AUSSIE 3-YEAR TECHS: (H6) S/T Net Higher After CPI Vol

* RES 3: 97.796 - 1.618 proj of the Sep 3 - 12 - 15 price swing * RES 2: 96.780 - High Jun 26 (cont)...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

PRECIOUS METALS: : Geopolitical Events Could Drive Higher Safe Haven Flows

Gold and silver were higher on Friday but finished the week down following Monday’s correction. The US ousting of Venezuelan dictator Maduro on the weekend is likely to add to geopolitical uncertainty as it is unclear if the US will intervene in other countries, especially in South America, and what the outcome of current unrest in Iran could be. This may drive higher safe haven flows which could boost precious metal prices.

- US Secretary of State Rubio has said that it will take time for democracy to return as most of the opposition lives outside of Venezuela. The US doesn’t have forces on the ground and the country is currently being run by Maduro’s ally Rodriguez who Trump has warned to cooperate.

- Gold prices rose 0.3% to $4332.29/oz on Friday but were down 4.4% on the week. They reached a high of $4402.30 before trending down to $4310.06 pressured by a strengthening of the US dollar (BBDXY +0.1%). They continue to trade above the 20-day EMA at $4259.9.

- Silver reached $74.553 before falling to around $71.50. It finished up 1.6% to $72.772 but was still 8.2% lower last week after a 10% rally on 26 December. The market is significantly smaller than for gold and the holiday-related lighter trading volumes caused volatility.

- Equities were stronger with the S&P up 0.2% and Euro stoxx +1.0%. Oil was little changed with Brent down 0.1% to $60.80. Copper rose 0.3%.

BONDS: NZGBS: Cheaper As Market Returns From Extended NY Holiday

NZGBs are ~3bps cheaper across benchmarks after an extended New Year’s holiday break.

- On Friday, after US tsys finished Friday with a modest bear-steepener.

- There was limited data on Friday: The final December S&P Global Manufacturing PMI was unchanged from the flash reading of 51.8, confirming a 5-month low for the index (52.2 Nov). In turn, the details of the report confirmed the flash data in portraying a broad-based softening amid overall growth in manufacturing.

- Focus in the first two full weeks of the year will be on nonfarm payrolls (Friday) and CPI reports (Jan 13) for December, with those two key reports back on their original schedules having been prioritized by the BLS. Private sector reports meanwhile are highlighted by ISM manufacturing and services reports Jan 5 and 7. No scheduled Fed speakers today.

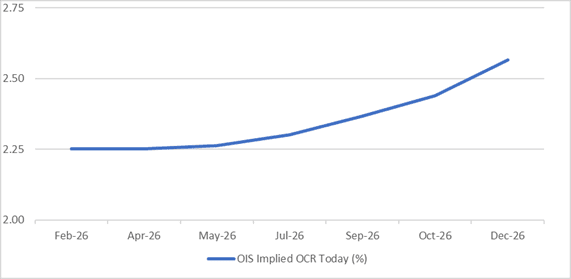

- RBNZ-dated OIS pricing is showing no tightening priced for February, while October 2026 assigns 19bps (see chart).

- The local data calendar is very light this week, with just Dec Cotality home value figures out later this evening. Next week we get Nov filled jobs, along with food prices as well.

Bloomberg Finance LP / MNI

AUD: A$ Up From Earlier Lows, Positive Technical Backdrop Holds, CPI Wed

AUD/USD tracks near 0.6685/90 in latest dealings, down around 0.10% versus end Friday levels, as modest risk off grips markets to start the week (earlier lows were at 0.6676). This follows the US capture and extradition of Venezuelan leader Maduro. Focus will be on broader risk trends, particularly in terms of oil and US equity futures. For oil, any market expectations around increased Venezuelan supply may take time to realize. The A$ could also see some offset from higher precious metal prices if risk off losses gain traction in the equity space.

- At this stage, the broader technical backdrop for AUD/USD is unchanged, which is still constructive. The pair remains above all key EMAs. The 20-day EMA is near by, close to 0.6660, while the 50-day is around 0.6610. On the topside, we can't hold moves above 0.6700 at this stage, with late 2025 highs at 0.6729, remaining intact.

- Broader risk/commodity price moves are likely to dictate sentiment today. The local data calendar swings back into gear tomorrow, with Dec final PMI reads for the S&P Global services and composite indices.

- Greater focus will rest on Wednesday's Nov CPI print though. Headline is forecast at 3.6%y/y (versus 3.8% prior), while the trimmed mean is seen unchanged at 3.3%y/y, per the market consensus.