NATGAS: Henry Hub Easing Back on Week

Henry Hub front month is losing ground today and is softening around 6.5% on the week. Prices remain elevated, but indications of slightly milder-than-expected weather has added some pressure.

- US Natgas FEB 25 down 5.3% at 3.47$/mmbtu

- US Natgas MAR 25 down 3.8% at 3.02$/mmbtu

- The NOAA 6-14 forecast still shows below normal temperatures in the Midwest and East Coast, but above normal in the Mountain and Pacific regions. However, the colder weather is abating towards the end of that period.

- Lower 48 natural gas demand has risen to 104.1 bcf/d today, the highest since Dec. 22 according to Bloomberg. This compares to the weekly average of 90.8 bcf/d

- US LNG export terminal feedgas is strong at 14.71bcf/d today, a new record level according to BNEF data.

- US domestic natural gas production was estimated at 104.9 bcf/d yesterday, according to Bloomberg, down from the 7-day average of 106.0 bcf/d.

- Export flows to Mexico is 5.47cf/d today, according to Bloomberg.

- EIA weekly storage data is due today at 10:30 ET. Bloomberg predicts a draw of 126 bcf. The WSJ predicts a draw of 131 bcf while Reuters sees a smaller draw of 124 bcf.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FED: St Louis's Musalem Eyes Risks Of Easing Too Much Too Soon

St Louis Fed Pres Musalem's comments (speech link) are a little more hawkish than those made recently by some of his FOMC colleagues (note he is a 2025 voter), though perhaps not quite as much as the initial Bloomberg headlines suggested and not surprisingly so given his historically hawkish leanings. His comments about risks of disinflation stalling, and potentially slowing/pausing cuts, were notably not part of his core scenario - and he says he is retaining "optionality" about the December FOMC meeting decision. However he does seem to see the balance of risks as tilted toward inflation remaining stubborn, entailing slower cuts.

- On a pause/slowing of cuts: "Based on what we know today, further easing toward a neutral policy stance will likely be appropriate over time... the path toward a neutral policy stance could be accelerated, slowed or paused depending on how the economic environment and outlook evolve... it seems important to maintain policy optionality, and the time may be approaching to consider slowing the pace of interest rate reductions, or pausing... while it is not in my baseline scenario, information received since September suggests a higher risk that progress toward 2% inflation could stall, or possibly reverse... In the current environment, easing policy too much too soon poses a greater risk than easing too little, or too slowly."

- Asked in the Q&A about potential for a pause, Musalem says "I said at future meetings... might be December, might be January, might be later...for December, I'm keeping all options open" on the rate decision, waiting to see upcoming data.

- The 75bp in cuts so far "lessened but did not eliminate monetary restraint. The policy rate remains above plausible levels for the neutral policy rate, appropriately so with inflation above target and a labor market close to full employment"

- That said, on neutral rates, "monetary policy rules suggest a federal funds rate between 4.3% and 5.4% for the fourth quarter of 2024. At 4.6%, the midpoint of the current federal funds target range is already well within the range suggested by policy rules, and below the median of this range. Further reductions in the federal funds rate will therefore require careful management and depend crucially on an expectation of further convergence toward 2% inflation."

- His outlook for the economy is pretty consistent with other FOMC members: "Progress [in inflation] should become more evenly balanced, shifting from a reliance on falling goods and energy prices and toward lower housing and services inflation. I expect economic activity will moderate toward its long-term potential in level and growth terms. Some further gradual labor market cooling is likely, accompanied by moderating compensation growth."

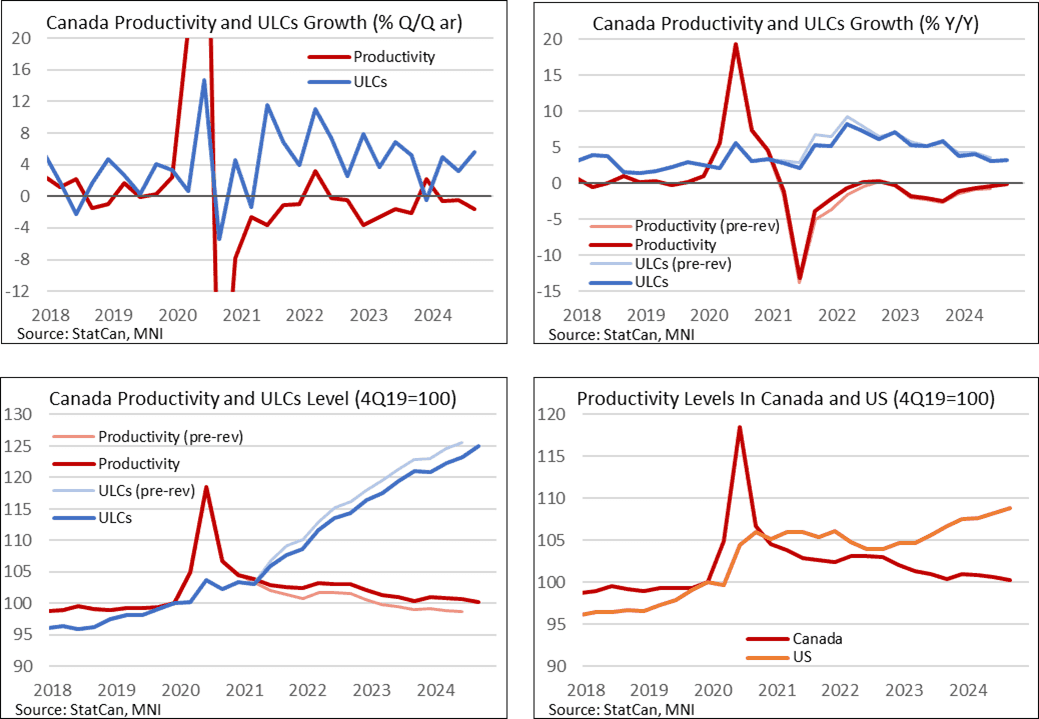

CANADA DATA: Productivity Data Sees Large, But Backdated, Dovish Revisions

- As our policy team notes, labor productivity fell -0.39% Q/Q (cons -0.3) in Q3 after -0.13% Q/Q (initial -0.17) in Q2, or -1.6% annualized after -0.5%.

- There were some large revisions, with dovish implications, but they were backloaded with far more modest recent changes.

- For example, the level of labor productivity was revised up 1.9% in Q2 but the Y/Y rate was only revised up from -0.7% to -0.3%, whereas the unit labor cost level was revised down -1.8% but the Y/Y rate was only revised down from 3.5% to 3.2%.

- The recent trend is broadly similar to what was previously known, with productivity declining in nine of the past ten quarters. However, a strong 0.5% increase back in 4Q23 helped see Y/Y growth of just -0.1% Y/Y in Q3 for its least negative since 3Q22. Unit labor costs meanwhile increased 3.3% Y/Y in Q3.

- The productivity trend continues to stand in stark contrast to the US where productivity growth stood at 2.0% Y/Y in Q3, its softest since 2Q23.

STIR: Effective Fed Funds Rate

- STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.58% (+0.00), volume: $94B

- Daily Overnight Bank Funding Rate: 4.58% (+0.00), volume: $248

- Earlier Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.64% (+0.00), volume: $2.329T

- Broad General Collateral Rate (BGCR): 4.60% (+0.00), volume: $832B

- Tri-Party General Collateral Rate (TGCR): 4.60% (+0.00), volume: $798B

- (rate, volume levels reflect prior session)