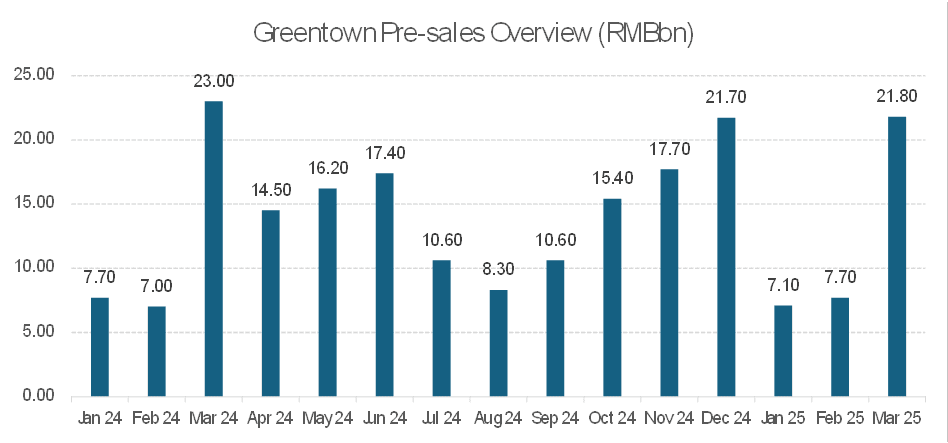

EM ASIA CREDIT: Greentown China (GRNCH, B1/NR/NR) sales decline moderates

Monthly property sales statistics are out for March. Sales reached around

RMB21.8bn (-5% YoY), with an approximate average selling price of RMB42,602 per sqm. As shown in the attached chart, year to date end March sales are around 3% lower YoY. We saw yesterday that Moody's revised the outlook to Stable from Negative as it expects a moderation in sales declines, which was evidenced in Q1. Overall neutral for spreads.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BUND TECHS: (M5) Oversold Trend Position But Remains Bearish

- RES 4: 130.40 Low Feb 19

- RES 3: 129.96 High Mar 5

- RES 2: 129.41 Low Jan 14

- RES 1: 128.33 High Mar 10

- PRICE: 126.85 @ 05:42 GMT Mar 12

- SUP 1: 126.53 Low Mar 11

- SUP 2: 126.28 2.618 proj of the Feb 5 - 19 - 28 price swing

- SUP 3: 126.00 Round number support

- SUP 4: 123.36 3.00 proj of the Feb 5 - 19 - 28 price swing

Bund futures are in consolidation mode and the contract is trading closer to its recent lows. A bearish theme remains intact. Last week’s impulsive sell-off signals scope for an extension towards 126.28 next, a Fibonacci projection. Further out, 126.00 is also within range. Note that the contract is in oversold territory, a recovery would allow this condition to unwind. Initial firm resistance to watch is seen at 129.41, the Jan 14 low.

EU: EU Announces Countermeasures To US Tariffs

The EU Commission has announced countermeasures after US steel and aluminium tariffs on EU imports came into effect. See details below.

- "First, the Commission will allow the suspension of existing 2018 and 2020 countermeasures against the US to lapse on 1 April. These countermeasures target a range of US products that respond to the economic harm done on €8 billion of EU steel and aluminium exports.

- Second, in response to new US tariffs affecting more than €18 billion of EU exports, the Commission is putting forward a package of new countermeasures on US exports. They will come into force by mid-April, following consultation of Member States and stakeholders.

- In total, the EU countermeasures could therefore apply to US goods exports worth up to €26 billion, matching the economic scope of the US tariffs.

- In the meantime, the EU remains ready to work with the US administration to find a negotiated solution. The abovementioned measures can be reversed at any time should such a solution be found." See this link from the EU Commission for more details.

GLOBAL MACRO: Growth Indicators Subdued But Not Flashing Red Yet

Markets have become increasingly concerned over the global growth outlook with signs that US confidence has been hit by uncertainty over US tariffs and likely retaliation. The RBA’s Hauser said that the Fed estimated that global growth was reduced by 1pp in 2019 due to uncertainty alone. Growth indicators are still suggesting that global IP should hold up for now. They continue to be at subdued levels though in line with recent muted growth, but are yet to flash red.

- The Q1 average of JP Morgan’s global composite PMI at 51.7 is below Q4’s 52.4 driven by services signalling slower but still positive growth. February’s composite was the lowest in over a year at 51.5. Manufacturing though has seen a pickup in Q1 but it is too early to tell if this is an attempt to front run US tariffs. China’s manufacturing PMI is down slightly in Q1 at 50.5.

- LME metal prices have been moving sideways for the last year and picked up at the start of this year but within the recent range. This is in line with continued global IP growth of around 2-2.5%. Iron ore has also been moving sideways, while wool has been recovering over the last 6 months.

Global IP y/y% vs LME metal prices

Source: MNI - Market News/Refinitiv

- Global money supply growth has been in a relatively tight range for the last two years. It tends to lead global IP growth and is also consistent with it staying positive but at subdued rates.

- Container freight rates have been trending lower since end-2024 with the easing in geopolitical tensions but the Baltic Freight Index has been recovering but remains off 2024’s highs.

Global IP vs money supply growth y/y%

Source: MNI - Market News/Refinitiv/Bloomberg