AUSSIE 3-YEAR TECHS: (H6) Recovery Mode

* RES 3: 97.796 - 1.618 proj of the Sep 3 - 12 - 15 price swing * RES 2: 96.780 - High Jun 26 (cont)...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

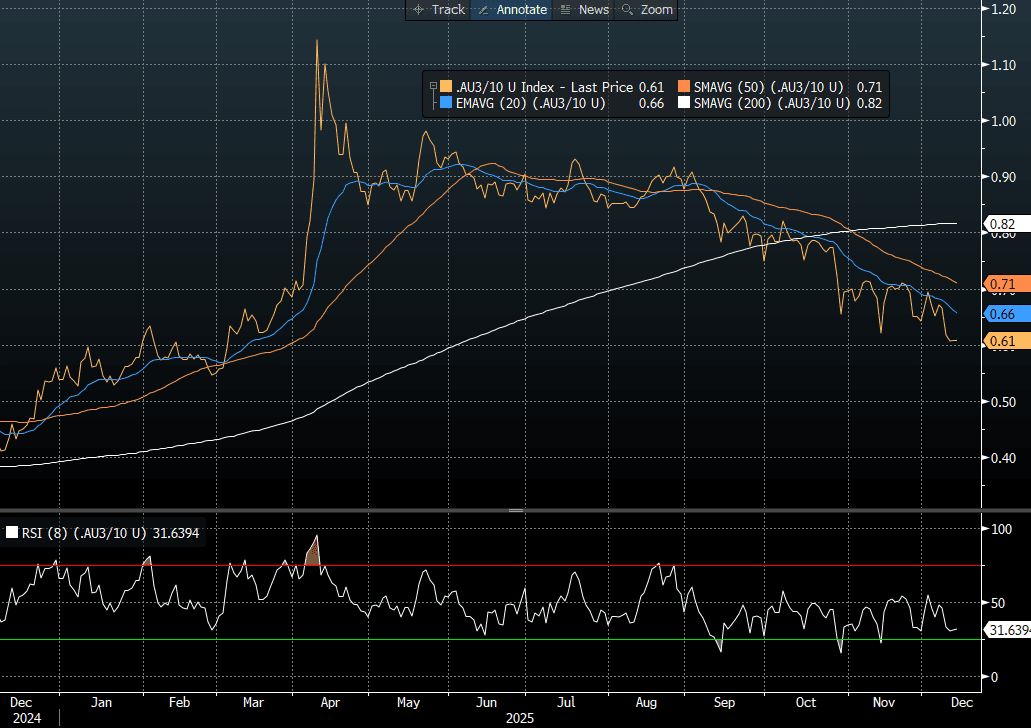

AUSSIE 3-YEAR TECHS: (Z5) Cracks Multi-Year Support

- RES 3: 97.796 - 1.618 proj of the Sep 3 - 12 - 15 price swing

- RES 2: 96.780 - High Jun 26 (cont)

- RES 1: 96.700 - High Sep 12

- PRICE: 95.885 @ 15:38 GMT Dec 11

- SUP 1: 95.755 - Low Dec 10

- SUP 2: 95.480 - Low 1st Nov ‘23

- SUP 3: 94.932 - 1.0% 10-dma envelope

Prices printed fresh pullback lows this week, prompting the active contract to take out notable support into 95.760 and clear through to new multi-year lows. The slower pricing for additional RBA easing - and partial pricing for a return to rate hikes next year - should keep the front-end of the curve under pressure. This keeps prices well below prior resistance at 96.615, the Sep 12 high, and refocuses attention on 95.480 as the next major support.

AUSSIE BONDS: Subdued Start To Data-Light Session, 3/10 YC Flattest Since March

ACGBs (YM -0.5 & XM flat) are little changed after cash US tsys finished near flat.

- Initial jobless claims 'surprised' higher at 236k (sa, cons 220k) in the week to Dec 6, a consensus reading that had looked for surprisingly little rebound considering it followed the 3+ year low of 219k in the week to Nov 29 in what had looked likely down to difficulty in adjusting around the Thanksgiving holiday. Continuing claims, meanwhile, were also lower than expected at 1838k (sa, cons 1938k) in the week to Nov 29 after a marginally downward revised 1937k (initial 1939k).

- Cash ACGBs are flat with the AU-US 10-year yield differential at +56bps.

- The 3/10 curve sits at its flattest since March. The recent curve flattening has occurred alongside a steady rise in market forward expectations for the RBA cash rate. A simple regression of the 3s/10s curve against the 1Y3M rate over the past three years suggests the current curve is roughly 20bps too steep relative to its fair value (see chart).

- The bills strip has bear-flattened, with pricing -3 to flat.

- RBA-dated OIS pricing shows tightening across all meetings, with the probability of a 25bp hike rising from 29% for February to 104% by June and 168% by December 2026.

- Today, the local calendar will be empty.

Bloomberg Finance LP

BONDS: NZGBS: Little Changed After US Tsys Finished Slightly Weaker

NZGBs are slightly richer after US tsys finished little changed after the extension to the post-FOMC faded.

- US tsys extended post-FOMC gains after higher-than-expected weekly jobless claims, while continuing claims were sharply lower than expected.

- Initial jobless claims ‘surprised’ higher at 236k (sa, cons 220k) in the week to Dec 6, a consensus reading that had looked for surprisingly little rebound considering it followed the 3+ year low of 219k in the week to Nov 29 in what had looked likely down to difficulty in adjusting around the Thanksgiving holiday. Continuing claims, meanwhile, were also lower than expected at 1838k (sa, cons 1938k) in the week to Nov 29 after a marginally downward revised 1937k (initial 1939k).

- NZ BusinessNZ manufacturing PMI edged up to 51.4 in Nov, from a revised 51.2 outcome in Oct. This leaves us off recent cycle highs (53.6) in Feb of this year. Post-COVID highs in the index were in the 60-65 range; see the chart below. Whilst the index remains in expansion, the pace of recovery looks fairly modest.

- Swap rates are 1bp lower.

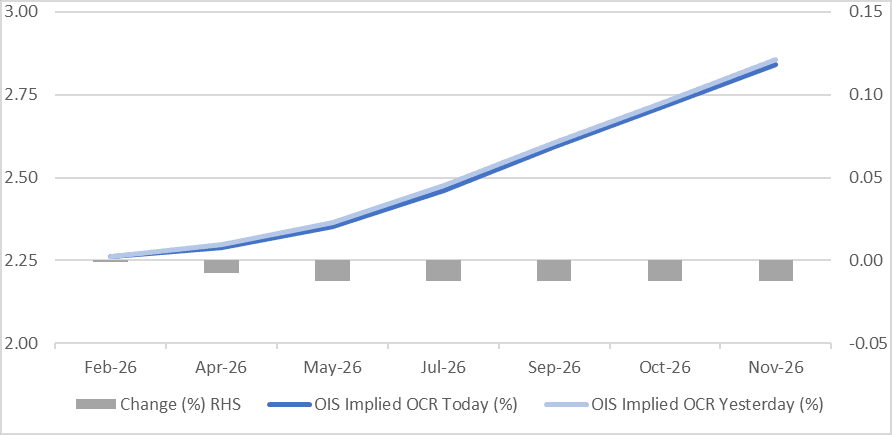

- RBNZ-dated OIS pricing is slightly softer across meetings. 1bp of tightening is priced for February, while November 2026 assigns 59bps (see chart).

Bloomberg Finance LP