EM ASIA CREDIT: Hanwha Energy USA: New $ mandate FV

(HWEUHC, Aa2/AA/-)

Mandate: $ 3y

FV: z+95bp

Hanwha Energy Corp. subsidiary, Hanwha Energy USA, has mandated banks for a new 3y $ bond, with investor calls this week and a possible launch date on Monday 23rd June. The bond will be guaranteed by The Export-Import Bank of Korea. The existing $300m bond matures in July. Hanwha Energy is a retail energy producer, its US subsidiary is focused on solar power.

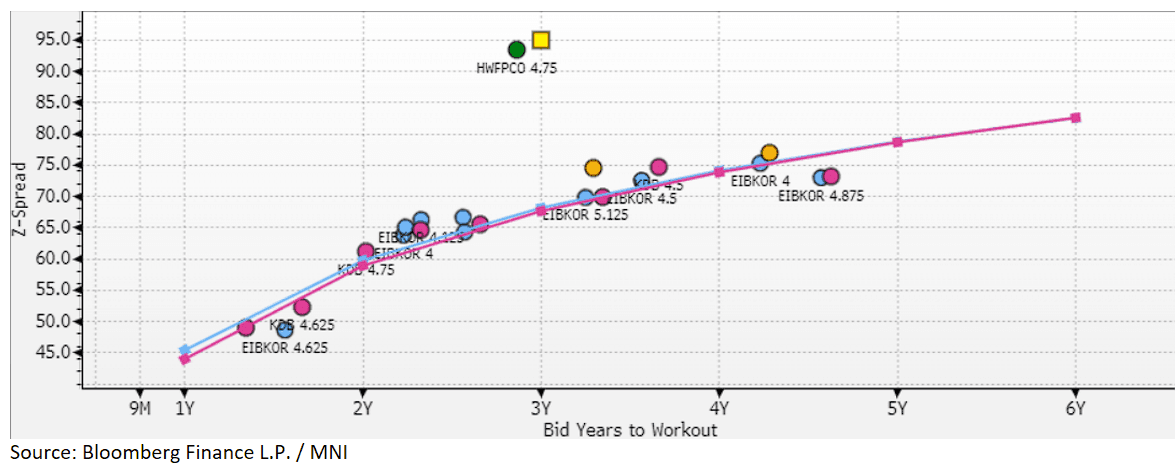

In terms fair value, we map the $ curves of the Export-Import Bank of Korea, Korea Development Bank as well as the Industrial Bank of Korea, all of which are rated the same as the Korean sovereign (Aa2/AA/AA-). The issuers, as you might expect, are trading more or less on top of each other. We also add Hanwha FutureProof (HWFPCO, Aa2/AA/-), which is part of the Hanwha group, as well as being guaranteed by the Korea Development Bank.

Hanwha FutureProof is a JV investment company owned equally between Hanwha Solutions and Hanwha Aerospace, headquartered in the U.S. The investment focus is energy sustainability, though we note the recent approval by Australian authorities to increase its stake in Australian defence company, Austal Ships.

We think Hanwha FutureProof acts as a natural anchor to a fair value estimate of Hanwha Energy's proposed 3y deal, given recent issuance, similarly guaranteed by the Korean State and being part of the Hanwha Group. We see fair value at the 3yr at z+95bp.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JGBS: Very Poor Demand Metrics For 20Y Auction, Tail Longest Since 1987

The 20-year JGB auction delivered very poor results across key metrics. The low price underperformed dealer forecasts, which were set at 99.80 according to a Bloomberg poll. Moreover, the cover ratio decreased to 2.5007x from 2.9639x in the previous auction, and the auction tail lengthened dramatically from 0.34 to 1.14 – the longest since 1987.

- As noted in the auction preview, today’s offering featured an outright yield near its cycle high, approximately 5bps above last month’s level.

- Moreover, the 10/20 yield curve remained near its recent high, its steepest since 1999.

- As a consequence, this result is likely to be seen as significantly worse than the performance observed in the 30-year JGB auction earlier this month.

- Post-auction, the 20-year JGB has cheapened 6bps.

JGBS AUCTION: 20-Year JGB Auction Results

The Japanese Ministry of Finance (MOF) sells Y750.9bn 20-Year JGBs:

- Average Yield: 2.453% (prev. 2.349%)

- Average Price: 99.29 (prev. 100.69)

- High Yield: 2.540% (prev. 2.374%)

- Low price: 98.15 (prev. 100.35)

- % Allotted At High Yield: 80.8791% (prev. 40.8163%)

- Bid/Cover: 2.5007x (prev. 2.9639x)

STIR: RBA Dated OIS Pricing Softer Ahead Of Today’s RBA Policy Decision

RBA-dated OIS pricing is flat to slightly softer across meetings today, with July/August leading, ahead of tomorrow’s RBA Policy Decision.

- A 25bp rate cut in May is given a 97% probability, with a cumulative 77bps of easing priced by year-end.

- Notably, today’s moves leave meetings pricing 3-42bps firmer than levels before the release of Q1 CPI data on April 30.

Figure 1: RBA-Dated OIS – Current Vs. Pre-Q1 CPI

Source: MNI - Market News / Bloomberg