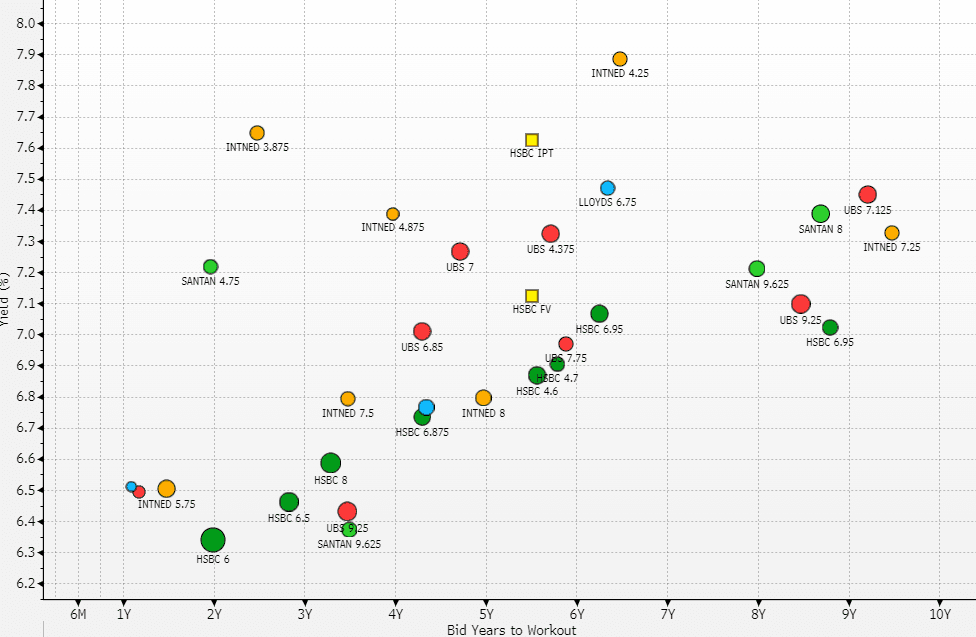

EU FINANCIALS: HSBC $ B'mark PerpNC5.5 AT1 - FV

May-29 09:38

- IPT:7.625 (c. 353bps float)

- FV: 7.125% (c303 bps float - which will make it the lowest HSBC AT1 float by 16bps)

- vs the HSBC 4.6% perp +0.25% yield for -63bps float spread - which is a middle of the range estimate. It might do reasonably well at 7.125, but might struggle an 1/8th lower.

- HSBC 4.6% Perp (365 bps float) 6.87%, 5.6y workout

- HSBC 4.7% Perp (325 bps float) 6.91%, 5.8y workout - which by the same logic as the new issue may screen expensive at basically the same yield and a 40bps float spread difference.

- Issuer Ratings: A3/A-/A+

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

SONIA: Call spread, spread

Apr-29 09:37

SFIZ5 96.80/97.10cs vs 2NZ5 96.90/97.20cs, bought the front for 0.25 in 9k.

FOREX: FX OPTION EXPIRY

Apr-29 09:36

Of note:

USDCAD 3.12bn at 1.3800/1.3835.

EURUSD 2.55bn at 1.1375/1.1395 (wed).

USDJPY 1.77bn at 142.00 (wed).

- EURUSD: 1.1325 (792mln), 1.1350 (282mln), 1.1440 (200mln).

- USDCAD: 1.3800 (489mln), 1.3805 (420mln), 1.3810 (770mln), 1.3820 (450mln), 1.3825 (667mln), 1.3835 (323mln).

- USDCNY: 7.3000 (674mln).

EGBS: Bund Futures Biased Slightly Higher But Key Resistance Remains Intact

Apr-29 09:31

Bund futures are +5 ticks at 131.32, with a downtick in oil prices and soft regional growth signals offset by a rise in spot/expected inflationary pressures. Kremlin suggestions that a 30-day truce with Ukraine is “impossible without solving all issues” provided only fleeting risk off flows into EGBs.

- Topside attention in Bund futures remains on 132.03, the Apr 7 high and bull trigger. Meanwhile the 20-day EMA at 130.70 provides support. German yields are 2-3bps lower across the curve.

- Spanish HICP inflation was 2.2% Y/Y (vs 2.0% cons, 2.2% prior), while 1/3-year ECB consumer inflation expectations also came in above consensus. However, this was offset by a weaker-than-expected Spanish Q1 GDP reading and a soft EC Economic Sentiment survey.

- Private sector lending growth continued its steady acceleration in March, rising two tenths to 2.6% Y/Y or three tenths to 2.0% Y/Y when adjusting for sales & securitisations (highest since Jun 2023).

- On the supply front, Finland and France are holding syndications while Italy has held a 5/10-year BTP and CCTeu auction.

- ECB’s Cipollone struck a characteristically dovish tone, warning of the downside growth risks related to US tariffs.

- 10-year EGB spreads to Bunds are within 0.5bps of yesterday’s closing levels. Following yesterday’s national outages, Spain and Portugal’s power systems are now back to normal.

- Tomorrow’s regional data calendar is equally heavy, with flash Q1 GDP and April inflation data due from Germany, France and Italy.