect EU ETS 1,2 Merge

Nov-12 15:36

An IETA survey showed that 46% of 143 respondents expect that EU ETS 2 will merge into the ETS 1, according to its latest report.

- 33% anticipate an integration after 2030, while 13% expect before 2030.

- 14% expect no future integration, while 40% did not take a position.

- EUA DEC 25 up 1.17% at 81.59 EUR/t CO2e today

- ICE EU ETS 2 Dec28 was priced at €69.74/t on 11 Nov.

- EEX EU ETS 2 Dec28 was priced at €44.53/t on 11 Nov.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EURIBOR OPTIONS: ERZ5 Call Buyer

Oct-13 15:34

ERZ5 98.25 call, paper pays 0.5 in 7.5k

US STOCKS: Equities Roundup: Chip Makers, Materials Lead Early Monday Rebound

Oct-13 15:29

- Stocks have recovered approximately half of Friday's sell-off in the first half of Monday trade, inside narrow ranges with prices off highs amid moderate profit taking ahead midday. Overall trade was relatively subdued due to the Columbus Day holiday.

- Currently, the DJIA trades up 579.6 points (1.27%) at 46,059.93, S&P E-Minis up 96.25 points (1.46%) at 6,692, Nasdaq up 438.1 points (2%) at 22,645.79.

- Information Technology and Materials sector shares led the rally, semiconductor makers outperforming: Broadcom Inc climbed +9.71% after reports of an accelerated AI chip deal with OpenAI , Monolithic Power Systems +7.55%, ON Semiconductor +6.17%, Microchip Technology +5.30% and HP Inc +4.50%.

- Materials sector gainers included Albemarle Corp, up +8.09% apparently on a short squeeze tied to lithium mining, Freeport-McMoRan +4.92%, Dow Inc +4.21%, Newmont Corp +4.12%.

- Conversely, Consumer Staples and Health Care sector shares led declines in the first half: Conagra Brands -2.93%, Monster Beverage -2.69%, J M Smucker Co -2.51% and The Hershey Co -2.30%. Pharmaceuticals weighed on the Health Care sector: Regeneron Pharmaceuticals -2.39%, Humana -2.29%, Edwards Lifesciences -0.65% and Cardinal Health -0.52%.

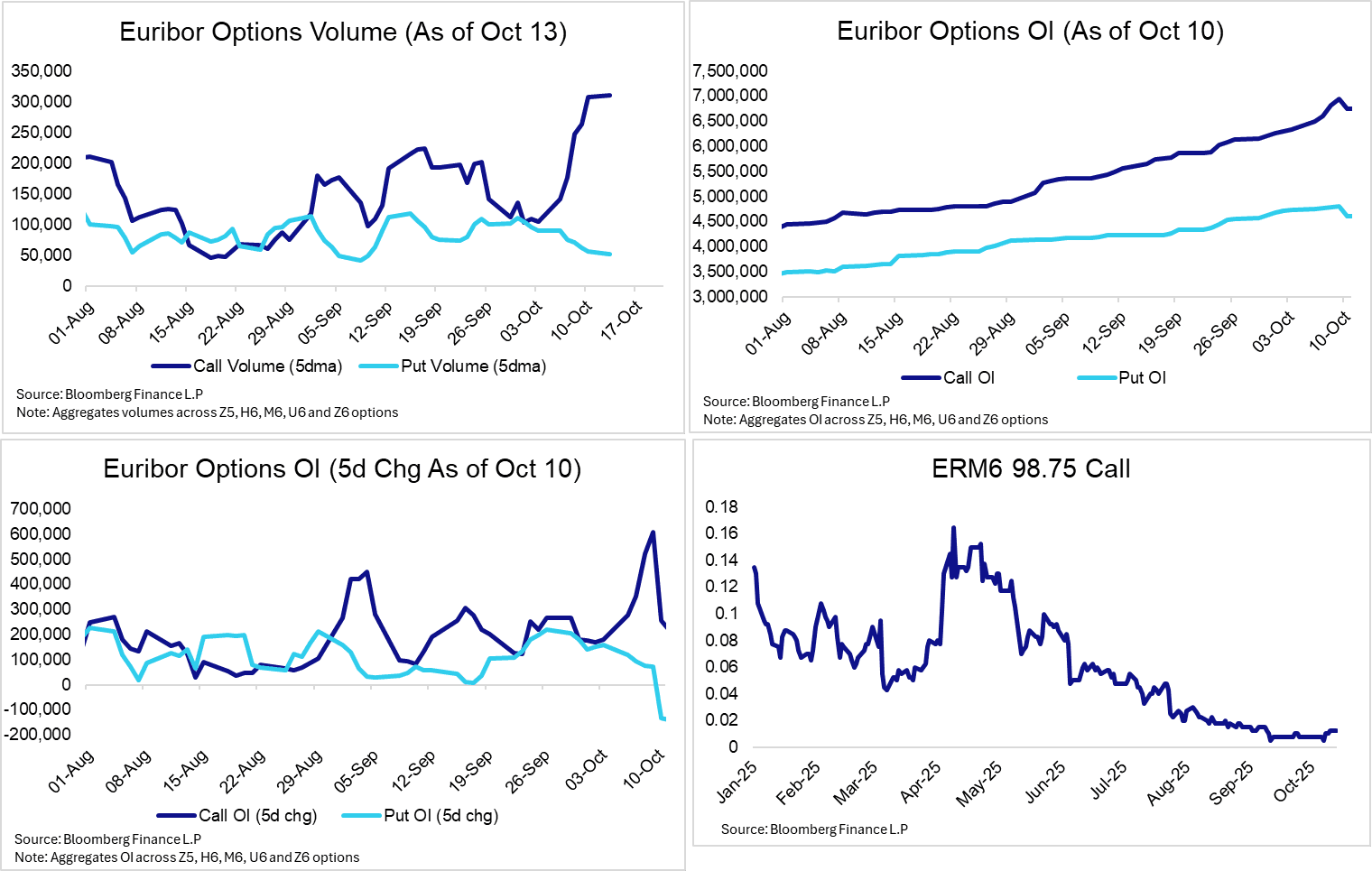

EURIBOR OPTIONS: Light Calendar Hasn’t Impeded EUR STIR/EGB Options Activity

Oct-13 15:25

Despite today’s light regional data calendar and the US Columbus Day holiday, options activity in EUR STIRs and EGBs has been healthy. Looking at the front-end, there’s been a notable uptick in aggregate call volumes and OI (latter as of last Friday) over the last week, with put activity less pronounced.

- Despite a softening of stance over the weekend, the US administration’s tariff threats again China on Friday served as a reminder that trade policy uncertainty is still a risk to the global economic outlook.

- Tariff-related risks were a particularly important driver of dovish Euribor (i.e. ECB) options flows earlier this year. However, these concerns had moderated in recent months, aided by the US-EU trade agreement.

- Options in ERM6 have been favoured over the past week, with the June 2026 expiry providing sufficient flexibility around the potential timing of additional ECB rate cuts.

- ERM6 call OI stood at 1.7mln contracts as of Friday, an increase of almost 500k compared to October 3. In contrast H6 call OI has increased just over 100k over the same period. Today’s flow has included an outright buyer of the M6 98.75 call for 1.25 ticks in 20k. Despite the small uptick in vol over the past few sessions, this call remains historically cheap. It cost around 5 ticks in June/July and over 10 ticks in mid-April (pricing per BBG).

- As we highlighted last week, the heavy end of month data calendar (including PMIs, flash GDP and flash inflation) remains a key focus.