BRENT TECHS: (H6) Trend Needle Points South

- RES 4: $70.06 - High Jul 30

- RES 3: $68.58 - High Sep 26

- RES 2: $64.81 - High Oct 24 and a key resistance

- RES 1: $61.99 - 50-day EMA

- PRICE: $59.93 @ 07:03 GMT Jan 7

- SUP 1: $58.53 - Low Dec 16

- SUP 2: $58.27 - Low Apr 9 and a key support

- SUP 3: $57.87 - 1.764 proj of the Jul 30 - Aug 13 - Sep 26 price swing

- SUP 4: $56.44 - 2.000 proj of the Jul 30 - Aug 13 - Sep 26 price swing

The trend outlook in Brent futures remains bearish and recent gains are considered corrective. Note that moving average studies are in a bear-mode condition, highlighting a dominant downtrend. A resumption of the bear cycle would open $58.27, the Apr 9 low. On the upside, key short-term resistance to watch is $64.81, the Oct 24 high. First resistance is $61.99, the 50-day EMA.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

USDJPY TECHS: Corrective Phase Exposes The 50-Day EMA

- RES 4: 158.87 High Jan 10 and a key resistance

- RES 3: 158.29 2.618 projection of the Sep 17 - 26 - Oct 1 price swing

- RES 2: 158.00 Round number resistance

- RES 1: 156.58/157.89 High Nov 28 / 20 and the bull trigger

- PRICE: 155.19 @ 07:12 GMT Dec 8

- SUP 1: 154.35 Low Dec 5

- SUP 2: 153.41 50-day EMA

- SUP 3: 152.82 Low Nov 7

- SUP 4: 151.54 Low Oct 29

Recent weakness in USDJPY is considered corrective. The deeper retracement has allowed an overbought condition to unwind. An extension lower would expose the 50-day EMA at 153.49 and the next important support. Moving average studies remain in a bull-mode position, highlighting a dominant medium-term uptrend. A resumption of the trend would open 158.00.

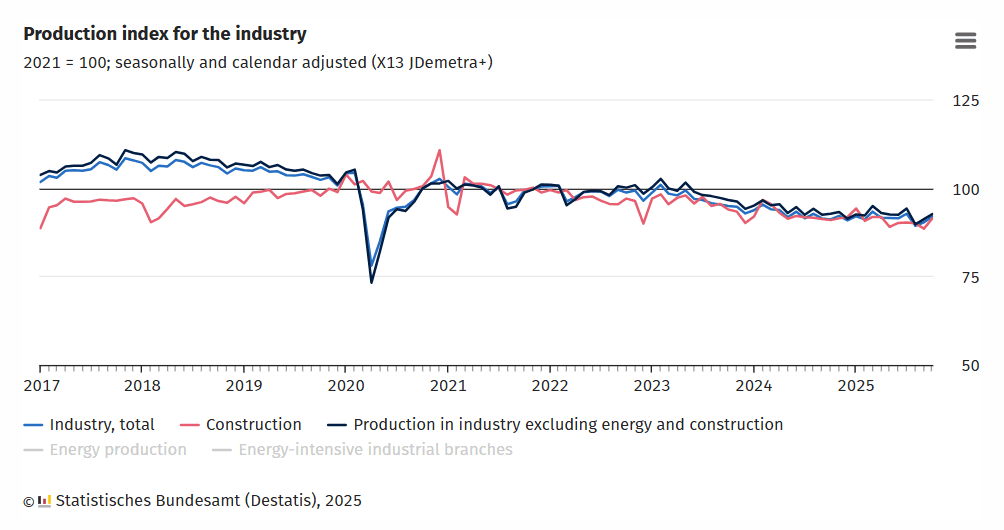

GERMAN DATA: IP Starts Off Q4 On Comparably Strong Note

- German industrial production was stronger than expected in October, even considering the downward September revision.

- "The less volatile three-month on three-month comparison showed that production was 1.5% lower in the period from August 2025 to October 2025 than in the previous three months [...] In October 2025, production in industry excluding energy and construction was up 1.5% [M/M] from September 2025 after seasonal and calendar adjustment."Destatis comments.

- On drivers within manufacturing (excl. energy and constr): "increases registered in the manufacture of machinery and equipment (+2.8%) and in the manufacture of computer, electronic and optical products (+3.9%) also made a significant contribution to the overall result. By contrast, the decline in production in the automotive industry (-1.3%), which is an important sector, had a negative impact"

- An increase in construction (+3.3% M/M) follows strong increases in dwelling approvals over the last couple of months in Germany which may be starting to filter through.

- Sentiment in German industry has faded most recently, with both the Manufacturing PMI and IFO index slightly lower in their December readings than in November. The IFO saw some reduction the difference between its expectations and current conditions subreadings - the spread between these remains notable, though.

EUROZONE ISSUANCE: EGB Supply: W/C 8 December and 2026 Funding Plans

Austria and Italy will look to hold conventional auctions this week. We pencil in issuance of E5.6bln for the week, down from E17.8bln last week. We expect Ireland, the Netherlands (Friday) and potentially Portugal to release 2026 funding plans. There may also be an update to the Slovak 2026 funding plan either this week or next. For details of funding plans released so far see pages 2-3 of the PDF

For the full MNI EGB Issuance, Redemption and Cash Flow Matrix with a look ahead to the remaining year's issuance and summaries of 2026 funding plans, click here..

- Austria will kick off issuance for the week tomorrow, with E575mln of the 2.80% Sep-32 RAGB (ISIN: AT0000A3NY15) on offer.

- Italy will come to the market on Thursday to hold a 3/5 year BTP auction (with no 7/15+ year BTP on offer) in the final Italian auction of 2025. On offer will be E2.5-3.0bln of the on-the-run 3-year 2.35% Jan-29 BTP (ISIN: IT0005660052) alongside E0.75-1.0bln of the 3.00% Oct-29 BTP (ISIN: IT0005611055) and E0.75-1.0bln of the 2.70% Oct-30 BTP (ISIN: IT0005654642). With the exception of the 3-year, the other two BTPs on offer are off-the-run.

- As we had expected, the MEF has cancelled the bond auctions scheduled for 29/30 December as well as the BOT auction scheduled for 29 December.

NOMINAL FLOWS: This week will see a redemption of E19.0bln from a German Schatz. Coupon payments for the week total E2.2bln of which E1.1bln are from the EU and E1.0bln German. This leaves estimated net flows for the week at negative E15.6bln, versus negative E15.1bln last week.