EM LATAM CREDIT: Hammack: Don't See Case For September Cut With Current Data

From MNI US FI Markets Economist:

Cleveland Fed President Hammack (non-2025 FOMC voter but votes in 2026; hawk) echoes earlier commentary today from the sidelines of Jackson Hole from KC's Schmid (a fellow hawk) in casting doubt on the necessity of a September rate cut. Going into Jackson Hole, we thought she was one of 10 (of 18) FOMC members that sounded open-minded enough in previous commentary to be persuadable on a September cut - but now the balance on the Committee clearly tips to 4 in favor/9 undecided/5 opposed.

- Hammack says: "I think that there's a lot of data we're going to get between now and September. And I walk into every meeting with an open mind about what the right thing to do is. But with the data I have right now, and with the information I have, if the meeting was tomorrow, I would not see a case for reducing interest rates."

- In short, Hammack sees inflation risks exceeding those of missing on the employment side of the mandate: "my biggest concern is that inflation has been too high for the past four years, and right now it's been trending in the wrong direction and so I think it's really important that we stay modestly restrictive to make sure that we can bring inflation back under control... When I take the balance of things, there's a lot to be focused on the labor side, but the inflation side is is right now giving us a place where we're not at our target. We're at our target on the employment side. We're worried that maybe possibly that could break down, but we know we're missing on the inflation side, and to me, we need to stay laser focused on that to make sure we can bring inflation down."

- On neutral rates: "I don't think we're very far. I don't disclose my dot, but I think we're right around."

- Asked how she would regards another weak jobs report (with negative revisions), Hammack repeats arguments heard from others on the FOMC that overall payrolls growth may not be the best indicator of a weakening labor market, given a reduction in immigration (ie labor supply): "with the changes that have happened in immigration policy, it's not clear that that headline growth number is going to be as informative as things like the unemployment rate, the vacancies to unemployed ratio, other things that we're looking at on the employment side of the mandate, and that's because we've seen a massive shift ... so yes labor demand may be coming down but labor supply has come down pretty dramatically as well. And so our goal of maintaining employment around maximum needs to look at both sides of that, and it could be that even though we're seeing much slower headline job growth numbers, it could be that the labor market is still in balance and so we'll need to look at that closely."

- She says that the inflationary impact of tariffs is yet to really bite. Re PPI, "wholesale prices were going up more significantly, but not necessarily being passed on to consumers. That tracks with what I'm hearing when I'm out traveling in the district and I'm hearing from manufacturers that they're trying to buffer these price pressures as much as they can, but that's not going to last forever, and so some of these price pressures that are coming into the PPI and coming into the wholesale space will eventually make their way into the consumer space".

- That means it could be several months before the Fed can get a read on the inflationary impact of tariffs: "It's just now I think that we're starting to see some of those impacts play through into the economy. It usually takes three to four months for to start seeing the early impacts of tariffs, and so we're just at that point right now, just past that three to four month mark. I do expect from the conversations I've had that we're not going to see the full impact of tariff pass through until sometime next year...it could be that we're still continuing to see some of these impacts in Q1 and Q2 in terms of whether tariffs are going to be a one time price level impact or more persistently inflationary."

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FED: Trump - Powell Doing A Bad Job But He's Out Soon Anyway

- Reporter: Do you think that Fed Chair Powell should resign?

- Trump: I think he’s done a bad job but he’s got to be out pretty soon anyway. In 8 months he’ll be out.

[That’s close to the May 2026 end for Powell’s Fed Chair term].

Trump follows with familiar comments, including later on that he wants rates at 1%: “He should have lowered interest rates many times. Europe lowered their rate ten times. We lowered ours none. It’s causing a problem for people wanting to buy a home. Look, our economy is so strong now, We’re blowing through everything. We’re setting records, you know that we see that.”

Trump then reverts to Fed renovation cost rhetoric.

FOREX: USDCAD Extends Lower as BOC/Fed Meetings Awaited Next Week

- Alongside the extension of dollar weakness on Tuesday, a strong performance for the Canadian dollar has prompted USDCAD (-0.40%) to trade to fresh two-week lows. The pair flirted above the key 50-day EMA last week, however, the swift reversal and subsequent resumption of weakness keeps a bearish trend intact. Downside momentum appears to have picked up below some daily lows around 1.3650 today.

- Further declines would refocus attention on key support at 1.3540, the Jun 16 low. Clearance of this level would confirm a resumption of the technical downtrend.

- PM Mark Carney kicked off his meeting with Canada's premiers in Huntsville, Ont., on Tuesday promising to battle the Trump administration at the negotiating table to ensure the country gets a good trade deal, while also doing everything he can to strengthen the Canadian economy.

- Consensus looks for the Bank of Canada to remain on hold next week (July 30 decision same day as the Fed). BBVA point out that market pricing for BoC policy reflects a highly prudent stance, which is supportive of the CAD. However, they believe ongoing uncertainty and the threat of potential higher US tariffs will likely temper upward movements in Canada's economy and the CAD until greater clarity emerges after Aug 01.

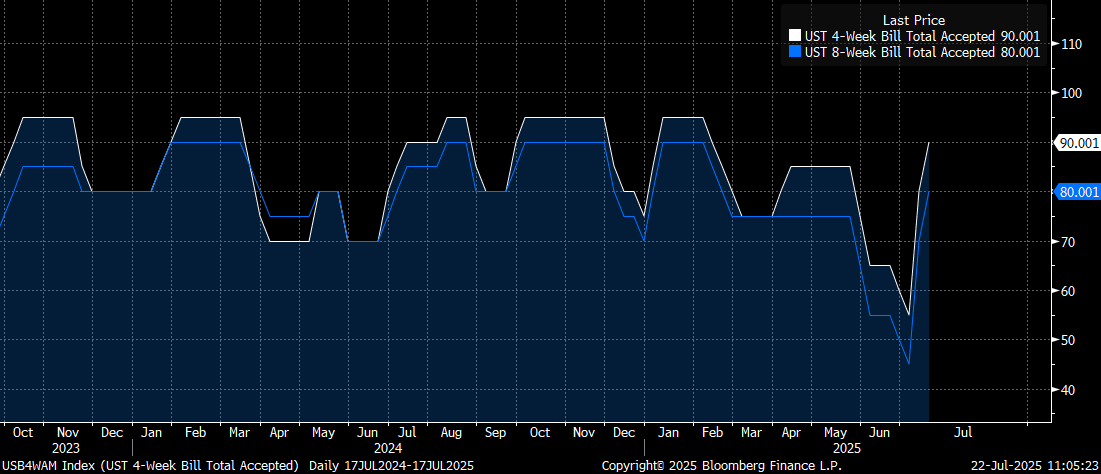

US TSYS/SUPPLY: Treasury Ups Bill Sizes Again As Cash Rebuild Picks Up Pace

Treasury continued to up the size of 4- and 8-week bills, rising $5B apiece for Thursday's auctions to $95B and $85B, respectively. The new 4-week level will match the all-time largest auctions seen over the last couple of years, with 8-weeks remaining below the $90B peak.

- This is the 3rd consecutive weekly increase - they're up from $55B/$45B at the beginning of the month, prior to the lifting of the debt limit. 17-week auction sizes were unchanged at $65B.

- The increase is something of a surprise (Wrightson ICAP this morning wrote "We think the Treasury has completed its current ramp-up of bill offering sizes"), in a possible sign that Treasury is not necessarily going to back-load its rebuild of the Treasury General Account post-debt limit: it said after the debt limit was lifted that it is aiming for a cash balance of $500B by end-July (vs $315B at end-last week) and $850B by end-September.

- Upon settlement next Tuesday, the bills will raise $60B in net cash.

- We expect to hear a little more about cash management plans in next week's Refunding round. For the foreseeable future, bills are going to be the moving part in meeting financing requirements, with coupon auction sizes not expected to be increased for several quarters at least. We'll publish our Refunding preview later this week.