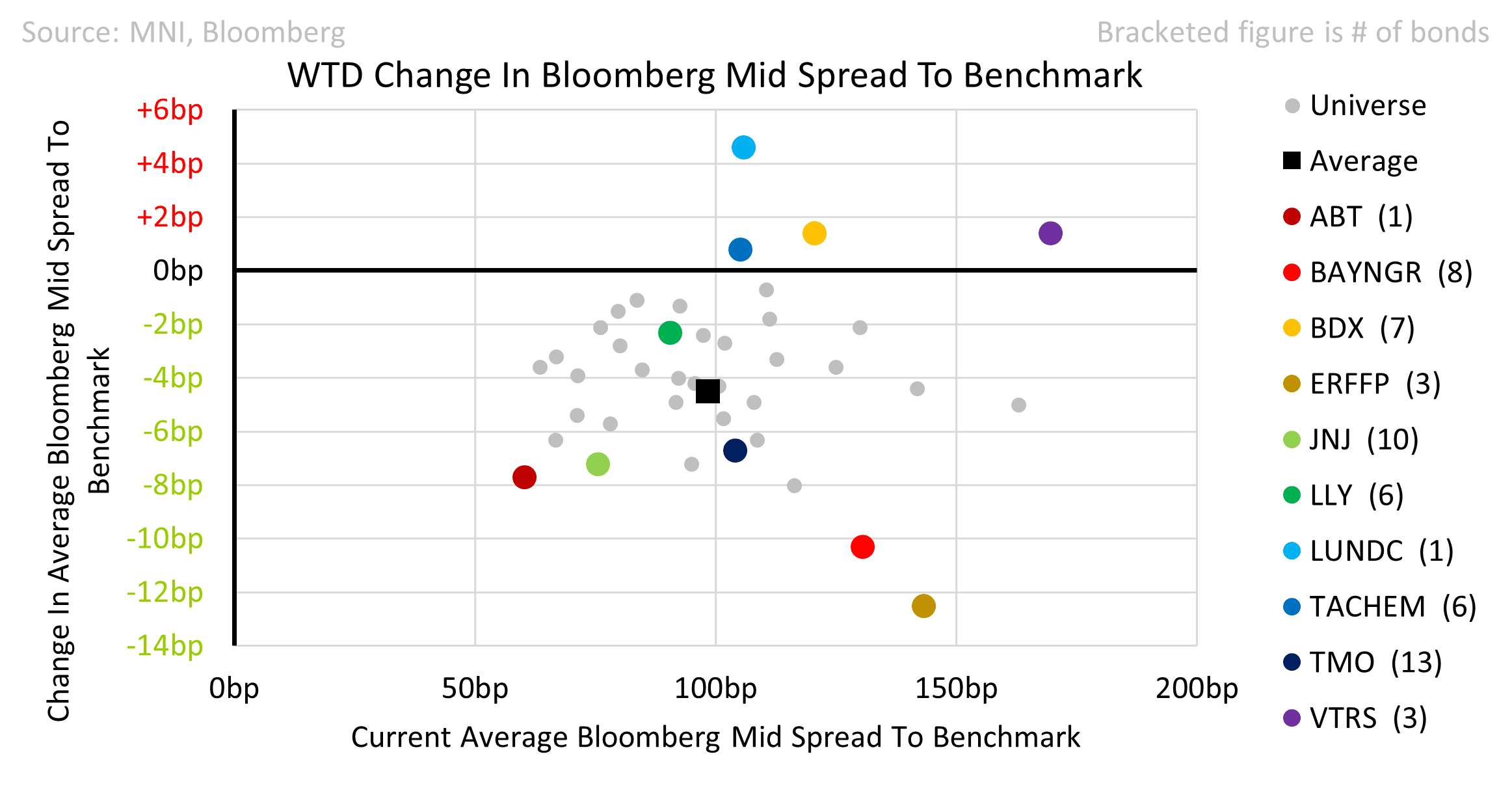

EU HEALTHCARE: Healthcare: Week in Review

A strong week with spreads 4.5bps tighter led by Eurofins and Bayer. These moves reflect beta rather than anything company specific. Viatris, however, did not benefit from the risk-on move as it is placing equity ahead of credit to placate shareholders.

• US Pharma Policy: Politico carried a piece which stated that Trump would use executive orders to enforce “most favoured nation” status for US Pharma imports to cut the price paid by Medicare for leading drugs. At the FDA, Vinay Prasad was appointed director of the Center for Biologics Evaluation and Research. As a leading opponent of Biden’s vaccination policy this could be negative for AZN, Sanofi, GSK and Pfizer.

• Sanofi was upgraded to Aa3 by Moody’s

• Earnings: Zimmer Biomet (Small Negative) tariffs to have larger impact in 2026, equity fell 12% but recovered half ; Philips (Small Negative) cut margin guidance and Respironics payouts consumed free cash; Fresenius Medical (Small Positive); Coloplast (Neutral) reduced guidance but is also cutting leverage; Novo Nordisk (Neutral) reduced guidance but from very high levels; Fresenius SE (Neutral); Takeda (Small Positive) reduced leverage, has limited tariff exposure and is replacing Vyanse with new products; Viatris (Negative) prioritising shareholders over creditors; Lonza (Small Positive) confirms +20% sales growth and 30% margin targets, limited tariff exposure.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

OPTIONS: Expiries for Apr10 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0900-10(E3.0bln), $1.0930-50(E3.0bln), $1.0960-65(E668mln)

- USD/JPY: Y143.00($1.3bln), Y145.00($744mln)

- EUR/GBP: Gbp0.8650-65(E643mln)

- AUD/USD: $0.6165(A$744mln), $0.6285($555mln), $0.6400(A$1.3bln)

- NZD/USD: $0.5600-05(N$724mln)

- USD/CAD: C$1.4395-00($1.5bln)

- USD/CNY: Cny7.3500($912mln), Cny7.4000($1.4bln)

GILTS: TD Securities Recommend Longs In 30s

TD Securities recommended longs in 30-Year gilts at 5.62%, targeting a move to 5.10%, with a stop set at 5.90%.

- They note that “rates vol. is heading to unhealthy levels, straining financial conditions. The BoE has already voiced its concern on this move. Markets should not underestimate a possible easing in the form of regulations or verbal easing or even a temporary QT freeze on this move. On every metric, 30-year Gilts are cheap: vs. U.S. Tsys & Bunds, as well as ASW and on the 5s30s curve”.

GERMANY: New Coalition Plans Making Use Of Increased Fiscal Space - Agreement

Key fiscal/economic measures announced by the incoming CDU/CSU/SPD coalition below. These broadly match the announcements seen in local media earlier today. Note that in Germany, an announcement of measures as part of a coalition agreement does not necessarily mean these will be implemented. Overall, the government seems to be planning to make use of the newly increased fiscal headroom:

- Reducing income taxes for small and medium incomes in the middle of the legislative period

- Investment "booster" in the form of amortization of equipment investment of 30% per year for the three years 2025-27

- After this has ended, decreasing the corporation tax in 5 steps by 1pp each starting January 2028 (currently standing at 15% of ~EBT but note that is not the only tax enterprises have to pay in Germany)

- Reduction of electricity taxes to the European minimum, reduce electricity network charges, abolish gas price levy, introduce a "industrial electricity price" for energy-intensive companies

- Make overtime bonuses tax-free, up to E2000/month tax-free labour work during pension, replace the "citizens income" by a "basic income" (compulsory job applications for unemployed persons and tougher sanctions)

- VAT decrease for food in restaurants by 12pp to 7% starting Jan 2026

- Increase of the minimum wage to E15/hour in 2026 (17% increase, agreement rather vague here though)

- Monetary incentives for EV purchases

- Plans to complete debt brake reform this year to "permanently enable additional investment"

Full coalition agreement pdf document available online, link here.