FOREX: Greenback Relief Rally Extends, Analysts Believe It Won’t Last

Sep-18 14:53

- Better-than-expected US data has bolstered the relief rally for the greenback Thursday, providing further fuel after the Fed’s mixed messaging disappointed the underlying bearish sentiment. At its highest point today, USDJPY (+0.70%) recovered by an impressive 278 pips, potentially exacerbated by the lingering political uncertainty and a bullish reversal signal on the chart. NZD (-1.46%) continues to lead G10 declines following growth data, placing the short-term focus back on the key pivot support located at 0.5800.

- From a selection of analyst views below, it appears the majority believe this recovery will be short lived, with the rally providing more attractive entry points for dollar bears.

- *SocGen: Ignoring the noise as far as possible, SG believe EURUSD will make it through 1.20 this year and up to the mid-125s in H1 next year. AUDNZD profit taking can act as a broader brake on the AUD, which while frustrating, won’t alter their underlying view that as US rates come down, AUDUSD should rise further.

- *MUFG: The 2-year US Treasury yield is currently trading close to levels prior to last night’s FOMC meeting indicating that rate cut expectations over the coming years have not changed much. Combining this with the growing risk of President Trump having more influence over Fed policy next year when Fed Chair Powell is replaced, MUFG doubt that the relief rally for the US dollar will be sustained.

- *ING interpret yesterday’s Fed decision as a net negative for the dollar, and think that some 'sell the fact' and positioning readjustment have exacerbated the dollar rally during and after the presser. They expect the USD to move lower in the coming days.

- *Rabobank see risk that this short-covering pressure could extend further towards EUR/USD1.16 on a 1 to 3 month view, before the currency pair drifts higher towards the 1.20 level early next year.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

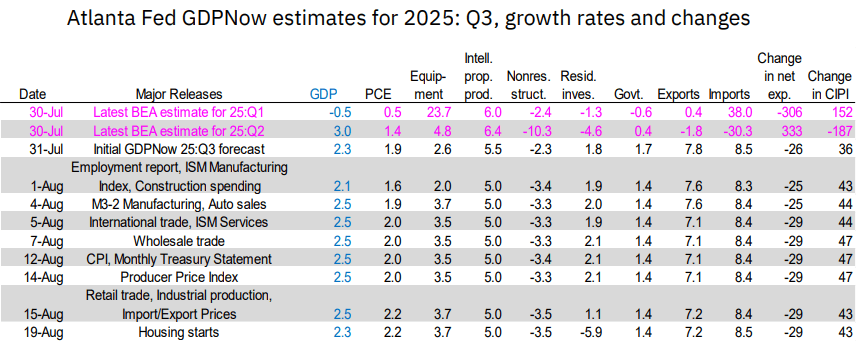

US OUTLOOK/OPINION: Residential Activity Drags On Q3 GDPNow Estimate

Aug-19 14:51

There was a decent pullback in the Atlanta Fed's Q3 GDPNow estimate today to 2.26% from 2.55% in the Aug 15 update. This comes entirely on the back of a shift in the expectation for residential investment growth in the quarter: now seen at -5.9% Q/Q SAAR, vs 1.1% in the prior estimate (and -4.6% in Q1).

- That equates to a 0.24pp subtraction from GDP from residential investment in the quarter, vs +0.04pp in the prior est.

- This reflects a big miss in today's building permits data (-2.8% in July vs -0.5% expected), and is reflective of weakness in a housing sector that increasingly looks like it will continue to be a drag on growth through year-end.

FOREX: GBPUSD Bull Cycle Remains Intact Ahead Of UK CPI

Aug-19 14:48

- GBPUSD has consolidated around the 1.35 mark on Tuesday amid gilts paring some of yesterday's weakness. A technical bull cycle remains intact, keeping sights on 1.3636, the 76.4% retracement of the bear leg between Jul 1 and Aug 1 ahead of tomorrow's UK CPI release.

- MPC focus is on headline CPI, which is expected to rise from June; from the previews that we have read the median expectation is for a 3.7% Y/Y. Energy prices could also gather some interest as we think they might come in higher than the median analyst expectation - for our full preview see here.

- Market expectations have swayed away from a November BoE cut recently following a flurry of better-than-expected data since the last meeting. However, December should remain well in play for now, with Governor Bailey, arguably the median voter, speaking Saturday on a panel in Jackson Hole.

- Danske meanwhile "increasingly see domestic factors and the relative growth outlook between the UK and the euro area as becoming GBP negatives", resulting in an EURGBP call "towards 0.89" on a 6 to 12-month horizon.

- ING mentioned yesterday they see "some sticky UK inflation for July looks unlikely to alter the market's view of the BoE", which "should keep GBP/USD bid this week, where a break of 1.3585/3600 could see 1.3680/3700 by the end of the week".

- Société Générale flagged (also yesterday) that sterling is the G10 currency which Asia market participants appear to be the least confident in.

OPTIONS: Expiries for Aug20 NY cut 1000ET (Source DTCC)

Aug-19 14:34

- EUR/USD: $1.1550(E915mln), $1.1600(E854mln), $1.1660-75(E1.4bln)

- USD/JPY: Y147.25-35($982mln), Y148.00-10($1.5bln)

- USD/CAD: C$1.3800($1.1bln), C$1.3835-55($872mln)

- USD/CNY: Cny7.1050($500mln)