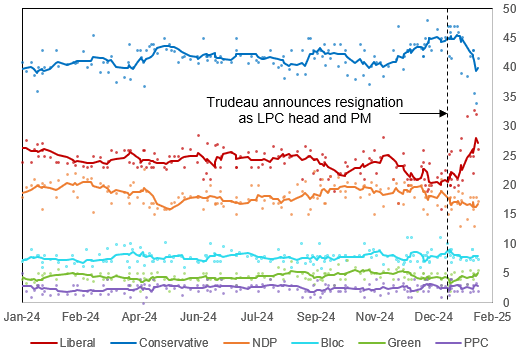

CANADA: Gov't Support Recovering Amid Trudeau Resignation & Trump Tariffs

The governing centre-left Liberal Party of Canada (LPC) is recording its strongest opinion polling in over a year amid heightened political and economic tensions with the US and the ongoing race within the party to succeed outgoing PM Justin Trudeau. In the month before Trudeau's resignation address on 6 Jan, the LPC's average polling score stood at 21.2%. This has risen to 24.5% in the month following.

- The shift towards the LPC may not be wholly attributable to Trudeau's resignation and former BoC and BoE governor Mark Carney becoming favourite to take over. Instead, an increasingly prominent 'rally round the flag' effect amid US President Donald Trump's threats of imposing tariffs and his consistent talk of making Canada a US state could be boosting support for the incumbents.

- In the last week of January, when US tariff threats escalated significantly, the LPC's polling rose further to an average of 27.1%. This included one EKOS poll showing the party on 32.7%, its highest support since May 2023.

- The latest Leger poll for the province of Quebec - accounting for almost a quarter of all seats in the Commons - on 2 Feb gave the LPC 29% support, level with the regionalist Bloc Quebecois. This compares to a 37%-21% advantage for the Bloc a week earlier.

- With a new LPC leader (and therefore PM) to be elected on 9 March given the gov'ts minority status, a snap election may be forced by a vote of no confidence. At the start of the year, an election was seen as almost certainly returning a sizeable Conservative majority. However, recent polling indicates that this may not be so assured.

- Political betting markets have begun to turn, with the Conservatives now assigned a (still high) 77% implied probability of winning a majority, down from a peak of 91% on Jan 17 according to Polymarket.

Chart 1. Federal Election Opinion Polling, % and 6-Poll Moving Average

Source: Leger, Nanos Research, EKOS, Abacus Data, Mainstreet Research, Relay Strategies, Ipsos, Pallas Data, Angus Reid, Innovative Research, MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EQUITIES: US Cash opening calls

SPX: 6,003.3 (+0.5%); DJIA: 42,897 (+0.4%/+190pts); NDX: 21,632.4 (+0.3%).

PIPELINE: $5B ADB 3Y SOFR Debt Launched

Shaping up to be another busy day for corporate bond issuance - unlikely to outpace Monday's record $59.55B.

- Date $MM Issuer (Priced *, Launch #)

- 01/07 $5B #ADB 3Y SOFR+31

- 01/07 $1b #Kuwait Finance House (KFH) 5Y SOFR Sukuk +95

- 01/07 $6B European Investment Bank (EIB) 5Y SOFR+42

- 01/07 $500M DBJ WNG 10Y SOFR+73

- 01/07 $500M Boston Gas WNG 10Y +145a

- 01/07 $Benchmark Chile 12Y +137.5a

- 01/07 $Benchmark World Bank 7Y +54

- 01/07 $Benchmark Met Tower 3Y +70a

- 01/07 $Benchmark CIBC 5Y SOFR+75a

- 01/07 $Benchmark Protective Life 7& +105a

- 01/07 $Benchmark Kommunalbanken 5Y +51

- 01/07 $Benchmark Santander 5Y +135a, 10Y +160a

- 01/07 $Benchmark APA Corp 10Y +180a, 30Y +215a

- 01/07 $Benchmark Cncl of Europe Dev Bank 5Y SOFR+45a

- 01/07 $Benchmark GA Global Funding 5Y +120a, 10Y +150a

- 01/07 $Benchmark HPS Corporate Lending 3Y +165a, +7Y +195a

- 01/07 $Benchmark Kexim 3Y +55a, 3Y SOFR, 5Y +75a, 10Y +90a

- 01/07 $Benchmark SMFG 5.25Y +100, 5.25Y SOFR, 7Y +110a, 10Y +120a

- 01/07 $Benchmark Daimler Truck Fin NA 3Y, 3Y SOFR, 5Y +105a, 7Y +115a, 10Y +125a

- Expected Wednesday:

- 01/08 $Benchmark Inter-American Development Bank (IADB) 5Y SOFR+45a

BONDS: J.P.Morgan Enter Longs In Bunds, More Cautious In GBP Rates

J.P.Morgan write “trade war/tariff uncertainty from US Trump policy remains a downside risk to Euro area growth and given the recent back up we now turn bullish on Euro duration (receive 1Yx1Y ESTR, enter longs in 10Y Bunds).”

- They think that the “heavy January supply calendar is already baked into intermediate German yield valuations.”

- Meanwhile, in the UK, they believe that “valuations in GBP rates are cheap vs. our BoE forecast (~60bp of easing priced over 2025 vs. J.P.Morgan’s 100bp forecast)” but “are more cautious on entering outright longs in GBP rates given the fiscal easing announced in October adds uncertainty over the path of BoE easing.”