HYBRIDS: Hybrids: Week in Review

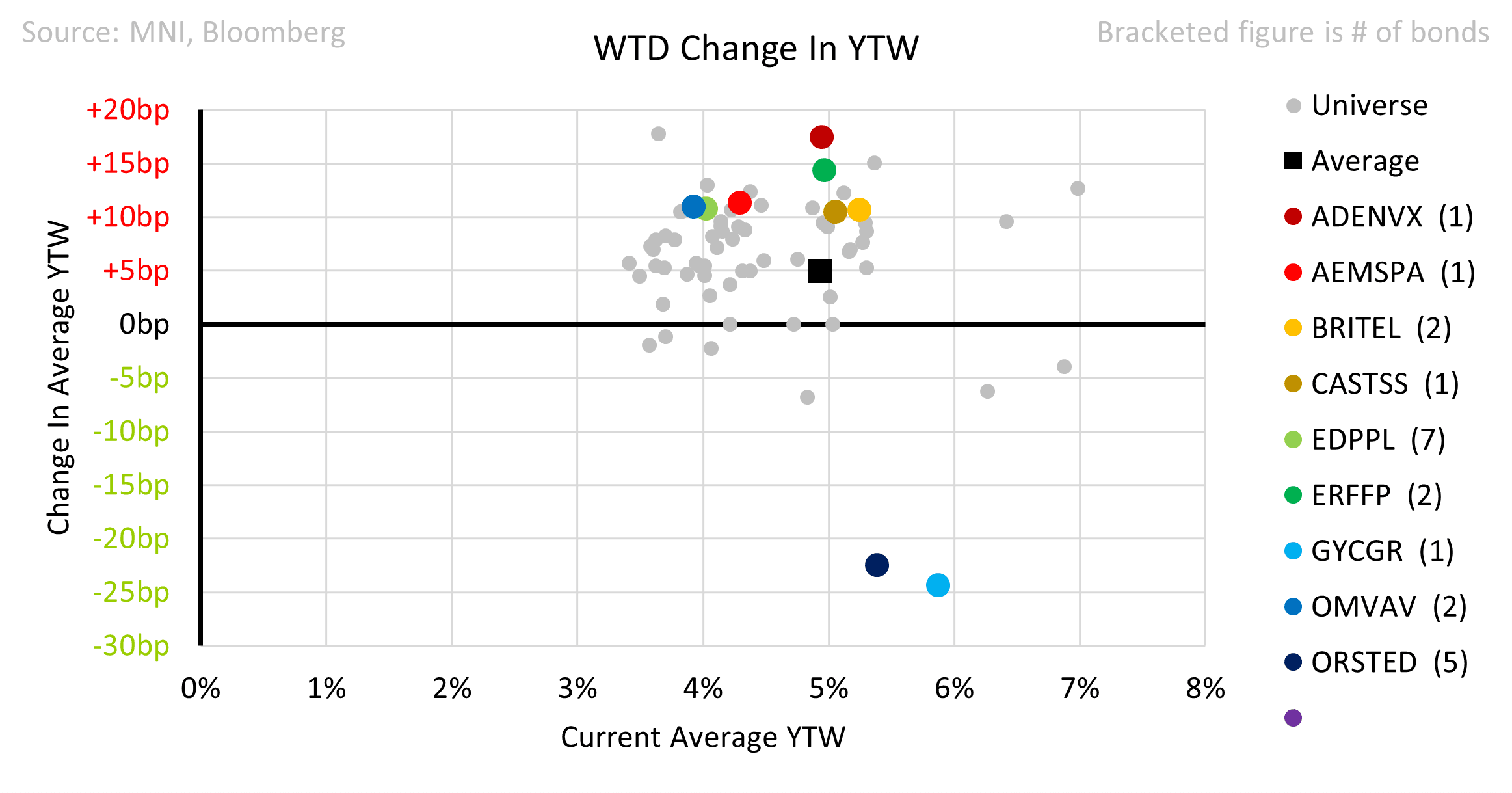

• Suedzucker’s return to the Perp market was phenomenal for existing holders and not so good for primary. The outstanding SZUGR Float Perps were not called in 2015 and have been an aberration in the market since. The bonds have never missed a coupon despite a brief cut to CC when the 5% cashflow clause threatened payment. The bonds were Tendered at Par, some 9 points above the undisturbed price. A relief for holders who sat through prices in the 70s in the past.

• The new SZUGR bond removed the cashflow clause and were consequently rated Ba1neg/BB, 2 notches better than the previous ISIN. We thought that 5.75% was fair but the bonds priced at 6% with a book that dropped from €1.6bn pre-rec to €1.2bn at finals. Bonds fell a further 90c in secondary.

• EDPPL issued €750m 30NC6.75 at 4.625%. This could be seen as an early refi of the May 2026 also €750m. Bonds -40c lower in secondary

• Arkema refinanced their €300m Call26 with a €400m NC5 @4.25% in-line with FV. Books were >2bn. Bonds were around reoffer in secondary.

• OMV’s IR team confirmed that the OMVAV 6.25 Call25 Perp had not formally been called but would be called in due course in accordance with the docs. The window for Redemption was also confirmed at any time from 90 days before the “First Call Date”.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US: WSJ Reports to Raise Focus on Imminent Bessent Appearance

These WSJ reports likely to raise the focus on Bessent's imminent appearance at the IIF in 4 minutes.

- He's set to be delivering keynote remarks and will "share his thoughts on the state of the global financial system". He will then hold a sit-down conversation with the IIF president. His remarks begin at 1000ET/1500BST and can be livestreamed here: https://vimeo.com/event/5054312/12805a306f

- His appearance follow closed-door remarks at an investor conference yesterday, where he supposedly said he sees de-escalation with China, with the current trade situation "unsustainable". Comments that will come into sharper focus given that WSJ report suggesting a "slashing" of import tariffs on Chinese goods - as well as a follow-up piece from the WSJ citing Bessent's influence in Trump deciding not to try to fire Powell.

BONDS: /STIR: EU & UK Markets Unwind Some Downside Growth Risks After WSJ Story

The move lower in bonds, as well as hawkish repricing in EUR & GBP STIRs, follows the WSJ report pointing to a potential dialling back of some of U.S. tariffs imposed on China.

- Those markets trade in a manner that points to less of a global growth shock, resulting in shallower central bank cutting cycles.

- ~60bp of further ECB cuts now priced through year-end vs. ~70bp at yesterday’s close.

- Meanwhile, ~85bp of BoE cuts are priced over the same horizon after showing over 90bp of cuts for much of today.

- Oil moves away from lows in sync.

US DATA: April Flash PMIs Disappoint Whilst Charge Inflation Accelerates

- Manufacturing PMI: 50.7 (cons 49.0) in April flash after 50.2 in March.

- Services PMI: 51.4 (cons 52.6) after 54.4 in March.

- Composite PMI: 51.2 (cons 52.0) after 53.5 in March, hitting a 16-month low.

- Highlights from the S&P Global PMI press release (in full here): "US business activity growth slowed to a 16-month low in April, according to flash PMI® survey data, with business expectations about the year ahead also dropping to one of the lowest levels seen since the pandemic. Prices charged for goods and services meanwhile rose at the sharpest rate for just over a year, with an especially steep increase reported for manufactured goods, linked to tariffs."

And specific detail on prices:

- "Average prices charged for goods and services rose in April at the sharpest rate for 13 months, increasing especially steeply in manufacturing (where the rate of inflation hit a 29-month high) but also picking up further pace in services (where the rate of inflation struck a seven-month high).

- Higher charges were attributed to rising costs, linked widely in turn to tariffs, rising import prices, and increased labor costs.

- Input costs in the manufacturing sector rose at a pace not seen since August 2022, as suppliers pushed through price hikes linked to tariffs, supply concerns and a weakened exchange rate.

- Service sector costs meanwhile rose at a slower rate than in March, though the increase was the second largest recorded over the past six months as higher raw material prices were accompanied by upward wage pressures."