US DATA: Household Survey Continues To Show Slow, Not Major Deterioration (1/2)

The major indicators in the Household Survey portion of April's employment report contained mostly positive news versus expectations. The general trend remains of a slowly loosening labor market, but there were few signs of any major deterioration at the start of the second quarter. A few observations are below:

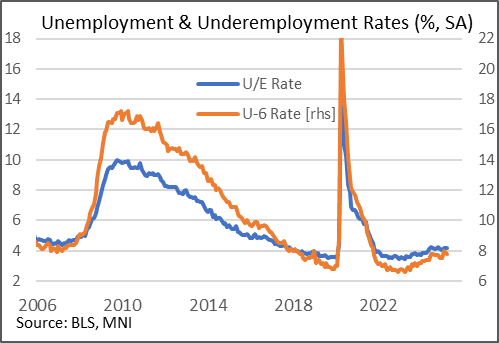

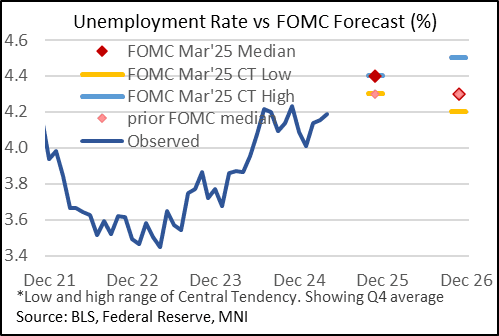

- Starting with the unemployment rate, which met consensus expectations by remaining steady at 4.2% rounded but ticking up slightly to 4.187% unrounded from 4.152% prior. This was the third unrounded increase, but those rises have been incremental and the rate remains within the range of the preceding 10 months. It keeps the rate below the FOMC's March end-year projection of 4.4%.

- Some of the calculations suggest this was a "healthy" rise in the unemployment rate. More specifically, there was an 82k rise in the number of unemployed persons (31k prior) but with the labor force rising by 518k (232k prior). The rise in the labor force was the biggest since August 2023 (excluding annual January benchmarking revisions).

- However, underlying the 82k rise in unemployed was a rise in job losers/those who completed temporary positions jumping by 140k - a 9-month high. 54k were on temporary layoff (9-month high, up from -6k prior), with those not temporarily laid off up 85k (up from 3k prior).

- Job leavers fell for a 3rd month in 4 (-15k), while defying the rise in the labor force was a 38k drop in new entrants (worst in 6 months, and vs +77k prior), however there were 60k re-entrants, reversing a 32k drop prior.

- The U-6 underemployment rate ticked lower for a second consecutive month, to 7.8% (7.9% prior), continuing to improve from 8.0% at February's 40-month high.

- Those not at work due to bad weather fell to a 58k from 87k (which had been lowest for a March since 2000), almost identical to the previous April's 55k. This had been an area of some interest after March's unusually low figure but this reading doesn't look out of the ordinary.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US: Senator McConnell To Vote Yes On Democratic Tariff Resolution - NBC

Senator Tim Kaine (D-VT) said that former Senate Republican Leader Mitch McConnell (R-KY) indicated that he will vote yes on a Democratic resolution that would "undo" President Donald Trump's tariffs on Canada by challenging the national security justification for their imposition, according to NBC News' Frank Thorpe on X. The resolution is seen as a message exercise as House Speaker Mike Johnson (R-LA) would kill the bill in the House, should it pass the Senate.

- For the resolution to pass, Democrats will need at least four Republican votes. Senator Rand Paul (R-KY) and moderate Senators Susan Collins (R-ME) and Thom Tillis (R-NC) have indicated they will vote yes.

- The vote, which will come later today after being punted from yesterday's schedule by Senator Corey Booker's (D-NJ) marathon speech, will put Republicans representing farm and manufacturing states in a challenging position, with polling suggesting that voters are sceptical of Trump's tariffs.

- Republican Senators may feel slightly more emboldened to oppose Trump's agenda after elections in Florida and Wisconsin yesterday provided warning signs that Independents and moderate Republicans are unconvinced by the early period of Trump's administration and the influence of advisor Elon Musk.

- Recognising that a significant Senate Republican rebellion could undermine his 'Liberation Day' announcement, Trump has issued two lengthy statements on Truth Social directly calling on Republicans to oppose the resolution.

TARIFFS: Deutsche Bank Expect Any Relief Rally Will be Short-Lived for Equities

- On today's market outcomes from the tariffs announcement, Deutsche Bank write that it is hard to see an outcome where we see material and sustained upside for equities.

- They write that even if tariffs are perceived to be on the lenient side, there remains a high degree of uncertainty over how various counties will respond and whether Trump will be more aggressive over time.

- Deutsche Bank see the broader USD reaction as likely to be led by equities and therefore see greater downside risks for the USD, led by the JPY and gold.

SWAPS: Long End ASWs Weaker Alongside Outright Bunds

Long end ASWs a little weaker on the day alongside the sell off in outright bonds detailed recently.

- Bund & Buxl ASWs have failed to push meaningfully above levels that prevailed ahead of the “whatever it takes” German fiscal moment, while Bund yields haven’t broken below the lows witnessed since the German fiscal loosening was table, pointing to new ranges being established as Germany moves to a new fiscal framework.