US DATA: Housing Activity Showing Increasing Signs Of Deterioration

Jun-18 13:06

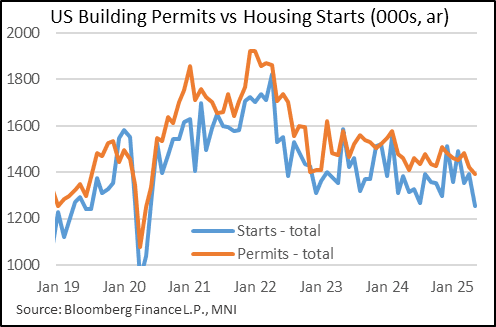

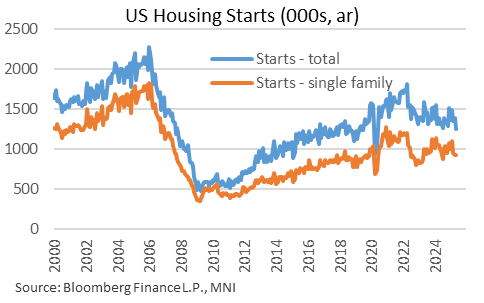

May's New Residential Construction report was very weak, portending very negative current conditions for residential investment activity, as well as a dim outlook for the quarters ahead.

- Housing starts fell to the lowest level since July 2019 (seasonally adjusted) excluding the sudden stop in 2020's pandemic, with a 9.8% M/M decline bringing the seasonally-adjusted annual rate of starts to 1,256k in May (vs 1,350k expected, 1,392k prior rev from 1,361k).

- Permits at 1,393k also disappointed vs expectations of a steady reading vs April at 1,422k and also hit the ex-pandemic lowest since July 2019.

- Weakness was seen across the board: single family permits fell 2.7% (4th fall in 5 months) to a 25-month low 898k, with multi-unit permits down 0.8% (7th fall in 9 months). Starts, which lag permits, saw single-family activity actually pick up slightly (0.4%, but only after falls in 3 of the prior 4 months) to 924k, but multi-units fall almost 30% to 332k.

- Starts are now down 4.6% Y/Y with permits down 1.0% Y/Y.

- New homes continue to sell, but combined with June's very poor NAHB survey - which tends to lead single-family starts/permits - the housing market is due to weaken significantly this year after 2024's residential investment bounce.

- The recent downward pressure in prices is set to accelerate too, albeit against the backdrop of very limited sales volumes as existing homeowners stay put (that said, inventories-to-sales have clearly picked up). New home sales are fairly robust though as we learned in the NAHB survey, that may be because discounting is picking up sharply.

- There is likely no relief in sight absent a pullback in mortgage rates, with homebuilders' responses to supply-side reform (eg regulation) probably paling in importance.

- Permits are a leading indicator for starts but there is a bit more of a gap than usual building between the two - we wonder if there is some combination of factors here restraining starts, including uncertainty over government policy, "surprisingly" elevated interest rates, and immigration policy shifts (which were noted in the Fed's latest Beige Book as a constraint on construction companies).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FRANCE T-BILL AUCTION RESULTS: 13/26/28/52-week BTFs

May-19 12:56

| Type | 13-week BTF | 26-week BTF | 28-week BTF | 52-week BTF |

| Maturity | Aug 20, 2025 | Nov 19, 2025 | Dec 3, 2025 | May 20, 2026 |

| Amount | E2.993bln | E1.898bln | E598mln | E2.098bln |

| Target | E2.6-3.0bln | E1.5-1.9bln | E0.2-0.6bln | E1.7-2.1bln |

| Previous | E2.993bln | E1.797bln | E1.797bln | E1.998bln |

| Avg yield | 2.042% | 2.011% | 2.004% | 1.947% |

| Previous | 2.057% | 2.023% | 2.023% | 1.985% |

| Bid-to-cover | 4.33x | 3.94x | 6.86x | 3.44x |

| Previous | 3.96x | 4.15x | 4.15x | 3.36x |

| Previous date | May 12, 2025 | May 12, 2025 | May 12, 2025 | May 12, 2025 |

US TSY FUTURES: TU/UXY Steepener blocked

May-19 12:51

Latest block trades lodged at 08:32:39 NY/13:32:39 London:

- TUM5 15.5K lots blocked at 103-08.25, looks like a buyer.

- UXYM5 6.7K lots blocked at 111-12+, looks like a seller.

- Would suggest a ~$570K Dv01 steepener, with subsequent price action on the 2s10as cash curve adding weight to that idea.

US TSYS: Goldman Marked End Of Year Yield Forecasts Higher Before Moody’s Action

May-19 12:38

Just ahead of Moody’s downgrade of the U.S. sovereign credit rating late on Friday Goldman Sachs revised their year-end 2-Year & 10-Year Tsy yield forecasts to 3.90% and 4.50%, respectively (from 3.30% and 4.00% previously).

- They reasoned that “the combination of a smaller mechanical tariff headwind and a meaningful reversal in financial conditions from the early-April peak has trimmed the downside risk around growth. With inflation still likely to reaccelerate meaningfully - albeit to a slightly lower peak than before - the baseline for further Fed cuts has shifted later and slower, with a quarterly cadence of cuts beginning in December reaching an unchanged terminal rate projection of 3.50-3.75% in June 2026”.

- For shorter maturity rates, Goldman think that “the absence of a clear growth catalyst may keep yields trade somewhat range-bound from here, but the vulnerability for now is closer to a carry drag than a clear case for substantial cheapening. The asymmetry is still to a sharp rally on bad news, with the market-implied probability of recession-type cuts having retreated significantly since the end of April”.

Trending Top

May-22 16:54