FED: Gov Miran: Rates Quite Far From Neutral

Sep-19 15:28

New Fed Governor Miran confirms in a CNBC appearance that he was the bottom dot on the new Dot Plot that saw rates ending the year at 2.75-3.00% (implying a total of 150bp of cuts going into the September meeting). He also suggests that he's not going not write the traditional essay explaining his dissent in favor of a 50bp cut (which which all told implied he supported 50bp cuts in September, October, and December), instead explaining in a speech on Monday (he's scheduled to speak at the Economic Club of New York):

- "This coming Monday, I'm going to be making a speech where I'm going to give a full accounting for my economic views and walk through in meticulous detail the economics and the arithmetic behind getting to those numbers. And it's too big for, you know, people usually write these dissents, and the dissents are, like, a page long, right? I'm going to walk through a lot of economics and a lot of arithmetic and a lot of math, and that's going to take a full speech to do. So we're going to get a full accounting of that on Monday. "

- Asked about whether he thinks conditions warrant a neutral interest rate now (as implied by his Dot Plot submission), Miran says: "I don't see a reason for being so far from neutral at the moment and the fact that we are quite far from neutral given that means the longer you stay very restrictive, the greater the risks build up of significant misses to the employment mandate."

- On whether it could cause concern for market participants to cut as aggressively as he signaled in the Dot Plot, Miran says: "I don't think so, and that's part of why I recommended getting there in in 50 clips instead of one, you know, 200 basis point cut. I mean, if you're really concerned, you would say just, get to neutral now, or get below neutral now. But I think that sort of getting there at a measured pace of half a point at a time is a reasonable pace of doing so. And if you look at the dot plot like I'm really only sticking out this year" but his 2026 dot "is not so far from everyone else's."

- Miran makes the case that monetary policy should be looser despite his expectation for "better growth in the second half of the year." "I want to caution that the implications for monetary policy are not very big, because I see actual and potential output increasing, but ... if you push out the supply side of the economy, you're increasing potential growth, and if actual growth is doing better, also, it's not clear monetary policy should react to it. In fact, standard models will tell you the opposite."

- He reiterates his view that tariffs have had no material inflationary impact. Asked if he's worried about weakness in the labor market, Miran says "We found out that the labor market was not as strong as we thought it was last year and into the beginning of this year. That's what happened in the revisions lately. And then on top of that, I'm more optimistic about the second half of the year, but that doesn't imply anything for monetary policy, because I view it as pushing potential and actual output at the same time. Now, when I put all these ingredients together, in my opinion, being so far above neutral means that monetary policy is quite restrictive, and the longer monetary policy stays [at] that level of restriction, the labor market - having done what it did last year and through the first half of this year - the greater the risks that we start to miss in the employment mandate."

- He says President Trump called him earlier this week to congratulate him on his confirmation as Fed Governor, but "He didn't ask me to do any particular actions. I didn't commit to doing any particular actions. I put down my dot based on my economic analysis and and that's what I'll continue to do."

- Asked about the President's comments that the Fed should cut rates in order to reduce government interest service costs, Miran addresses his prior comments regarding a third Fed mandate on longer-run interest rates, saying "I think it is true that if the interest rate would go down, then the interest expense goes down mechanically. I don't think that's controversial. However, as I said, as I said before, the Congress assigned the Fed some very particular statutory mandates, price stability, full employment, and it is true, moderate long term interest rates, but that's usually considered to be implied by achieving the first two."

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FED: US TSY 17W AUCTION: NON-COMP BIDS $455 MLN FROM $65.000 BLN TOTAL

Aug-20 15:15

- US TSY 17W AUCTION: NON-COMP BIDS $455 MLN FROM $65.000 BLN TOTAL

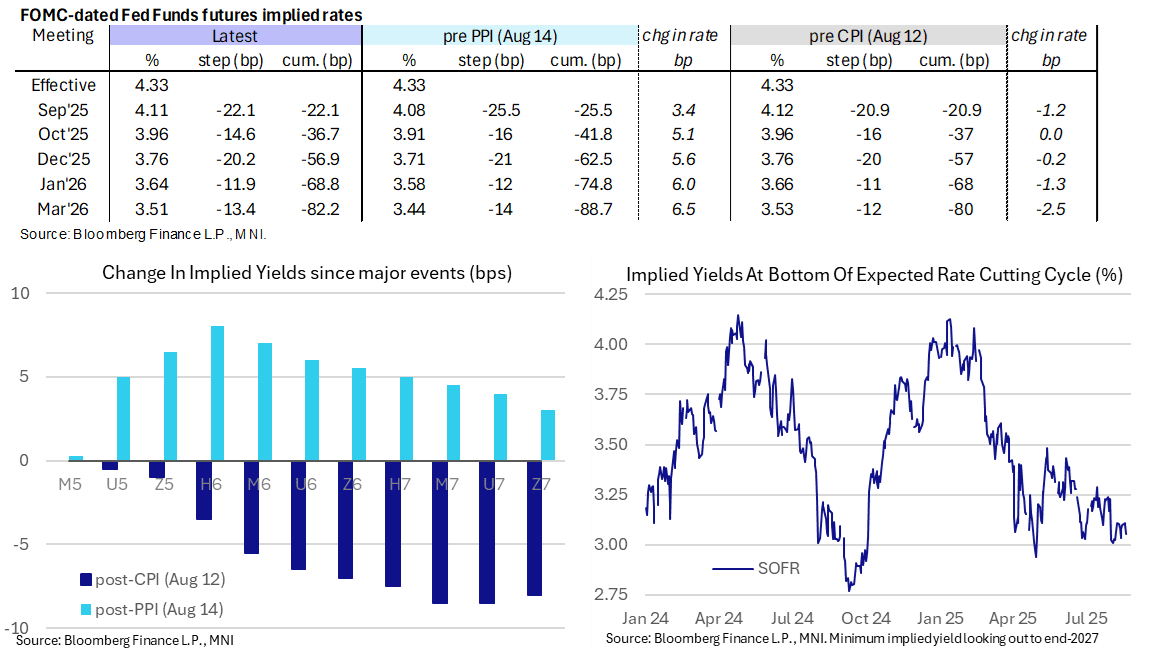

STIR: 2025 Rate Cut Prospects Build But Only Back To Pre-CPI Levels

Aug-20 15:13

- Rate cut prospects have increased on the two-prong nature of tech-led equity weakness and the WSJ reporting that Trump is considering firing Fed Governor Cook (a step up from his earlier Truth Social post urging her to resign).

- Fed Funds implied cumulative cuts from 4.33% effective: 22bp Sep, 36.5bp Oct, 57bp Dec, 69bp Jan and 82bp Dec.

- For context though, the 57bp of cuts to year-end is only back to levels seen shortly after Thursday’s strong PPI report and as such continues to have at least fully reversed the dovish impact from CPI earlier last week.

- Dovish implications are clearer to see further out the curve, with the SOFR implied terminal yield of 3.055% (SFRH7) now 4.5bp lower on the day (7.5bp lower than pre-CPI levels) after some narrow ranges in recent days.

- Terminal pricing does however keep to the 125bp +/-5bp of cuts from current levels range broadly seen since the Aug 1 payrolls report.

US TSY FUTURES: Extending Highs

Aug-20 15:10

- Mirroring late support in German Bund, Treasury futures continue to extend highs in late morning trade, weaker stocks (SPX eminis at 6377.5 -55.0) contributing to the move.

- Tsy Sep 10Y contract +7 at 111-31.5 session high, initial technical resistance at 112-15.5 (High Aug 5 and the bull trigger).

- Curves have reversed early flattening to steeper: 2s10s +.237 at 55.847, 5s30s +1.491 at 109.733.

- Focus on this afternoon's July FOMC minutes release at 1400ET.