BRENT TECHS: (H6) Trades Through The 50-Day EMA

- RES 4: $70.06 - High Jul 30

- RES 3: $68.58 - High Sep 26

- RES 2: $64.81 - High Oct 24 and a key resistance

- RES 1: $63.02 - High Jan 8

- PRICE: $62.76 @ 07:08 GMT Jan 9

- SUP 1: $58.53 - Low Dec 16

- SUP 2: $58.27 - Low Apr 9 and a key support

- SUP 3: $57.87 - 1.764 proj of the Jul 30 - Aug 13 - Sep 26 price swing

- SUP 4: $56.44 - 2.000 proj of the Jul 30 - Aug 13 - Sep 26 price swing

A recovery in Brent futures yesterday has resulted in a break of resistance around the 50-day EMA, at $61.92. The break highlights a short-term improvement in the current bull theme and signals scope for an extension of the corrective cycle. The trend condition remains bearish and a reversal lower would $58.27, the Apr 9 low. Key resistance to watch is $64.81, the Oct 24 high. A breach of this hurdle would highlight a stronger reversal.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BRENT TECHS: (G6) Bear Threat Still Present

- RES 4: $70.86 - 76.4% retracement of the Jun 23 - Oct 17 bear leg

- RES 3: $70.33 - High Jul 30

- RES 2: $68.86 - High Sep 26 and a key resistance

- RES 1: $65.25 - High Oct 24

- PRICE: $62.10 @ 07:06 GMT Dec 10

- SUP 1: $59.93 - Low Nov 20 and the bear trigger

- SUP 2: $58.92 - Low May 5

- SUP 3: $58.11 - Low Apr 9 and a key support

- SUP 4: $56.22 - 2.00 proj of the Jul 30 - Aug 13 - Sep 26 price swing

A bear threat in Brent futures remains present - the move down since Oct 24 highlights a bearish theme. A stronger resumption of weakness would expose key support and the bear trigger at $59.93, the Oct 20 low. Clearance of this level would confirm a continuation of the bear cycle. Key short-term resistance to watch has been defined at $65.25, the Oct 24 high. A breach of this level would instead signal scope for a stronger correction.

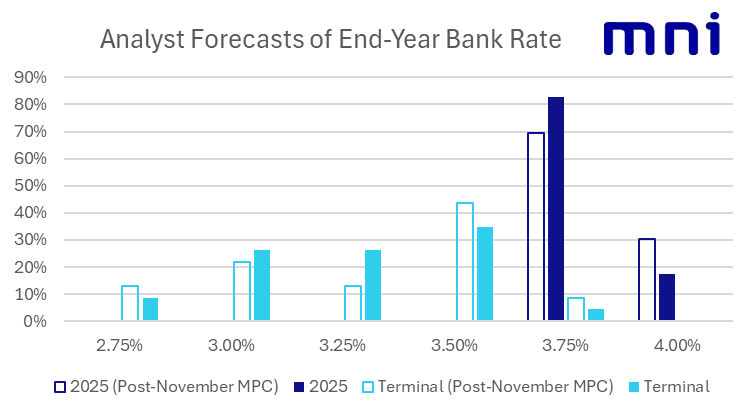

BOE: VIEW CHANGE: MS raises terminal rate expectation to 3.00%

- Morgan Stanley has raised its BOE terminal rate forecast to 3.00% from 2.75% "as the balance of risks around our 2026 forecasts shifts slightly."

- MS "still expect the BoE to cut in December and February, but now see a skip in March, followed by further action in April and June, as inflation data continue to evolve favourably."

- This is below market pricing (which prices in around 56 bp of cuts from the current 4.00% rate) but it is not hugely inconsistent with other sell side views (14/23 of the analysts we track look for a 3.25% rate or lower with 8/23 looking for 3.00% or lower).

SCANDIS: NOKSEK Holds Above Support Following Early Scandi Data

Little net reaction in NOKSEK to this morning’s Scandi data. The cross remains at ~0.9230, above support at the 0.9200 figure. Yesterday’s impressive SEK strength saw the cross breakdown notably, reinforcing our view that risks are still skewed to the downside.

- Norway November CPI-ATE inflation was a tenth below Norges Bank and analyst consensus at 3.1% Y/Y (vs 3.4% prior), but still within the 3.0-3.2% Y/Y range of estimates we had seen. Overall, this should make for a broadly neutral impact from spot inflation on the “prices and wages” component of the December MPR relative to September. Will follow up with details in due course.

- The prices and wages rate path component may be impacted to a greater extent by tomorrow’s Q4 Regional Network Survey, which includes wage expectations and capacity utilization estimates.

- Swedish October GDP was -0.3% M/M (vs -0.1% prior). The four analyst estimates submitted to Bloomberg ranged from -0.8% to 0.4%. Both household consumption and private sector production fell on the month, but we don’t take much signal from one set of (volatile, revision prone) monthly data. Other economic activity signals have been improving in recent months.